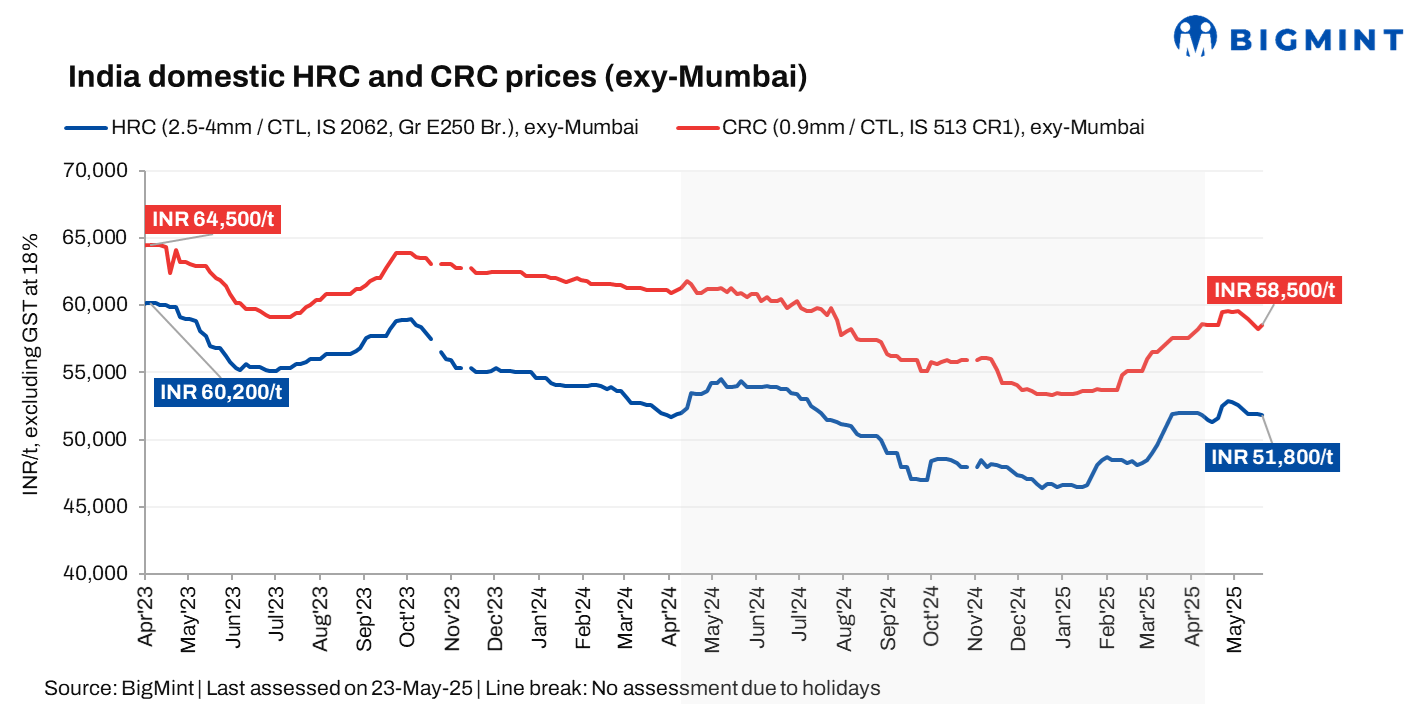

Market sees falling demand with monsoon onset: Market demand has started to decline with the onset of the monsoon season, as several regions have already begun experiencing rainfall. This seasonal shift has increased pressure on sellers to offload existing inventory particularly in the cold rolled coil (CRC) segment as buyers are looking to reduce stock levels in anticipation of logistical and storage challenges typically associated with the monsoon period.

“The market is currently experiencing a slowdown in demand as the monsoon season approaches, leading to a natural deceleration in construction and related activities. Adverse weather conditions and labour shortages have further impacted project execution, contributing to reduced consumption. Additionally, liquidity constraints are weighing on purchasing capacity. In anticipation of potential price corrections or support from mills, many buyers have temporarily paused their procurement activities, opting to wait for more favorable pricing conditions,” a market participant noted.

Import trends: India’s bulk imports of HRCs and plates touched 1,71,834 t as of 19 May, based on vessel line-up data from BigMint. The same totalled 306,260 t in April 2025 and 408,762 t in March 2025. Around 24,238 t of additional cargo are expected by May-end.

Export trends: Export offers for Indian HRCs of grade S275 to the European Union (EU) declined by $10/t w-o-w, and are now being quoted at $630–635/t CFR Antwerp ($580–585/t FOB eastern Indian port), compared to last week’s $640–645/t CFR. Despite the price correction, trading activity in the region remained limited.

Meanwhile, Chinese HRC offers to the Middle East (ME) remained within a narrow range due to the seasonal summer slowdown in demand. Japan, however, secured bookings for HRC shipments to the region which are scheduled for late July. Indian mills have refrained from actively offering to the ME market, citing stiff competition from Chinese suppliers and more attractive domestic realisations.

Outlook

The Indian HRC market is likely to face downward price pressure in the near-term, due to declining demand ahead of the monsoon, labour shortages, and liquidity issues. Buyers are seen deferring purchases, expecting mill price adjustments. Exports will also remain challenged by subdued EU demand and competitive Chinese pricing in the Middle East.

Leave a Reply