- Pak, Bangladesh see limited buying ahead of Eid

- Turkiye market stays firm despite weak steel tags

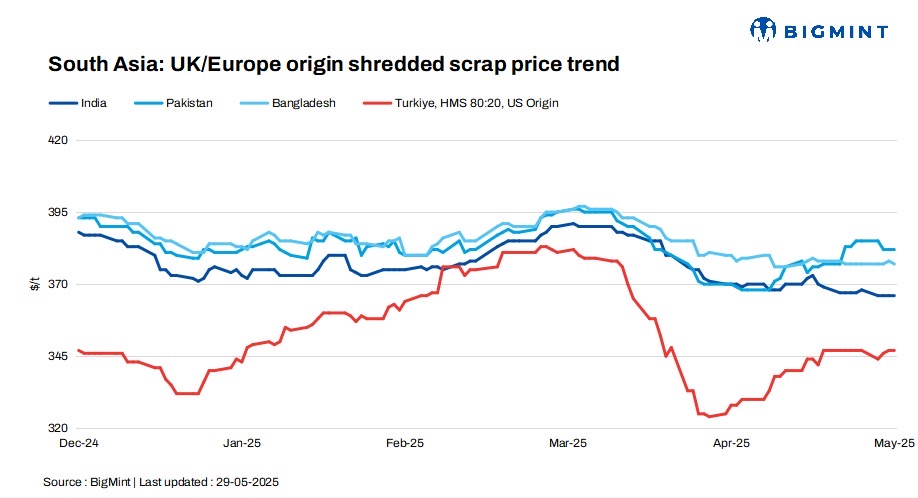

The South Asian imported scrap market experienced subdued activity amid a mix of seasonal slowdowns, logistical challenges, and weak steel demand. In India, mills remained cautious, favouring short-transit cargoes, as margins tightened and alternative raw materials gained traction. Pakistan and Bangladesh saw limited buying ahead of the Eid holidays, with freight costs and credit issues weighing heavily on imports. Meanwhile, Turkiye’s market held firm despite pressure from falling steel prices, as sellers maintained confidence amid cautious buyer interest.

Market overview

India: India’s imported scrap market faced continued pressure from weak steel demand and tight margins, alongside increased preference for sponge iron and pellets. Mills favoured short-transit cargoes due to upcoming monsoon uncertainties.

Shredded offers from the UK/Europe were at around $370-375/t CFR, with bids at $360-365/t CFR. HMS 80:20 was quoted at $345-350/t CFR, while buyers’ bids ranged within $340-345/t.

Australian shredded prices stood at $360-365/t CFR Chennai, and HMS 80:20 was offered at $340-345/t CFR, reflecting cautious buying amid subdued market sentiment.

Pakistan: Pakistan’s imported scrap market saw subdued trade, as mills remained largely inactive ahead of Eid, citing poor end-user demand and rising freight costs. Buying interest was limited, with most participants unwilling to match offers.

UK/EU shredded was offered at $380-385/t CFR, but bids stayed lower, keeping trade volumes thin.

Bangladesh: Bangladesh’s imported scrap market remained under pressure, as mills stayed on the sidelines amid an Eid-related slowdown, letter of credit (LC) hurdles, and rising freight costs. Only limited containerised deals were heard, with PNS at $380-385/t CFR and shredded at $370-378/t CFR. Bulk bookings were largely absent, with buyers wary of high landed costs and soft steel demand.

Mills focused on inventory control rather than fresh imports, while elevated freights from Hong Kong further discouraged buying. Overall, the market is expected to stay quiet until the second half of June.

Turkiye: The Turkish imported scrap market remained steady, with bulk HMS 80:20 assessed at $347/t CFR following a confirmed US-origin deal. Mills faced pressure from falling rebar and billet prices, pushing for lower scrap values amid weak steel demand ahead of the Eid holiday. However, sellers resisted, expecting upcoming restocking and citing firm demand and stable collection costs. While some offers from the EU softened slightly, overall sentiment stayed firm, with sellers unwilling to go below $350/t CFR. The market remained in a stand-off, balanced between buyer pushback and seller confidence in limited scrap availability.

Price assessments

India: UK-origin shredded indicatives were assessed at $366/t CFR Nhava Sheva, unchanged d-o-d.

Pakistan: UK-origin shredded indicatives stood at $382/t CFR Qasim, unchanged d-o-d.

Bangladesh: UK-origin shredded prices were assessed at $377/t CFR Chattogram, down by $1/t d-o-d.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $347/t CFR Turkiye, unchanged d-o-d.

Leave a Reply