- Mills may limit imports amid weak billet prices

- Stronger yen may keep Japanese H2 offers high

Imported ferrous scrap prices in Vietnam fell by $5/t w-o-w, as suppliers maintained a bullish stance, attempting to raise offers, while buyers remained cautious due to stable downstream product prices.

Buying interest from Vietnamese mills was moderate. Bulk scrap prices held steady, whereas containerised scrap saw an upward trend. Meanwhile, the domestic longs market remained relatively strong, supported by steady construction demand.

Weekly assessments

- US-origin HMS 80:20 bulk was assessed at $335/t CFR, down $5/t w-o-w.

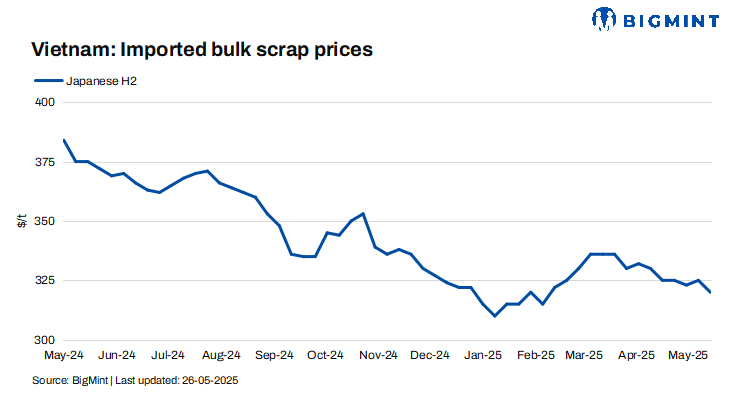

- Japanese H2 was assessed at $320/t CFR, down $5/t w-o-w.

Recent deals

- A deal for HMS 80:20 in 40-ft containers (open origin) was reportedly concluded at $290/t CFR Vietnam

Market commentary

A mill-side source informed that offers for Japan-origin H2 scrap in bulk were heard at $325-330/t CFR Vietnam, although recent deals were concluded below $325/t, with bids falling to $320/t levels. A local mill reportedly booked up to 30,000 t. The upward adjustment in offers was partly driven by the strengthening yen.

Meanwhile, US-origin HMS 1&2 (80:20) in bulk was offered at $350/t CFR Vietnam, with open-origin cargoes indicatively above that level. However, these offers failed to generate buying interest.

A trader mentioned, “Rebar prices have remained largely flat, while billet and iron ore prices are trending downwards. So, mills are not rushing to restock scrap.”

A Japanese supplier said that HS scrap offers softened to $350/t CFR, while bids remained at around $340/t CFR.

Domestic scrap market

- North Vietnam: Domestic scrap bids rose slightly w-o-w to VND 8,500-8,900/kg ($327-339/t), excluding VAT.

- South Vietnam: Prices ranged from VND 7,700-8,000/kg ($304-331/t) excluding VAT, stable from the previous week.

In Vietnam’s domestic longs market, Hoa Phat Hung Yen Steel raised rebar prices by VND 200/kg ($8/t), attributing the increase to higher billet costs. Market participants observed that demand for longs remains robust, supported by active construction activity.

Outlook

Vietnam’s imported scrap market is likely to remain under pressure in the near term, as buyers continue to resist higher offer levels amid weak billet and flat steel prices. Unless finished steel prices recover meaningfully, mills are expected to adopt a cautious procurement strategy, especially with ample inventory levels.

However, rising domestic scrap prices and ongoing strength in construction activity could lend some support to import demand, particularly if regional suppliers adjust offers more competitively. The Japanese yen’s movement will also be a key factor influencing H2 scrap offers in the coming weeks.

![]()

Leave a Reply