- Premiums surge up to 51% at OMC’s chrome ore auction

- Tsingshan’s ferro chrome tender price remains firm m-o-m

Indian high-carbon ferro chrome (HC60%, Si:4%) prices were largely stable this week, down marginally by INR 100/t ($1/t) in comparison to the assessment on 14 May. Prices were steady w-o-w, as market activity was on hold following the conclusion of OMC’s chrome ore auction.

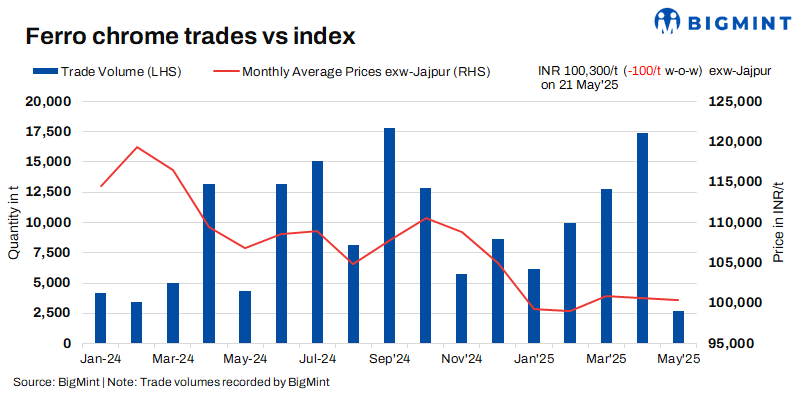

High-carbon ferro chrome (HC60%, Si:4%) prices in India were at INR 100,300/t ($1,171/t) exw-Jajpur, as per BigMint’s assessment on 21 May. Approximately 1,800 t of material were traded in this assessment window at INR 100,200-100,500/t (1,170-1,173/t) exw.

For low-silicon high-carbon ferro chrome, prices fell by INR 1,000/t ($12/t) w-o-w to INR 104,500/t ($1,220/t) exw-Jajpur. Tags stayed unchanged w-o-w for low-carbon (C:0.1%) ferro chrome at INR 201,000/t ($2,346/t) exw-Durgapur.

Market highlights (15-21 May 2025)

Market silent following OMC’s chrome ore auction: At OMC’s chrome ore auction on 19 May, 62,200 t were sold out of the 93,100 t offered. Bids for grades above 48% surged by 3-50% (INR 633-11,324/t) m-o-m, while other grades saw a slight increase of up to 3%. Premiums over the base prices reached up to 51%.

Following this, key sellers in the domestic market paused offering material to analyse cost dynamics, particularly of chrome ore. A prominent seller informed BigMint, “The rise in bids is mainly due to stocking up of material ahead of monsoons. Had demand been strong, the entire offered volume would have been sold out.”

FACOR’s ferro chrome auction reflects market stability: At yesterday’s ferro chrome auction by FACOR, the bigger lot of 10-150 mm fetched an H1 price of INR 100,300/t exw, above the base price of INR 99,500/t exw. Compared to the previous 28 April 2025 auction, prices saw a slight uptick of INR 800/t m-o-m.

The auction outcome reflected the current market stability, as prices have been largely steady for the past several weeks.

Tsingshan’s tender price unchanged m-o-m: Tsingshan kept its ferro chrome tender price stable m-o-m at RMB 8,095/t ($1,124/t) DAP, including taxes, for June 2025 deliveries.

In the Chinese domestic market, prices stayed largely steady w-o-w amid weak downstream demand and cautious steel mill purchasing. Despite positive US-China tariff developments boosting the stainless steel sector, the ferro chrome market saw limited impact. Chrome ore prices stayed higher due to tight inventories, pressuring producers’ margins and slowing production resumption. Steel mills maintained conservative procurement strategies, extending inventory cycles and avoiding large-scale restocking.

India stainless steel prices inch down: Prices of stainless steel 304-grade hot-rolled coils (HRCs) edged down by INR 2,000/t ($23/t) w-o-w to INR 184,000/t ($2,148/t) exw-Mumbai. Nickel prices on the London Metal Exchange (LME) dipped 2.1% w-o-w to $15,605/t, and Asian nickel pig iron (NPI) tags also declined. Despite steady pricing for most stainless steel products, market activity slowed with the onset of the rainy season.

Outlook

With the recent hike in domestic chrome ore prices, offers in the coming days may rise, but this will largely depend on acceptance from buyers.

For China, the outlook remains subdued, with weak demand, cautious buying, and restrained steel production likely to keep ferro chrome prices and market activity under pressure in the near term.

Leave a Reply