- Indonesian prices steady, South African offers weak

- Domestic prices ease on weak non-power demand

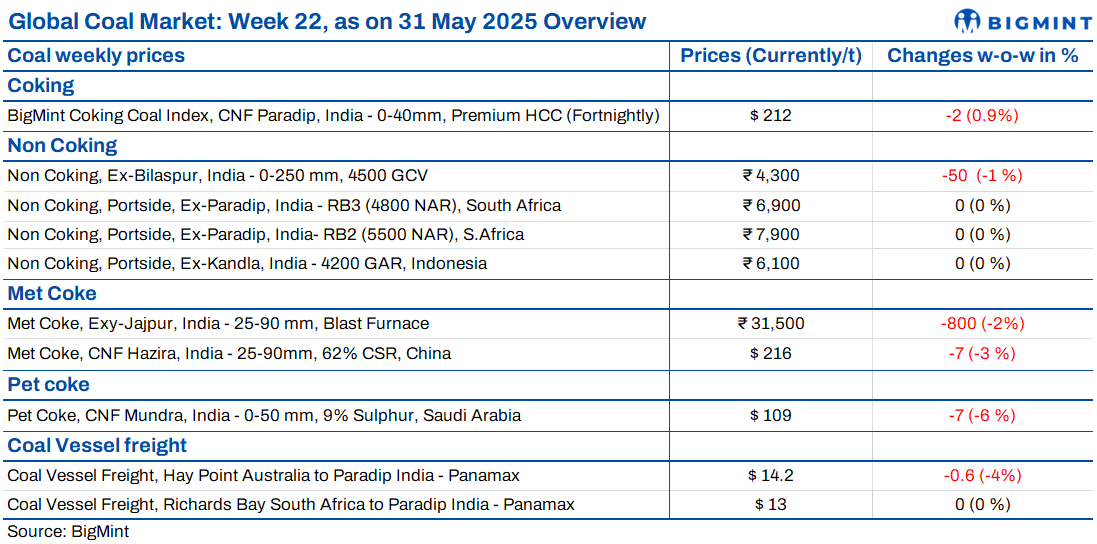

This week, India’s coal market remained largely subdued, reflecting weak demand across both domestic and imported segments. The onset of the monsoon continued to weigh on portside activity, with buyers adopting a cautious, need-based procurement approach. Industrial offtake stayed sluggish, particularly from sponge iron and non-power sectors, while high inventory levels at ports and power plants reduced urgency in the market. Despite stable freight rates on most routes, overall sentiment remained bearish due to limited transactions, oversupply in some regions, and lack of clear demand triggers in the near term.

Indonesian prices steady at Indian ports this week

Indonesian thermal coal prices at Indian ports remained unchanged amid subdued demand and higher vessel arrivals. As of 30 May, the 5000 GAR grade was assessed at INR 7,750/tonne at Kandla. The 4200 GAR stayed flat at INR 6,100/t at Kandla and at INR 6,000/t in Vizag, while 3400 GAR held at INR 4,500/t at Navlakhi. Weak industrial demand, adequate domestic coal stocks, and cautious buying capped trade volumes. On the international front, 5800 GAR dropped by $1.26/t to $75.96/t FOB, while 4200 GAR and 3400 GAR fell to $46.20/t and $32.66/t, respectively, on limited global offtake.

South African offers weak amid monsoon lull

South African thermal coal prices at Indian ports remained under pressure this week, with RB2 (5,500 NAR) assessed flat at INR 7,900/t exw-Gangavaram and RB3 (4,800 NAR) stable at INR 6,900/t. Demand was muted amid the onset of the monsoon, pushing portside prices to near four-year lows. Buyers placed low bids, with limited deals heard – 10,000 t of RB2 were sold at INR 8,100/t exw-Vizag, while 7,000 t got booked at INR 7,900/t in Mangalore. Port stocks rose 2% w-o-w to 15 mnt due to increased arrivals. Weak buying interest and falling global offers continued to weigh on sentiments. Meanwhile, CDRI prices at Rourkela dropped INR 200/t to INR 24,500/t. PDRI ranged between INR 23,350–25,700/t.

Domestic coal prices ease on weak industrial demand

Domestic coal prices in India declined this week amid sluggish industrial demand and limited buying activity. The 4,500 GCV grade dropped by INR 50 to INR 4,300/t ex-Bilaspur, while the 5,000 GCV remained unchanged at INR 4,800/t. SECL’s auction on 26 May saw the allocation of 676,200 t, largely comprising power-grade G11 coal. As most volumes were taken by power plants, demand from the non-power segment stayed subdued. This lack of industrial offtake continued to weigh on prices.

Met coke prices slump to 5-month lows

Indian metallurgical coke (met coke) prices declined further this week, hitting a five-month low amid poor demand and lack of trade. BigMint assessed 25-90 mm BF-grade coke at INR 31,500/t ex-Jajpur, down INR 800/t w-o-w, while Gandhidham prices slipped INR 200/t to INR 30,800/t. Offers as low as INR 29,500/t were reported. Weakened steel prices and muted procurement by mills weighed on sentiment. BigMint’s Steel Composite Index fell 0.6% to 135.8 points on 23 May. Meanwhile, China’s coke prices dropped by RMB 50-55/t due to oversupply. Talks of extending India’s import quota into 2025 may offer future price support if implemented.

China’s met coke market steady, margins turn negative

China’s metallurgical coke market remained broadly stable in the week to 22 May, with Mysteel’s composite price assessed at RMB 1,293.2/t ($179.6/t), nearly unchanged. Despite this, average producer margins turned negative, slipping to a loss of RMB 15/t from a profit of RMB 7/t last week. Losses deepened in Jiangxi to RMB 190/t, while profits in Hebei narrowed to RMB 47/t. Coking coal prices declined by RMB 22.1/t to RMB 1,040.7/t, but most producers had yet to use cheaper feedstock. Market fundamentals stayed weak, and a second round of met coke price cuts appeared likely by month-end.

Imported pet coke market shows mixed trends

The imported petroleum coke market in India displayed mixed pricing trends during the week. US-origin pet coke prices edged up to $106-108/t CFR, compared to $100-102/t in the previous week. In contrast, Saudi-origin offers declined slightly to $109-111/t CFR from $116-118/t. Despite these movements, no transactions were reported as most buyers had already built stocks amid the earlier US-China tariff concerns. While suppliers maintained firm offers, buyers stayed on the sidelines, leading to a subdued trading environment. Market sentiment remained weak due to limited demand and a lack of fresh buying interest.

Australia-India coal freight dips; other routes steady

Panamax coal freight rates to India showed a mixed trend this week. Rates on the Australia-India route declined by $0.6/t to $14.2/t, while Indonesia and South Africa routes held steady at $13.5/t and $13/t, respectively. A surplus of vessels for end-May loadings, along with cautious chartering, softened Pacific basin sentiment. Port stocks rose 2% w-o-w to 15 mnt, reducing fresh enquiries. The Baltic Panamax Index dropped 82 points to 1,208, and the Baltic Dry Index fell by 92 points to 1,296. Overall, weak demand, high inventories, and easing bunker costs pressured freight levels across key routes to India.

Leave a Reply