The South Asian imported scrap market is currently facing a challenging phase marked by weak demand, rising costs, and seasonal slowdowns across key countries.

India’s market is subdued amid sluggish steel demand and a shift towards alternative raw materials, while Pakistan is struggling with high freight charges and hesitant buyers ahead of Eid. Bangladesh is contending with financial and logistical hurdles which are impacting import activity.

Meanwhile, Turkiye sees ample supply pushing prices lower and buyers cautious.

Thus, UK-origin shredded scrap offers remained unchanged d-o-d, while US-origin HMS 80:20 offers to Turkiye stood stable further today.

Market overview

India: India’s imported scrap market remained weak due to sluggish steel demand, tight margins, and rising preference for sponge iron and pellets. Mills showed caution, favoring short-transit cargoes amid monsoon uncertainties.

Shredded scrap offers from the UK/Europe were around $370-375/t CFR, with bids at $360-365/t, while HMS 80:20 was offered at $345-350/t CFR, with buyer bids near $340-345/t. Australian shredded scrap prices at Chennai stood at $360-365/t CFR.

A trader noted that activity was very slow across countries, with lower material inflows. Pakistan’s Qasim port also saw weak activity and low inquiries, while India slowed down ahead of monsoon while the Western countries prepared for summer holidays with reduced factory operations.

Pakistan: Pakistan’s imported scrap market was subdued, weighed down by high freight costs, weak steel demand, and the approaching Eid holidays. Trading activity remained low as mills hesitated to book cargoes, resulting in limited buying interest. UK/EU-origin shredded scrap offers ranged between $380-385/t CFR Port Qasim, but bids stayed slightly lower, around $380-382/t, causing thin trade volumes.

Shipping surcharges caused some cargoes to divert to India, though low Indian prices might lead to these shipments returning to Pakistan. Overall, the market sentiment was cautious with minimal booking activity.

Bangladesh: Bangladesh’s imported scrap market remained under pressure as mills stayed cautious amid an Eid slowdown, LC issues, and rising freight costs. Australian HMS 80:20 was offered at $355-360/t CFR Chattogram, HMS 1 at $365-367/t CFR, shredded scrap at $375-380/t CFR, and bushelings at $385-390/t CFR.

Domestic scrap prices ranged between BDT 53,000-55,000/t ($434-450/t), while rebar prices fell to BDT 82,000-83,000/t ($671-679/t) in Dhaka and BDT 84,000-86,000/t ($686-703/t) in Chattogram. With subdued construction activity and the approaching Eid holidays, market sentiment is expected to remain soft through mid-June.

Turkiye: The Turkish imported scrap market softened slightly as ample supply outweighed weak demand, resulting in reduced buying interest and lower bid levels. Indicative values stayed at or below $347/t CFR, with bids heard at $340/t CFR for US-origin and down to $335/t CFR for EU-origin material. Despite the pressure, sellers held firm on pricing, particularly for EU-origin scrap at around $342/t CFR. However, buyers remained largely inactive, citing oversupply and current price levels as unworkable. Overall, the market sentiment turned increasingly cautious, with bearish undertones growing stronger.

Price assessments

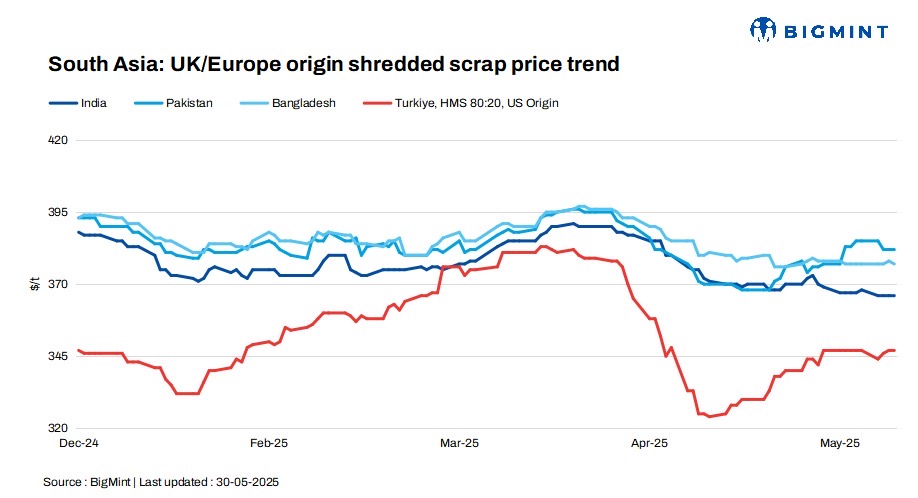

India: UK-origin shredded indicatives were assessed at $366/t CFR Nhava Sheva, unchanged d-o-d.

Pakistan: UK-origin shredded indicatives stood at $382/t CFR Qasim, unchanged d-o-d.

Bangladesh: UK-origin shredded prices were assessed at $377/t CFR Chattogram, unchanged d-o-d.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $347/t CFR Turkiye, unchanged d-o-d.

Leave a Reply