- Charterers taking a wait-and-watch approach

- High coal inventories at ports reducing fresh inquiries

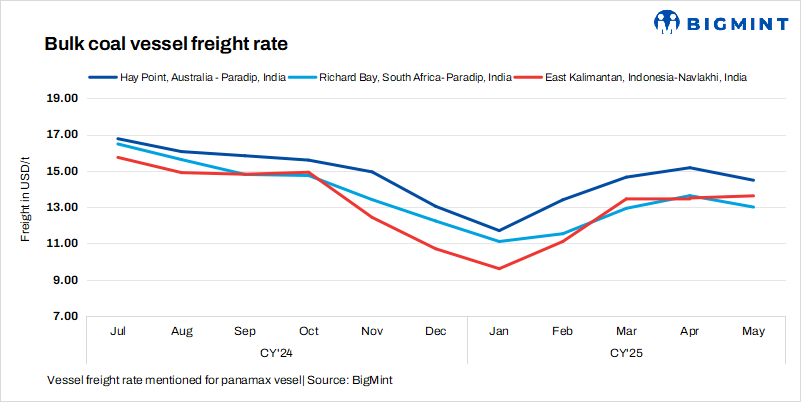

Panamax coal freight rates to India exhibited a mixed trend w-o-w, with the Australia-India route witnessing a decline, while other key routes remained largely stable.

The divergence in freight trends can be attributed to contrasting market dynamics across regions, particularly between the Atlantic and Pacific basins. In the Atlantic, a persistent oversupply of tonnage coupled with subdued cargo demand continues to exert downward pressure on freight rates.

Conversely, the Pacific basin, which earlier showed signs of firming, is now experiencing a softening in sentiment. While cargo demand remains for June loading schedules, an excess of available vessels for end-May laycans is creating downward pressure on prompt freight levels. Charterers, anticipating further rate corrections, are adopting a wait-and-watch approach, prompting owners to revise their offers downward.

Market sentiment is further weighed down by easing freight derivatives and a marginal decline in bunker fuel prices. The softening in bunker costs offers limited support. Overall, the interplay of regional tonnage imbalances, cautious chartering activity, and easing cost indicators resulted in mixed movements in Panamax coal freight rates to India.

Notably, thermal coal stocks at Indian ports rose almost 2% w-o-w to 15 million tonnes (mnt) in week 21 of CY’25, up from 15 mnt last week. The rise was largely due to increased arrivals at several ports, although demand remains subdued overall.

Baltic indices fall w-o-w: The Baltic indices, which indicate trends in vessel demand, dipped w-o-w. The Baltic Dry Index (BDI) was recorded at 1,296 on 26 May, decreasing by 92 points w-o-w. Meanwhile, the Baltic Panamax Index (BPI) fell by 82 points to 1,208 on 26 May against 1,290 on 19 May. Additionally, the Baltic Supramax Index (BSI) was assessed at 974 on 26 May, edging down by 4 points w-o-w.

Route specifications

- Australia-India rates drop: Freights from Australia to India dipped by $0.6/t w-o-w, with BigMint’s assessment indicating that rates for Hay Point Port to Paradip were at $14.2/dry metric tonne (dmt). Sources informed that RINL booked one Panamax vessel from Australia to Gangavaram at $14.4/t, with shipment scheduled for 21-30 June.

- South Africa-India freights unchanged: Freights from the Richards Bay Coal Terminal (RBCT) to Paradip remained firm w-o-w at $13/t due to balanced vessel supply and demand on the route. Limited market activity, driven by India’s preference for domestic coal amid high stock levels, led to reduced volatility. Additionally, no significant logistical disruptions were reported from South African ports, supporting rate stability.

- Indonesia-India freights stable: Freights for coal shipments from East Kalimantan to Paradip stood at $13.5/t, unchanged w-o-w amid subdued cargo demand being matched by ample vessel availability. The onset of the monsoon season in India dampened import activity, limiting rate fluctuations. Despite soft fundamentals, no major disruptions in Indonesian load ports helped maintain rate stability.

Leave a Reply