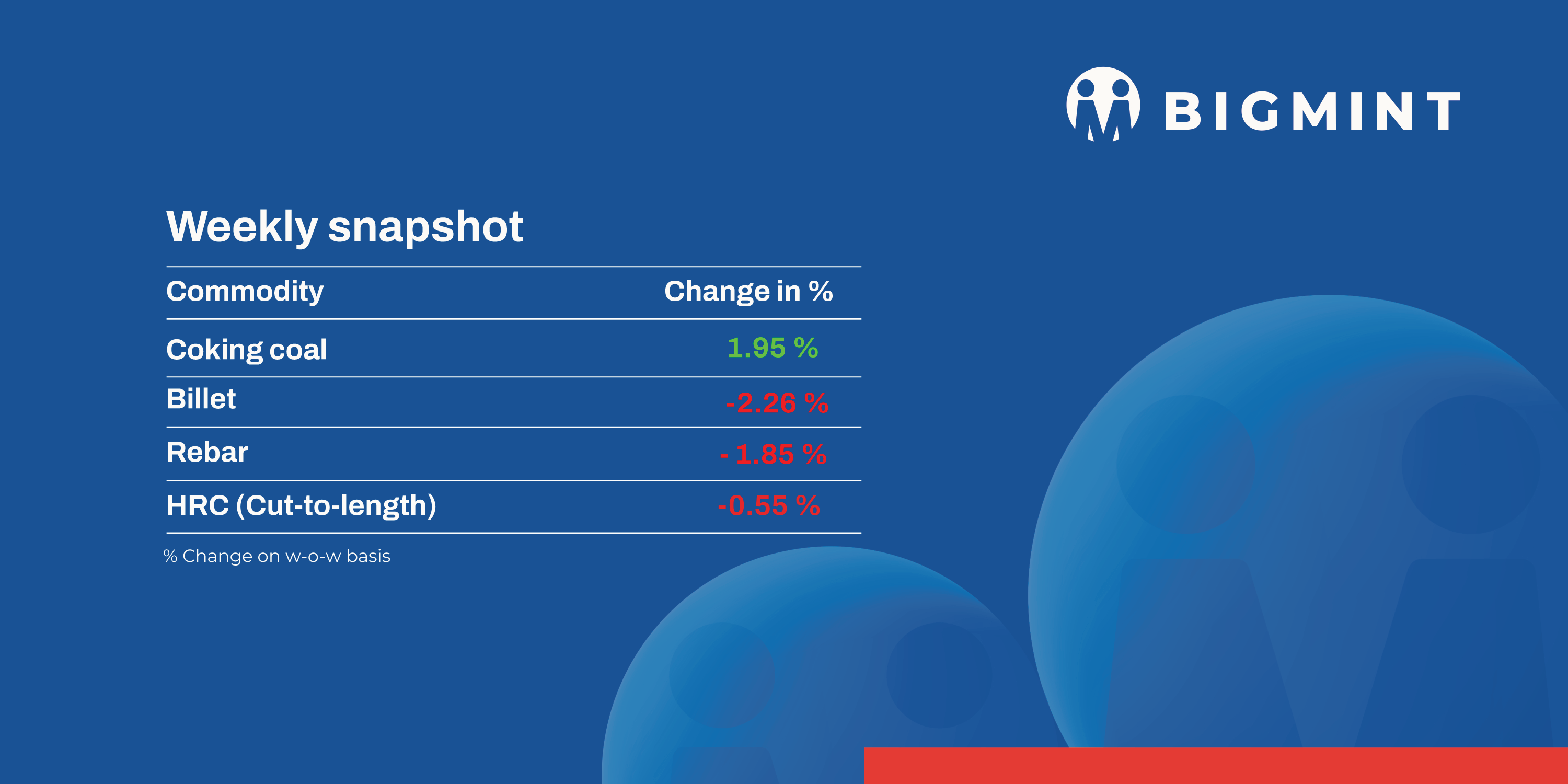

- IF rebar prices down by INR 500-1,100/t w-o-w

- Trade-level HRCs fall by up to INR 500/t w-o-w

Domestic induction furnace finished long steel prices declined by INR 500-1,100/tonne (t) w-o-w. Trade reference prices of hot rolled coils (HRCs) and cold rolled coils (CRCs) also dropped by INR 300-500/t. Semi-finished prices showed a predominant downtrend across majority of the markets.

