- Chinese coal firms cut 2025 output amid declining profitability risks

- High inventories, weak demand pressure prices despite policy support

Mysteel Global: More Chinese listed coal companies have set lower production guidance for 2025, citing ongoing loss-making risks as subdued downstream demand may continue to drag selling prices lower, Mysteel Global has learned from their latest reports.

Among the 15 coal firms that have disclosed their operation plans for this year, 8 have announced reduced production targets, Mysteel Global noted. Notably, Shanghai-listed Shanxi Lu’an Environmental Energy Development plans to produce around 50 million tonnes of coal in 2025, which represents a 13.1% fall compared with the 57.57 million tonnes it produced last year. This also marks the sharpest drop in coal production guidance among the 15 coal firms.

Profit decline being a key driver

The year of 2025 started with a bearish note since domestic coal consumption – whether by coke makers, steel mills or power generators – kept notching new lows even following a downbeat 2024. Profitability among coal miners, as a result, was battered in the first quarter this year, dampening their confidence towards the near-term market, Mysteel Global understands.

Mysteel’s review of the latest quarterly reports from 39 listed coal enterprises showed that 29 remained profitable in the first quarter, but most reported varying degrees of year-on-year net profit declines. The remaining 10 posted losses, with Panjiang Refined Coal suffering a drastic reversal – swinging from a Yuan 21 million ($2.9 million) profit in Q1 2024 to a loss of Yuan 105 million.

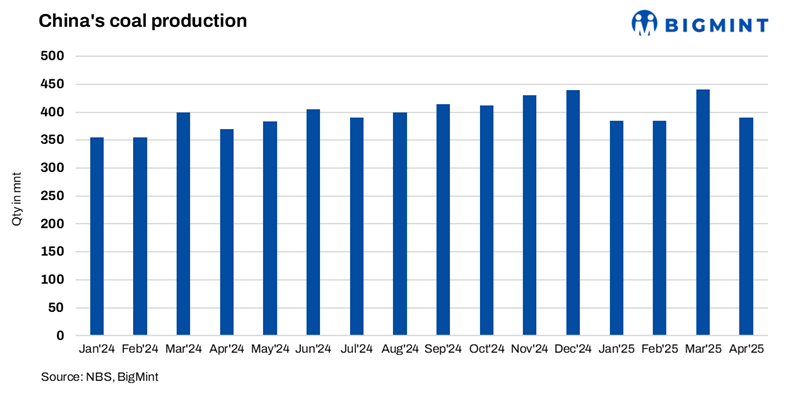

The profit decline began in 2024, when shrinking demand worsened an already significant supply surplus caused by record-high imports and domestic coal production, Mysteel Global noted. China’s coal imports and output last year reached all-time highs of 542.7 million tonnes and 4.76 billion tonnes, respectively, as reported. This indicated a total coal supply of 5.3 billion tonnes in the domestic market in 2024, up by 3.3% from 2023, Mysteel Global calculated.

Market scenario for 2025 stays dim

This glut has continued to weigh on China’s coal market so far this year. For example, domestic prices of coking coal – a major ingredient for steelmaking – trended lower as stock accumulation kept weakening pricing stance among miners, despite previous price rebounds in the downstream steel market and the still-high hot metal production at steel mills. Meanwhile, thermal coal prices experienced a free fall in the past month due to record inventories at China’s northern ports.

With such massive stockpiles to be digested, the coal market outlook for the whole year of 2025 remains grim. Any notable recovery for the fuel prices in the future may not be sustained for long, some market insiders warned.

Oversupply – a similar yet different fate

The current oversupply in China’s coal market seems a repeat of some similar market conditions during 2012-2016, when coal production capacity expanded drastically with the country’s investment boom while energy consumption intensity dropped due to a change of economic growth model.

However, unlike an effective mitigation of excessive coal supply following China’s 276-workday regulation at domestic coal mines in 2016, no comparable policy has emerged yet to pull the market out of the embattled situation this time, Mysteel Global noted.

“Coal output reduction is the best solution to this long-standing problem,” a North China-based trader said. “The several major market upticks in the past two years – which had already presented a fading upward strength of an oversupplied market – all coincided with major cuts on supplies, since end-users were apparently motivated to temporarily drop their low-inventory strategies,” he explained.

But a substantial reduction in coal output is unlikely this year. Despite lower production targets made by some coal firms, many mines will opt to ramp up production in the near term to dilute elevated per-tonne production costs, according to Mysteel’s latest survey.

Energy security still a priority

After experiencing energy shortages over 2021-22, China has lifted the priority of national energy security to a new high, especially when the increased geopolitical conflicts worldwide have stimulated major economies to shake off energy dependence on other nations in recent years.

This was echoed by a statement made by the National Energy Administration during a meeting last December that China will target 4.8 billion tonnes of coal production in 2025, demonstrating the country’s sustained focus on ensuring energy security. The goal for this year suggests another growth of 0.84% compared with the realized output last year, Mysteel Global learns.

Additionally, Shanxi province, the country’s second-largest coal-mining hub after Inner Mongolia, is expected to pursue higher coal output at around 1.3 billion tonnes in 2025 – a 2.4% increase year-on-year – in a bid to support regional economic recovery after last year’s output cuts.

China has delayed coal imports by tightening controls on trace elements of imported cargoes starting this year, which is another common strategy used to balance domestic coal supplies. Despite these measures, coal stocks remain stubbornly high, despite a cumulative year-on-year decrease of 8.48 million tonnes in coal imports during January-April.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply