- US suppliers firm on offers, limited bookings seen

- European scrap supply caps buying interest

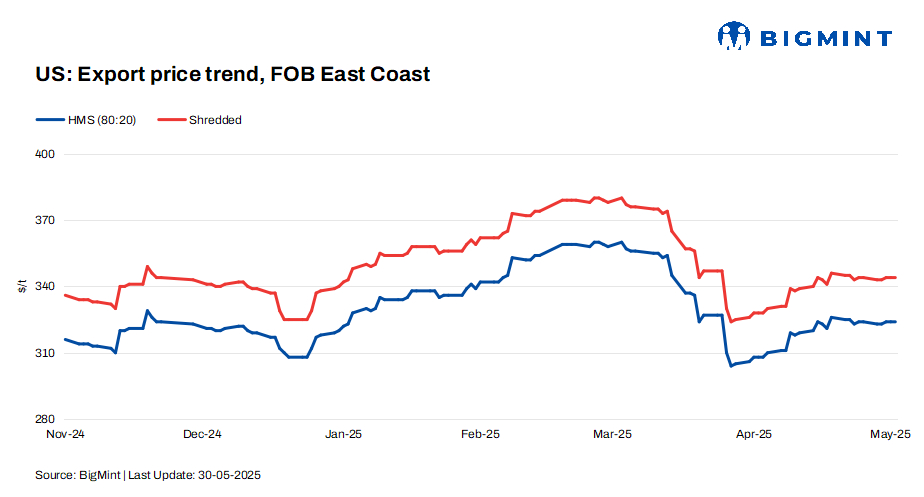

BigMint’s US ferrous scrap export prices remained steady this week. Tight supply, firm seller offers, and selective restocking needs kept FOB East Coast values range-bound. Demand varied across major import destinations, with Turkiye showing modest improvement, while sentiment in Vietnam and Bangladesh stayed weak amid holidays and cautious buying.

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $324/t, stable w-o-w.

- Shredded – $344/t, stable w-o-w.

Key importers

Turkiye: Demand for US-origin scrap in Turkiye showed modest improvement this week, even though overall trading remained limited. Turkish mills, facing low inventories for June shipments, showed willingness to accept slightly higher prices. A recent deal was concluded at $347/t CFR.

US suppliers mostly held firm, offering HMS 80:20 at $350-352/t CFR, supported by tight availability and limited inventories. In contrast, European-origin offers at $338-345/t CFR continued to face resistance from mills, as sellers expected firmer prices ahead of Eid restocking.

Improved domestic long steel sales helped mills absorb the higher scrap input costs, while upcoming Eid al-Adha holidays prompted mills to secure material early. Although activity was not widespread, these factors contributed to a cautiously firmer sentiment in the US-origin scrap market.

Factors limiting buying interest

- Abundant European-origin offers ($338-343/t CFR) weighed on sentiment

- Mills were cautious due to sluggish domestic rebar sales and approaching Eid holidays

- Absence of new US-origin offers reduced the momentum of fresh bookings

Bangladesh: Demand for US-origin HMS 80:20 scrap in Bangladesh remains dull heading into June. Buyers remain cautious amid upcoming Eid holidays 5-15 June, with limited procurement expected until at least 20 June. Bulk offers from the US are heard around $365-370/t CFR, while bids remain lower at $355-360/t, reflecting the subdued buying appetite.

Mills are holding back major purchases ahead of the national budget announcement in June, waiting for clarity on fiscal policies. At the same time, freight issues, especially from Hong Kong, continue to hamper scrap logistics, discouraging fresh bookings.

Mills in Chattogram remain largely inactive, reportedly holding sufficient inventories to cover short-term needs.

Vietnam: Demand for US-origin HMS (80:20) scrap remained weak in Vietnam, with bulk offers at $345-350/t CFR drawing little interest. The assessed price dropped $5/t w-o-w to $335/t CFR. While containerised scrap showed slight gains, bulk cargoes struggled to find buyers amid cautious market sentiment.

Vietnamese mills were hesitant to restock as rebar prices held steady and billet and iron ore prices continued to soften. With no strong trigger from the downstream market, mills preferred to wait, keeping overall scrap demand subdued.

CFR assessments (US-origin HMS 80:20, bulk)

- Turkiye: $347/t, stable w-o-w.

- Vietnam: $340/t, stable w-o-w.

- Chattogram: $376/t, up by $3/t w-o-w.

Outlook

US-origin scrap prices are expected to remain stable in the near term, supported by firm offers from American suppliers. Turkiye could see a pickup in buying activity after Eid, while demand across Asia is likely to stay subdued until late June. The availability of lower-priced European scrap is expected to cap any significant upward movement in global prices.

![]()

Leave a Reply