Iron ore and pellet

- BigMint’s bi-weekly domestic pellet (Fe63%) index fell by INR 150/t ($2/t) w-o-w to INR 9,250/t ($108/t) DAP Raipur on 30 May. Raipur-based pellet producers reduced offers for Fe 62/63% (+/- 0.5%) by INR 9,000-9,100/t ($105-106/t) exw. Around 65,000 t of trade took place this week in the Raipur region by local and Odisha suppliers.

- NMDC Chhattisgarh auctioned 193,200 t of iron ore from its Bacheli mines on 29 May. Of 189,200-t of Baila fines (Fe 64%), around 51,000 t were sold at a base price INR 5,500/t. Notably, in the last 4-6 months, for the first time, iron ore fines received bids. The entire 4,000-t lumps (10-20 mm, Fe 65.5%) were booked at a base price of INR 6,640/t. Prices were on FOR basis, inclusive of royalty, DMF, and NMET.

- An Indian pellet-maker recently concluded an export deal for 50,000 t (Fe63%, 2.5% Alumina) via tender. The deal was recently concluded at around $96-97/t FOB India, as per sources. Due to the decline in seaborne iron ore prices, bids have decreased for the pellet export tender.

Coal

- South African thermal coal prices at Indian ports remained under pressure this week, with RB2 (5,500 NAR) assessed flat at INR 7,900/t exw-Gangavaram and RB3 (4,800 NAR) stable at INR 6,900/t. Demand was muted amid the onset of the monsoon, pushing portside prices to near four-year lows. Thermal coal stocks at Indian ports rose almost 2% w-o-w to 15 million tonnes (mnt) in week 21 of CY’25, up from 15 mnt last week.

- Domestic coal prices in India declined this week amid sluggish industrial demand and limited buying activity. The 4,500 GCV grade dropped by INR 50 to INR 4,300/t ex-Bilaspur, while 5,000 GCV remained unchanged at INR 4,800/t. SECL’s auction on 26 May saw the allocation of 676,200 tonnes, largely comprising power-grade G11 coal. As most volumes were taken by power plants, demand from the non-power segment stayed subdued. This lack of industrial offtake continued to weigh on prices.

- Indian metallurgical coke (met coke) prices declined further this week, hitting a five-month low amid poor demand and lack of trade. BigMint assessed 25–90 mm BF-grade coke at INR 31,500/t ex-Jajpur, down INR 800/t w-o-w, while Gandhidham prices slipped INR 200/t to INR 30,800/t. Offers as low as INR 29,500/t were reported. Weakened steel prices and muted procurement by mills weighed on sentiment.

Ferrous scrap

- India’s imported scrap market stayed stable this week as mills avoided fresh bookings amid weak steel demand and tight margins. Buyers preferred cheaper alternatives like sponge iron and pellets, making it harder to justify high scrap prices and limiting overall import activity.

- UK-origin shredded scrap was assessed at $366/t CFR, slightly down from last week. Offers hovered at $370-375/t, while bids stayed lower at $360-365/t. Mills remained cautious, favouring short-transit cargoes amid monsoon uncertainty, leading to limited bookings.

- Activity was slow across regions, with low material inflows and the upcoming summer holidays season in the West adding to the subdued mood. No immediate demand recovery is expected.

- India booked around 5,500-6,500 t of imported scrap this week, including 2,500-3,500 t of HMS 80:20 at $335–350/t, 1,500-2,000 t of PNS at $370-372/t, with the rest being Busheling and Turning scrap.

Ferro alloys

- Silico manganese: Indian silico manganese prices witnessed a slight rise of INR 200/t ($2/t) w-o-w to INR 71,500-72,200/t ($836-844/t) in the key regions of Durgapur, Raipur and Vizag. Prices rose mainly due to limited supply, despite subdued downstream demand. Market participants expect stability to persist as availability tightens. Attention is now focused on MOIL’s anticipated manganese ore price revision for June 2025, which may influence market direction.

- Ferro manganese: Indian ferro manganese (HC 70%) prices increased by INR 200/t ($2/t) w-o-w to INR 72,500/t ($847/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, also rose by INR 500/t ($6/t) to INR 72,800/t ($851/t). Due to persistent supply shortages and production cuts, producers resisted cutting prices, pushing them higher.

