- Slow finished offtake hits entire steel production chain

- Only coking coal sees price gains amid supply crunch

- Early monsoon arrival dampens construction activity

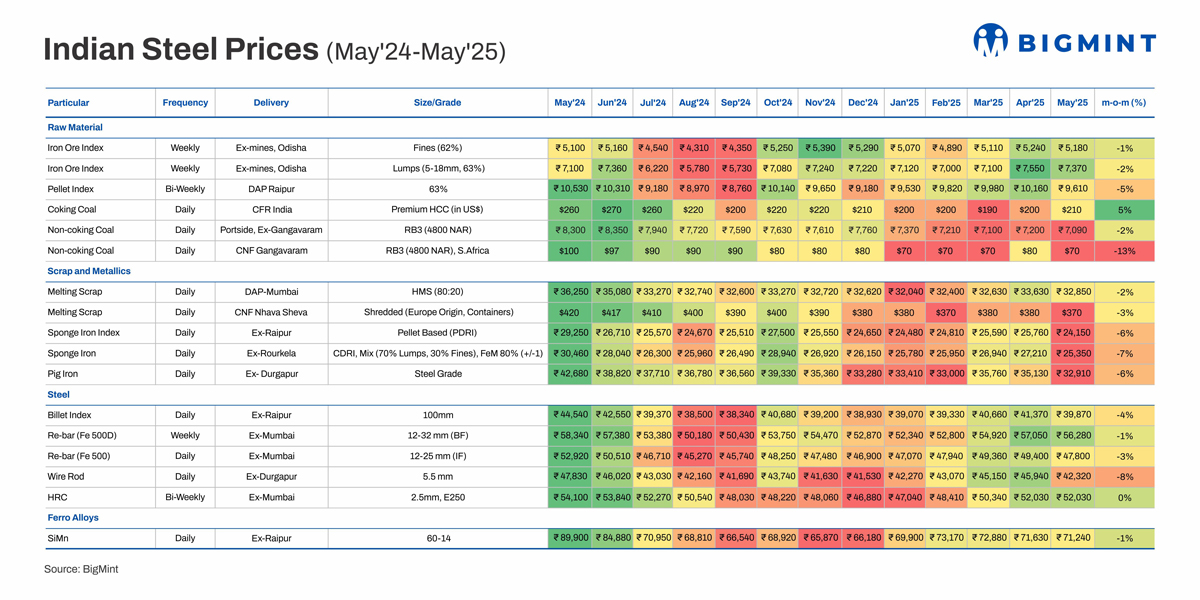

Morning Brief: Domestic steel and raw material prices slumped across the board, with sluggish demand for finished products impacting the entire steel production chain. Only coking coal proved to be an exception, with prices gaining because of limited cargo availability.

As market participants had feared, although the safeguard duty was able to curtail low-priced imports, it was not able to address the core problem of flagging steel consumption.

Manufacturing sentiment also remained weak last month, as evidenced by the purchasing managers’ index falling to a three month-low of 57.6 points.

Factors influencing domestic steel, raw material prices in May’25

Raw materials

Iron ore: Price tags of iron ore, ex-mines Odisha, eroded by 1-2% m-o-m in May, given the downtrend in the pellet, sponge iron, and billet markets. However, pre-monsoon restocking momentum kept prices supported to an extent. Despite lower base prices m-o-m, the response to the Odisha Mining Corporation (OMC) auction was underwhelming, especially for fines, reflecting subdued market sentiment. While some merchant miners revised offers downward, this failed to spark sustained buyer interest.

Pellets: BigMint’s domestic pellet (Fe63%) index, DAP Raipur, lost 5% m-o-m amid sluggish, need-based trade activity. Bid-offer disparities emerged amid expectations of future price corrections, and buyers adopted a wait-and-watch stance amid squeezed profit margins. Additionally, competitive offers from Odisha and increasing selling pressure pressured prices.

Coking coal: Australian premium hard coking coal (PHCC) prices rose 5% m-o-m, amid pre-monsoon restocking in India and supply constraints due to weather-related logistical disruptions. However, demand remained weak, with price resistance from steelmakers. Availability of cheaper Canadian alternatives and a decline in India’s met coke prices to a five-month low also staved off further price gains.

