- India sees lower arrivals amid steel price volatility

- Pakistan, B’desh continue to face HKC upgrade delays

South Asia’s ship-breaking markets remained under pressure in May due to geopolitical tensions, weak currencies, and disruptions related to complying with the Hong Kong Convention (HKC). India witnessed sluggish activity at Alang, while Pakistan faced letter of credit (LC) issues and slow compliance. Bangladesh led in terms of the tonnage processed, though it struggled with yard restrictions and political uncertainty, pushing vessel flow towards India.

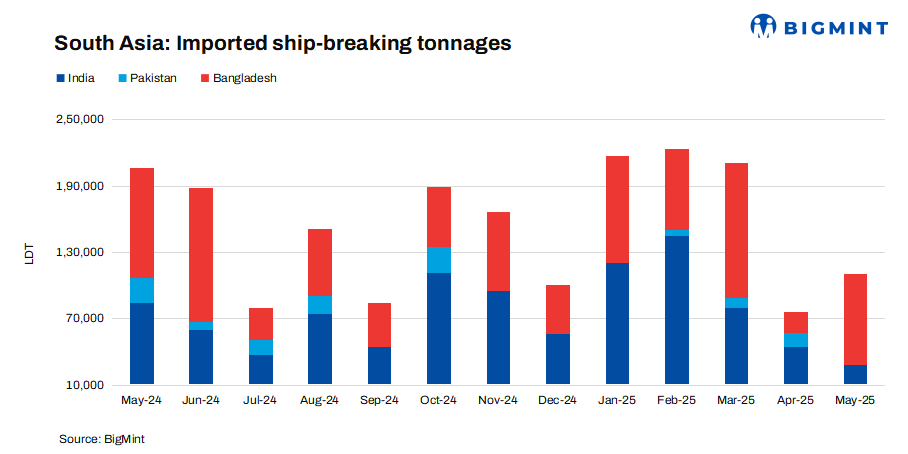

India: India’s ship-breaking sector processed 28,379 light displacement tonnes (LDT) in May 2025, a 36% decline compared to April’s 44,062 LDT. However, this was a 66% decrease compared to the 84,181 LDT recorded in May 2024.

The Alang ship-breaking yard saw a decrease in arrivals, receiving four vessels for recycling in May, four fewer than in April.

India’s ship-breaking market stayed weak in May, with limited vessel arrivals and cautious buying at Alang. Hopes of a pre-monsoon boost faded amid steel price volatility, rupee depreciation, and geopolitical tensions. A brief rise in arrivals saw most deals close at losses due to poor supply and demand.

However, later in the month, India gained over Bangladesh, as delays and yard constraints shifted deals to Alang. Recyclers secured large vessels, including LNG carriers and tankers, but a sharp $11/tonne (t) drop in steel prices kept pressure on offers. Although tonnage supply improved, sentiment remained subdued.

Pakistan: No tonnage arrived for recycling in May 2025, a sharp decline from 13,533 LDT in April and a significant drop from 22,347 LDT recorded in May 2024. Notably, no ships were recycled in April.

Pakistan’s ship-breaking market remained mostly inactive in May amid trade curbs, political tensions with India, and weak fundamentals. A falling rupee, LC issues, and declining steel prices kept recyclers cautious. Brief early-month buying faded, leaving Gadani yards largely empty despite firmer local steel prices.

By the month-end, urgency grew with the 26 June HKC deadline approaching. Though Pakistan briefly gained from regional disruptions, limited HKC compliance capped deals. A small steel price rise and IMF-backed support offered slight relief, but without swift upgrades, key tonnage may be missed.

Bangladesh: Bangladeshi recyclers processed around 82,012 LDT in May 2025, showing a sharp fourfold increase from 18,684 LDT in April, although this was 17% lower than the 99,504 LDT recorded in May 2024.

Twelve ships were recycled during the month, up by six compared to April, reflecting a notable increase in m-o-m performance.

Bangladesh’s ship-breaking market remained under pressure in May due to delays with securing HKC compliance and no objection certificates (NOCs). While approvals resumed for certified yards, only a few were operational, prompting sellers to divert vessels to India and Pakistan. Steel plate prices held steady at $475-477/t, but weak pre-monsoon demand kept sentiment low.

Later in May, the taka weakened, and steel prices fell by $21/t, adding pressure. Though nine yards gained HKC approval, clearance delays and inspections created backlogs. With most yards nearly full and political uncertainty ahead of the 30 June elections, buying slowed further, shifting focus to India.

Leave a Reply