- Ferro silicon: Indian ferro silicon prices were mostly stable with a slight rise of INR 200/t ($2/t) w-o-w to INR 94,300/t ($1,102/t) exw-Guwahati. However, prices in Bhutan stood at INR 94,900/t ($1,109/t) exw, down by INR 100/t ($1/t).Prices remained stable due to low inquiries, with most market participants awaiting next month’s price announcement from Bhutan.

- Ferro chrome:Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices remained unchanged w-o-w at INR 100,300/t ($1,172/t) exw-Jajpur. Following the OMC auction on 19 May, and rising chrome ore prices, many domestic sellers, especially those without captive sources, maintained their offers

Semi-finished

- Indian semi-finished steel prices showed mixed trends as per BigMint’s assessment. Domestic billet prices in all key locations decreased by INR 500-1,100/t across regions except in Raipur where tags rose by INR 100/t. Similarly, sponge iron prices also showed a downward trend in almost all key locations, moving down by INR 200-800/t, with a major decrease of INR 800/t seen in the Ramgarh region.

- Indian DRI (Direct Reduced Iron) export offers decreased by $6/t for CPT Raxaul to $334/t while, CPT Benapole offers decreased by $11/t to $324/t.

- SAIL’s Bokaro Steel Plant (BSL) held an auction for 17,500 t of steel-grade pig iron on 29 May. The total volume was booked at an average price of INR 30,800/t exw. In the previous auction on 19 February, the entire quantity of 17,500 t offered was sold at an average price of INR 30,700/t exw.

Finished longs

IF-rebar: India’s induction furnace-route finished long rebar prices continued to face pressure this week, recording further declines. Buyers stuck to need-based purchases, while a wide gap between bids and offers forced manufacturers to lower trade prices. Retailers remained cautious, avoiding bulk buying due to market uncertainty and heavy rainfall in key regions. This slowed demand, increased sales pressure at mills, and led to inventory buildup, now at around 10-12 days. Prices, though near their lowest, in most of the regions, are likely to remain subdued amid no major clear signs of recovery.

- On a weekly basis, rebar steel prices declined by INR 600-1,800/t across regions, as per BigMint assessment.

- The trade reference prices of IF-route Fe 500 grade rebar of 10-25 mm was assessed at INR 42,200-42,600/t exw Raipur, and at INR 46,000-46,600/t exw Jalna.

- Trade reference prices of heavy structural steel of 150mm stood at INR 44,100-44,400/t exw-Raipur.

- Trade reference prices of wire rods hovered at INR 42,500-43,000/t ex Raipur.

- BF-rebar: Trade prices fell w-o-w across major Indian markets due to need-based buying activities. Uncertainty over mill pricing for June prompted buyers to delay purchases. As such, they chose to stay on the sidelines and adopt a cautious approach.

Trade-level BF rebar prices declined by INR 500/t w-o-w to INR 55,500/t exy-Mumbai, as per BigMint’s assessment on 30 May 2025. Prices are exclusive of GST at 18%.

In the projects segment, prices were under pressure at INR 54,000-54,500/t FOR Mumbai, as buyers remained cautious amid market uncertainty and weak sentiment. Early monsoon and labour shortages further slowed construction activity, impacting procurement decisions.

Flats

- Trade-level prices of India’s hot-rolled coils (HRCs) fell by up to INR 500/t ($6/t) w-o-w, to INR 51,100-52,800/t ($596-616/t) across markets. CRC prices showed mixed trend w-o-w at INR 56,500-61,500/t ($659-718/t).

Market demand is low because many parts of southern India have started receiving rainfall. In addition, the market is facing a cash shortage due to high levels of credit sales and slow payment collections. - India’s bulk imports of HRCs and plates touched 2,49,446 t as of 27 May 2025, based on vessel line-up data from BigMint. Around 21,648 t of additional cargo are expected by May-end and 88,820 t in June 2025.

- Indian HRC export offers remained stable w-o-w at $630–635/t CFR Antwerp ($580–585/t FOB East India). Weak demand and seasonal uncertainty continue to pressure the EU market. Indian mills are focusing more on the domestic market due to better price realisations.

- Meanwhile, Chinese HRC offers to the Middle East stayed firm as bookings were made for end-July shipments ahead of Eid-al-Adha. Indian mills are less active in the ME market, given stronger domestic margins and competitive Chinese pricing.

Leave a Reply