Thermal coal: The bearish sentiment in the sponge iron and steel segments also extended to the thermal coal market. Portside prices of South African thermal coal inched down by 2%, while CNF tags suffered a steeper 13% drop despite summer marking the peak demand season. Indian portside prices of South African coal were at a four-year low in May, with buying interest dulled by a rise in India’s coal production, increased preference for domestic material, and a drop in thermal coal tags globally.

Ferrous scrap: Both domestic and imported scrap edged lower by 2-3% m-o-m in May. Weak steel demand weighed on procurement for both variants, while elevated freights and persistent bid-offer disparities reined in buying interest for imported material. Additionally, a slowdown in the construction segment due to an early monsoon, availability of cost-effective alternatives such as sponge iron, and liquidity shortfalls weighed on scrap demand.

Sponge iron: Prices of sponge iron (PDRI and CDRI) dropped 6-7% m-o-m in May, settling at an over four-year low due to oversupply, driven by rapid production growth; absence of bulk purchases, stemming from muted steel demand; weaker production costs due to lower iron ore and thermal coal tags; and a subdued export landscape.

Pig iron: Pig iron prices were down by 6%, in line with the softness in the steel sector. Even major auctions from leading steelmakers witnessed limited participation, partial bookings, and lower bids. An oversupply in the market also led to slack trading.

Silico manganese: Slow domestic and export trades led to a slight 1% m-o-m dip in silico manganese prices, though production cuts helped prop up tags in the second half of May. Additionally, production costs declined, with manganese ore prices edging lower m-o-m in May. While MOIL implemented reductions of 5-10% across various grades, offers for imported grades slipped, driven by weak demand and market caution.

Steel

Billets: Sluggish finished steel offtake dampened trade momentum in billets, with prices diving 4% m-o-m. Lower raw material tags also failed to provide cost support, and overall, market confidence was poor, given a slowdown in construction activity due to the early arrival of the monsoon.

Rebars: Trade prices of blast furnace (BF) origin rebars dipped 1% m-o-m amid lukewarm procurement trends. Mills faced increased selling pressure, with inventories rising 10% m-o-m in early-June, but with buyers showing continued resistance to prevailing prices, they faced challenges in securing new orders. As a result, mills also offered discounts/rebates last month.

Induction furnace (IF) route rebars fell a sharper 3% m-o-m, as buyers engaged in trades only for their urgent needs. Inquiries were limited, and manufacturers either kept list prices stable or offered discounts. Inventory holding periods increased to above 12 days by the month-end, with heavy rains and labour shortages hindering construction activity.

Wire rods: Wire rods plunged 8% m-o-m, recording the highest fall among all the steel products tracked. First, manufacturers of downstream products such as galvanised iron (GI) wire rods and binding wire faced subdued demand, which led to need-based procurement. Secondly, government-driven infrastructure activity and project orders were low. Additionally, buyers were unwilling to entertain April’s higher offers, and limited buying led to inventory piling up. Consequently, wire rod producers cut offers to liquidate inventories.

HRCs: Hot-rolled coil (HRC) prices remained stagnant m-o-m, with liquidity troubles and subdued demand keeping trade lethargic. Buyers delayed purchases, hoping for further price corrections. Moreover, labour shortages and the monsoon weighed on prices, though supply shortages in early May and a decline in import arrivals due to the safeguard duty lent support.

Outlook

India’s steel and raw material segments are staring at a grim June, with sales volumes expected to be pressured by a continued slowdown in construction activity, liquidity shortfalls and slow payment recovery, and buyer resistance to prevailing prices.

Consequently, prices also face downside risks. While Tier 1 mills have already reduced rebar list prices by INR 1,500/t ($17/t), HRC prices are likely to be rolled over or cut by INR 1,000/t ($12/t).

Parallelly, NMDC has trimmed its iron ore offers by INR 150-160/t ($2/t). The downtrend is likely to extend to other commodities and may last until the end of the monsoon.

Leave a Reply