- HRC trade prices fall, liquidity crunch impacts trade sentiment

- Rebar prices soften as monsoon affects construction demand

- Deteriorating global steel prices exert pressure on domestic market

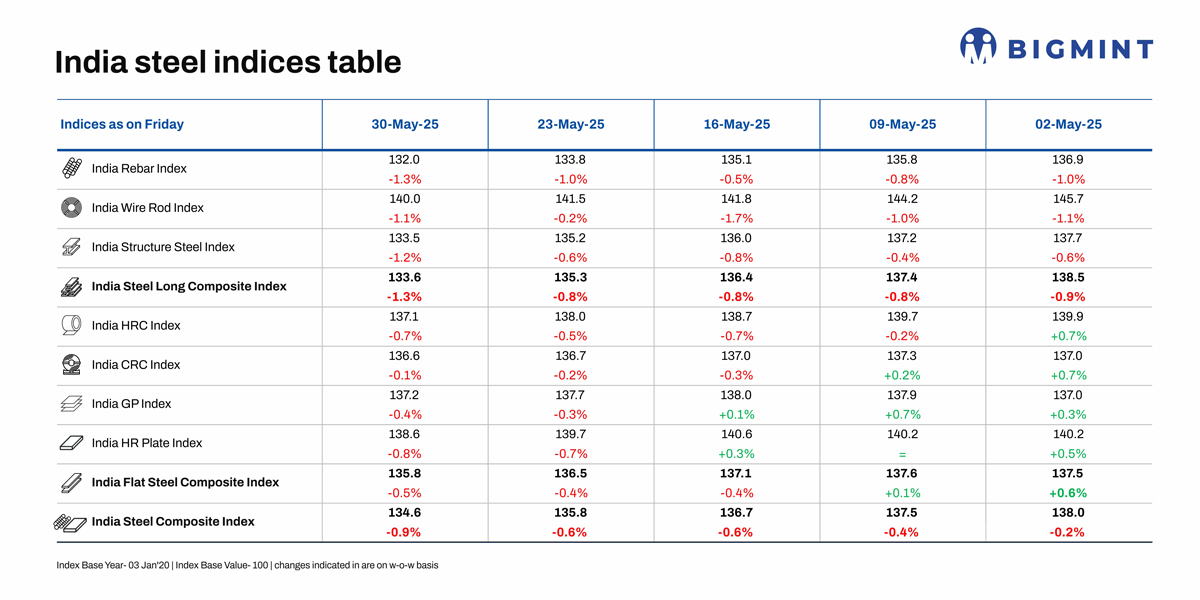

Morning Brief: The Indian steel market remained under pressure in the last week of May 2025 and prices witnessed a decline across segments. As assessed on 30 May, the India Steel Composite Index edged down by 0.9% w-o-w, its sharpest weekly decline last month. While the flat steel index fell by 0.5% w-o-w, the longs composite index declined more steeply by 1.3% w-o-w.

In May, the flagship index – a barometer of the domestic steel market – fell by 2.7%, which indicates that the 12% provisional safeguard duty on imports of flat steel, which came into force in mid-April, failed to have a sustained positive impact on the market amid global uncertainty and deterioration in steel prices.

Flats

HRC trade prices decline: Trade-level prices of hot-rolled coils (HRCs) fell by up to INR 500/tonne (t) ($6/t) w-o-w to INR 51,100-52,800/t ($596-616/t) across markets, as per BigMint’s latest reading recorded on 28 May. The benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) declined by INR 300/t ($4/t) w-o-w to INR 51,500/t ($601/t).

Demand was low because many parts of south India received heavy rainfall. Additionally, the market continued to grapple with tight cash flows due to high levels of credit sales and slow payment collections.

However, the CRC index fell marginally by 0.1% w-o-w. Cold-rolled coil prices showed a mixed trend and were at INR 56,500-61,500/t ($659-718/t).

HRC export prices stable: Indian HRC export offers remained stable w-o-w at $630-635/t CFR Antwerp ($580-585/t FOB East India) under pressure from weak demand and seasonal uncertainties. As a result, Indian mills continued to focus more on the domestic market due to better price realisations.

Longs

Blast furnace rebar prices drop: Trade-level BF rebar prices declined by INR 500/t ($6/t) w-o-w to INR 55,500/t ($649/t) exy-Mumbai, as on 30 May. Prices are exclusive of GST at 18%. Trade prices dropped w-o-w across major domestic markets due to need-based buying activities. Uncertainty over mill pricing for June prompted buyers to delay purchases.

In the projects segment, prices were under pressure at INR 54,000-54,500/t ($631-637/t) FOR Mumbai, as buyers remained cautious amid market uncertainty and weak sentiment. The early onset of monsoon rains and labour shortages put a brake on construction activity, impacting procurement decisions.

IF rebar trade prices fall w-o-w: IF rebar trade prices declined w-o-w on soft demand. The monsoon-affected regions saw slower sales, prompting manufacturers to reduce list prices and offer discounts. This led to inventories rising above 12 days compared to 10-12 days last week. In Mumbai, prices plunged INR 1,000/t on the week to settle at INR 46,800/t exw on 30 May.

Outlook

Monsoon blues will continue to affect market sentiments going forward, with the arrival of seasonal rains in different parts of the country. At the same time, labour crunch and liquidity issues are likely to impact trading. Moreover, weak global steel prices will exert heavy pressure on the domestic market, especially the flats segment, with the export scenario, too, continuing to remain bleak.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply