- Indian buyers cautious amid weak steel demand

- Turkish scrap prices decline, activity slows down

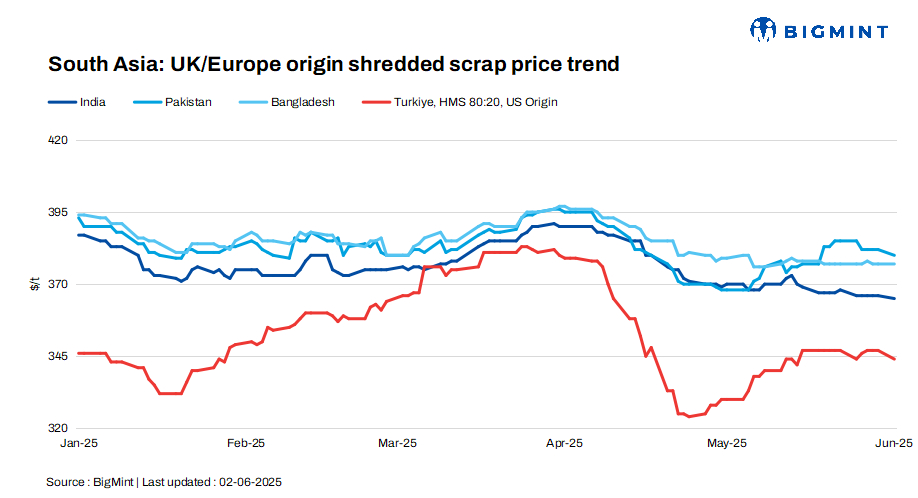

The South Asian imported scrap market remained under pressure today, with trading activity slowing across key regions due to the upcoming Eid al-Adha holidays, weak steel demand, and ongoing logistical constraints. UK-origin shredded offers softened by $1/tonne (t) in India and $2/t in Pakistan, while prices held steady in Bangladesh amid low buying interest.

Across India, Pakistan, and Bangladesh, mills showed limited appetite for fresh bookings as domestic alternatives, letter of credit (LC) issues, and seasonal factors such as the monsoon added to the slowdown.

In parallel, Turkiye echoed the regional quietude, with bulk scrap prices slipping by up to $3/t amid subdued demand and cautious mill buying.

Market overview

India: India’s imported scrap market remained weak, pressured by poor finished steel demand, availability of cheaper alternatives such as domestic sponge iron and Iranian hot briquetted iron (HBI), and cautious buying ahead of the monsoon. Mills delayed scrap purchases amid sluggish construction activity and rising use of direct reduced iron (DRI).

Containerised shredded offers were at $365-370/t CFR, but tradable values and deals mostly settled at $360-365/t CFR. HMS 80:20 was offered at $345-350/t CFR, with deals at around $340-345/t. Overall, market activity was subdued, with buyers sidelined and volumes thin, as both supply and demand fundamentals remained weak.

Pakistan: Pakistan’s imported scrap market remained sluggish, with limited bookings due to weak finished steel demand and the onset of the Eid al-Adha holidays. Mills remained cautious, leading to low trading activity.

Offers for UK/EU-origin shredded were at $380-382/t CFR Port Qasim, while bookings and tradable values hovered at around $380/t. Despite freight surcharges, Pakistani buyers continued to pay higher prices than their Indian counterparts. Some cargoes were initially diverted to India due to logistics, but softer Indian demand may redirect them back.

Bangladesh: Bangladesh’s imported scrap market remained slow, as mills paused fresh bulk bookings after securing ample volumes earlier. Demand weakened further due to upcoming Eid holidays, LC constraints, adverse weather conditions, and high freight costs. Bulk HMS 80:20 offers from the US stood at $355-360/t CFR, while shredded was quoted at $360-365/t CFR.

Containerised HMS and shredded prices from Australia remained stable at $350-355/t CFR and $375-380/t CFR, respectively. With mills sufficiently stocked and construction activity subdued, market sentiment stayed cautious and trade volumes limited.

Turkiye: Turkiye’s imported scrap market weakened, as mills remained largely inactive with the onset of the Eid al-Adha holidays. Offers for EU-origin HMS 80:20 dropped to $334-338/t CFR, while US/Baltic-origin material hovered at around $344/t CFR. Mills delayed purchases, citing poor finished steel sales and a wait-and-watch approach. Recyclers struggled to reduce offers further due to firm euro exchange rates and rising costs. Market sentiment remained bearish, with activity expected to stay subdued until the holiday ends.

Price assessments

India: UK-origin shredded indicatives were assessed at $365/t CFR Nhava Sheva, down by $1/t compared to the last close on Friday.

Pakistan: UK-origin shredded indicatives stood at $380/t CFR Qasim, down by $2/t compared to the last close on Friday.

Bangladesh: UK-origin shredded prices were assessed at $377/t CFR Chattogram, unchanged in comparison with the last close on Friday

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $344/t CFR Turkiye, down by $3/t compared to the last close on Friday.

![]()

Leave a Reply