- Vietnamese buyers stay cautious amid bid-offer gaps

- Taiwan’s prices stay firm despite weak rebar demand

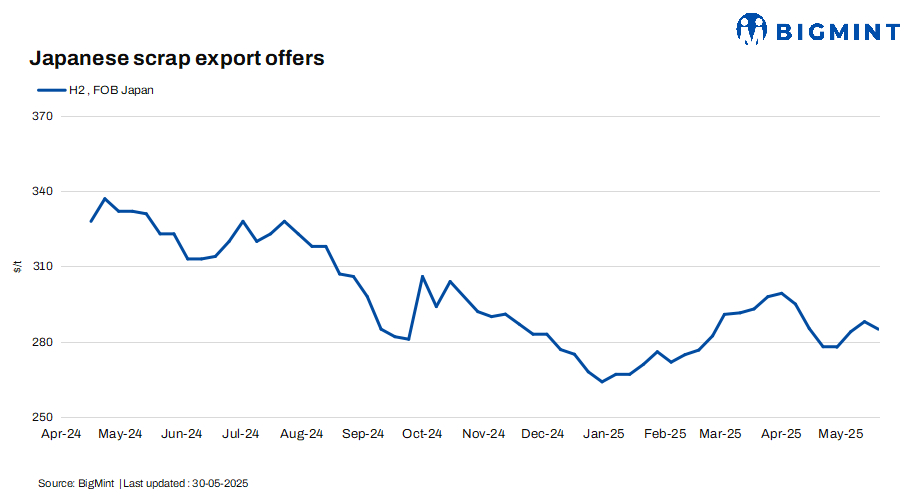

Japanese H2 scrap export prices declined marginally w-o-w amid currency fluctuations and subdued buying interest. BigMint’s weekly H2 assessment stood at JPY 41,100/tonne (t) ($285/t) FOB Tokyo Bay, down JPY 100/t ($1/t) from the previous week’s JPY 41,200/t ($286/t), whereas domestic FAS collection prices for H2 were assessed lower at JPY 40,500/t ($258/t).

The depreciation of the Japanese yen from JPY 142 to JPY 144 against the US dollar led many buyers to adopt a cautious stance, resulting in a slowdown in seaborne trade. With a weaker JPY, sellers showed greater flexibility in pricing and were open to negotiating lower levels compared to last week’s relatively bullish sentiment. However, some sources noted that despite the softer currency, Japanese sellers were more hesitant to make fresh offers, contributing to the market’s overall quiet tone.

According to the latest release from the Japan Iron and Steel Association, the average price of H2-grade scrap iron across three major regions in Japan stood at JPY 38,100/t ($243/t) in the fourth week of May, marking a JPY 100/t ($1/t) decline from the previous week. Regionally, prices fell by JPY 100/t ($1/t) to JPY 37,900/t ($241/t) in Kansai and JPY 42,000/t ($268/t) in Kanto, while those in Chubu remained unchanged at JPY 36,300/t ($231/t).

Other market updates

Vietnam: Vietnam’s imported scrap market remained steady w-o-w, with US-origin HMS 80:20 indicative offers holding at $350/t CFR Vietnam, although market participants pointed to muted buyer interest due to a persistent bid-offer gap. Japanese H2 offers ranged between $325-340/t CFR Vietnam, with tradable levels at around $320-323/t CFR Vietnam.

In Vietnam’s domestic longs market, Hoa Phat Hung Yen Steel increased rebar prices by VND 200/t ($8/t), citing rising billet costs as the main driver. Market participants noted that demand for longs remained strong, underpinned by ongoing robust construction activity.

Market participants also highlighted that a recent issue at a Vietnam-based blast furnace is expected to dampen scrap demand in the near term, with recovery likely to extend beyond the initially expected 1 to 2 weeks.

South Korea: South Korea’s ferrous scrap inventory fell 4% w-o-w to 765,000 t, with the central region up 6% and the southern region down 2%. Large steelmakers kept stocks steady amid production cuts, while small and medium mills faced slow inventory recovery due to rising prices.

Price hikes and incentives have slightly boosted inventory m-o-m, but the market remains unbalanced. Some mills may need to adjust buying ahead of the June holidays and the rainy season. Small and medium mills are expected to increase scrap purchases despite ongoing supply challenges.

Domestic scrap imports remained limited, with under 40,000 t, mainly at Incheon (15,000 t), Gunsan (11,000 t), Jinhae (2,000 t), and Gwangyang (6,000 t). Shipping continued with the vessel ‘JIA HE’ loading 1,000 t at Jinhae and 5,000 t planned at Pohang. With exports continuing alongside unstable scrap supply, the market is closely watching how these trends will impact future prices and domestic availability.

Taiwan: Taiwan’s imported scrap market remained firm this week, supported by rising global prices, while subdued end-user demand limited rebar price gains. US-origin HMS 80:20 scrap was assessed at $300/t CFR Taiwan, and Japanese H2 scrap at $318/t CFR, both up $5/t w-o-w.

Feng Hsin Steel, Taiwan’s largest rebar producer, rolled over its rebar list prices at TWD 17,400/t ($582/t) exw and raised its local scrap procurement prices by TWD 200/t ($7/t) w-o-w in response to stronger seaborne scrap offers.

Despite rising scrap costs, rebar prices lost upward momentum due to shrinking downstream demand during the wet season. Rebar price weakness in mainland China also added to the cautious sentiment in Taiwan’s steel market.

Outlook

Japanese H2 scrap export prices are likely to remain under pressure amid a weak yen, limited buying interest, and cautious seller participation. Regional markets show mixed signals – Vietnam stays range-bound, South Korea grapples with tight supply, and Taiwan faces rising scrap costs but weak rebar demand. Market sentiment is expected to stay subdued in the near term.

Leave a Reply