- Inventories rise m-o-m in subdued market

- IF-rebar prices drop m-o-m on weak sentiments

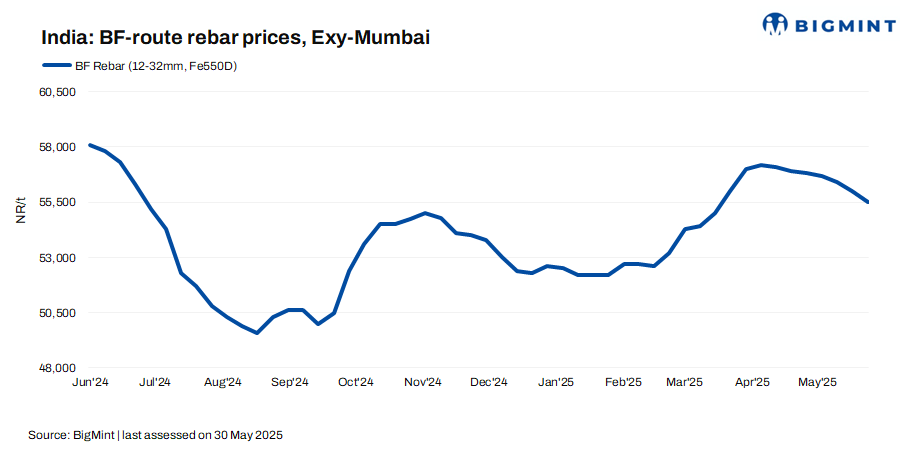

Indian Tier-1 mills have reduced rebar list prices by up to INR 1,500/t ($17/t) for early-June 2025 deliveries as against prices prevailing in end-May, sources informed BigMint. Post-revision, list prices were at INR 54,500-55,500/t ($635-646/t) on landed basis. It should be noted that mills had offered discounts/rebates to augment sales last month.

Rebar inventories at Tier-1 mills increased by approximately 10% m-o-m in early-June, sources informed, due to sluggish sales in May, as declining prices and subdued demand posed challenges for mills in securing new orders.

Update on projects

- KEC International has secured new orders worth INR 2,211 crore across T&D in the Middle East and Americas, oil & gas terminal works in Africa, and cable supply orders in both domestic and international markets.

- L&T’s Water & Effluent Treatment (WET) business has secured significant orders from Rajasthan’s Public Health Engineering Department, including an EPC contract for rural water supply and fluorosis mitigation, covering 5,251 km of pipelines and various reservoirs in Jhunjhunu and Ajmer districts.

Factors behind drop in prices

1. IF-rebar prices decline m-o-m: Induction furnace (IF) rebar trade prices declined steadily throughout last month amid weak market sentiment, limited demand, and need-based buying. Manufacturers responded to muted inquiries and slow trade activity by either rolling over list prices or offering discounts. As demand weakened further, especially in monsoon-affected regions, inventory holding period increased to above 12 days by month-end. Overall, the market remained under pressure due to seasonal slowdown and cautious buying. IF rebar prices dropped by INR 1,600/t ($19/t) m-o-m to a monthly average of INR 47,800/t ($557/t) exw-Mumbai in May.

The BF-IF rebar price gap widened to around INR 8,500/t ($99/t) in Mumbai. IF rebars hold a dominant 65-70% market share in India.

2. Property registrations drop m-o-m: Property registrations in Mumbai, the country’s largest real estate market, witnessed a drop of 5% m-o-m to 11,565 units in May as against 12,142 units in April, as per data released by Knight Frank India. Y-o-y, registrations were down 4% as compared with 12,000 units in May 2024.

3. Raw material prices range-bound: BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,100/t ($59/t) on 31 May. Iron ore prices in Odisha continued to face downward pressure this week as weak demand from the downstream steel sector weighed heavily on market sentiments. Sponge iron and finished steel prices declined over the past two weeks, prompting traders to adopt a cautious, wait-and-watch approach.

NMDC reduced iron ore prices by INR 150–160/t ($/t), setting DR CLO at INR 7,050/t ($82/t) and fines at INR 5,350/t ($62/t) (FOR Bacheli), including royalty, DMF, and NMET.

Australian premium hard coking coal (PHCC) prices rose by $4/t w-o-w to $210/t CNF Paradip.

Outlook

Trade-level BF-rebar prices may remain under pressure in the coming days amid need-based buying activities.

Leave a Reply