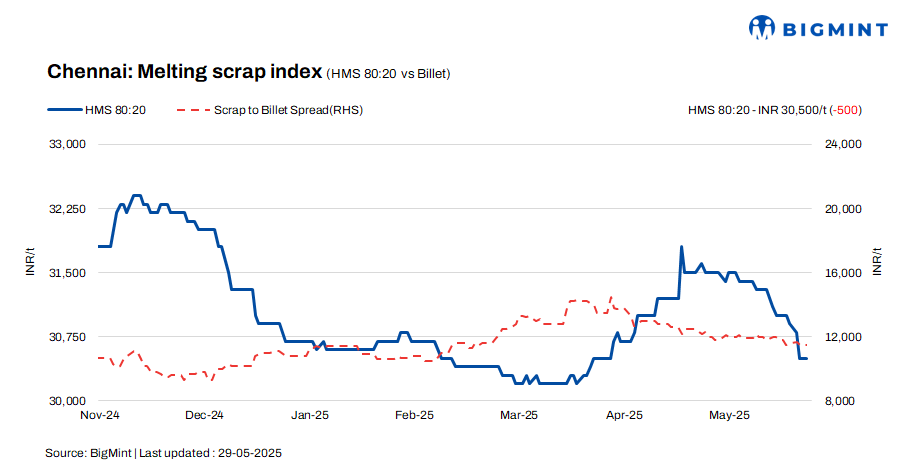

As per BigMint’s latest report, HMS (80:20) prices in Chennai declined by INR 500/t w-o-w to INR 30,500/t, though remained unchanged on a daily basis. Billet prices stood firm at INR 42,000/t d-o-d, reflecting an INR 800/t drop over the week. Similarly, rebar prices maintained stability d-o-d at INR 47,300/t, yet witnessed a weekly dip of INR 500/t. The overall market reflects subdued momentum with selective corrections across key semi-finished and long product categories.

Imported and domestic price trends

A scrap trader reports that current offers for shredded scrap from Australia are quoted in the range of $360-365/t CFR Chennai, while HMS 80:20 offers stand slightly lower at $340-345/t. Market sentiment indicates that mills are showing a stronger preference for booking bulk cargoes over containerized shipments, driven by cost-efficiency and logistical advantages in securing larger volumes amid softening global scrap prices.

In Chennai, domestic HMS (80:20) scrap prices are currently quoted between INR 30,000-30,500/t for spot transactions with immediate payment. For deals involving extended credit terms, rates are marginally higher, ranging from INR 30,500-31,000/t. Market activity indicates that most offers and concluded trades are occurring within the INR 30,000-31,000/t range, reflecting prevailing liquidity preferences and credit-related pricing differentials.

Buyer-supplier sentiments

A mill representative informed BigMint that finished steel demand has weakened over the past few weeks, leading to inventory accumulation of 15-20 days’ worth of rebar at mill level. This surplus stock is exerting downward selling pressure, impacting billet prices, which have dropped by approximately INR 1,500/t over the past month. In parallel, sponge iron prices in Bellary, Karnataka have declined, further prompting Chennai-based sponge manufacturers to reduce their offers, adding to the overall pressure across the semi-finished product segment.

According to a scrap supplier, HMS 80:20 scrap is currently trading in the range of INR 30,000-31,000/t, influenced by varying payment terms. With declining demand for both semi-finished and finished steel, mills are under pressure to reduce scrap purchase prices. Notably, mills that previously cleared scrap payments within 5-7 days are now extending payment cycles to 10-12 days, reflecting tighter cash flow. Additionally, with a recent decline in imported scrap offers, mills have begun booking imported material in bulk to secure inventory for future production needs.

Regional comparison

In the Jalna market of Western India, billet, rebar, and HMS 80:20 prices declined by INR 100/t, now standing at INR 41,600/t, INR 46,500/t, and INR 31,900/t, respectively. The arrival of the monsoon season has dampened construction activity, resulting in reduced demand for both semi-finished and finished steel products. Rebar prices, in particular, have undergone a notable correction of INR 1,000–1,500/t over recent days. In response to weak market sentiment and to control conversion costs, mills have scaled down their scrap procurement prices.

Outlook

Despite the ongoing market slowdown, scrap prices are expected to stay within a relatively tight band in the near term, with potential movements limited to around INR +/- 500/t. These price fluctuations will largely be dictated by evolving demand trends, inventory levels, and overall market sentiment.

Leave a Reply