- Tight vessel supply supports higher freights

- Baltic indices up, underscore vessel demand

Dry bulk iron ore freight rates on the India-China route showed an upward trend this week, primarily due to a tightening vessel supply trend amid consistent cargo demand. Limited availability of spot tonnage, especially within the Pacific Basin, has intensified competition among charterers, leading to firming up of freights. This tightening in supply is giving shipowners stronger leverage in negotiations, especially for longer-haul voyages from India.

In addition, seasonal cargo flows are contributing to the freight increase. Pre-monsoon iron ore shipments from key Indian east coast ports such as Paradip and Haldia have picked up pace, driving a surge in regional demand for vessels. This seasonal uptick, coupled with constrained fleet availability, is reinforcing upward pressure on freight levels across the sector.

The rise in iron ore Capesize freight rates was primarily driven by increased cargo demand from key mining companies such as FMG and Rio Tinto. This surge in volume, particularly for early June laycans, resulted in heightened chartering activity, effectively tightening vessel availability in the Pacific Basin and exerting upward pressure on freight levels.

Additionally, market sentiment received a boost from modest gains in forward freight agreements (FFAs) observed during late Asian trading hours. These derivative market movements enhanced pricing expectations and bolstered owner confidence. While freight offers initially softened throughout the trading session, consistent cargo demand, coupled with improved FFA signals, helped support firmer rate levels through the day.

Factors influencing freights

- Baltic indices rise w-o-w: The Baltic indices, indicating trends in vessel demand, remained positive w-o-w. The Baltic Dry Index (BDI) was recorded at 1,388 on 19 May, increasing by 89 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 2,018, up by 309 points w-o-w. Meanwhile, the Baltic Supramax Index (BSI) inched up by 9 points w-o-w to 978.

- China’s iron ore spot prices dip $1/t w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $101.1/t CFR on 20 May, down by $1/t w-o-w. The decline was in fresh trades driven by steel mills aiming to preserve margins through price cuts and purchases only on need basis. According to reports, demand for lower-grade fines remained strong, and relying on medium and high-grade materials is unsustainable, as margin depends on cost reductions and efficiency improvements.

Route-wise updates

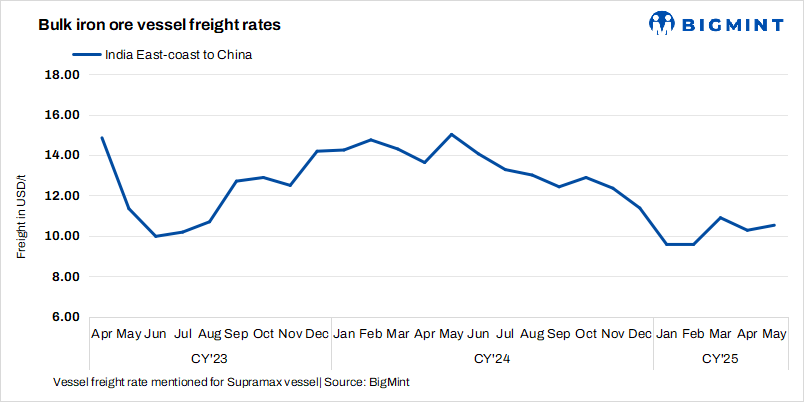

- India-China: Freights from the Indian Ocean to China were recorded at $10.8/t, edging up by $0.3/t w-o-w. According to market sources, a Supramax vessel was recently fixed at approximately $9.5/t for a prompt shipment, while several other fixtures remain under negotiation, indicating ongoing activity and firming sentiment in the region.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $7.7/t on 21 May, rising by $0.3/t w-o-w. According to sources, major Australian miners Rio Tinto and FMG booked Capesize vessels from a Western Australian port to Qingdao at around $7.55-8.25/t. Shipment is scheduled for 31 May-7 June.

- Brazil-China: Freights for Capesize vessels from Brazil to China fell this week. Rates from Tubarao to Qingdao Port were assessed at $18.5/t on 21 May, marginally up by $0.1/t w-o-w. As per sources, Vale booked a Capesize vessel from Tubarao to Qingdao at $18.60/t for the shipment period of 1-5 June.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao increased by $0.6/t w-o-w to $14.2/t on 21 May. Sources informed BigMint that Ore and Metal booked one Capesize vessel from Saldanha Bay to Qingdao at around $14.35/t, with shipment scheduled for 6-10 June.

Leave a Reply