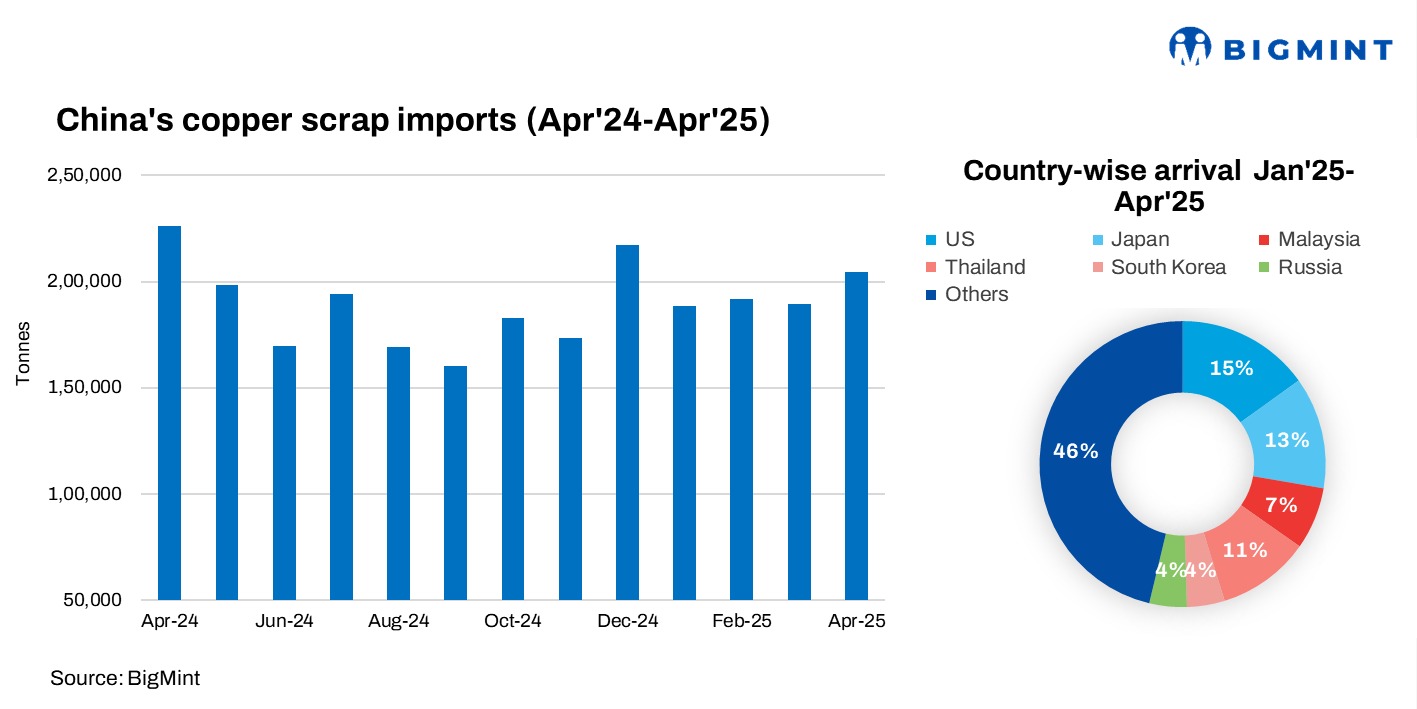

China’s copper scrap imports dipped slightly in the first four months of 2025, reflecting growing uncertainty and shifting trade dynamics. A key reason behind the softening is reduced supply from the United States, following the impact of higher tariffs. Many Chinese traders have pulled back from purchasing US-origin scrap, leading to a significant drop in shipments.

US volumes drop, market sentiment weakens

The sentiment among buyers remains cautious, with the US once a major supplier, now seeing exports fall sharply as buyers steer away due to tariff-related risks. This retreat from US material—down nearly a quarter compared to last year—has left a noticeable gap in the market and heightened concerns about long-term availability.

Thailand steps up amid changing flows

To offset this shortfall, Chinese importers have shifted attention to Thailand. Imports from the country have surged as traders look for cost-effective and reliable alternatives. Thailand has become a preferred origin, especially as Japanese scrap remains expensive and logistical delays continue at Malaysian ports. The change reflects both price sensitivity and a growing need for logistical stability.

Subtle shifts from other suppliers

Japanese exports held relatively steady, though on the higher side cost-wise, making them less attractive in bulk. Imports from Malaysia, meanwhile, have faced challenges, with volumes dipping due to congestion at key ports. Russia and South Korea continued to supply, but with minimal change in sentiment or flow.

Country-wise trends (Jan-Apr 2025):

US: Still a key origin, but shipments fell sharply by 23.9% to 117,056 tonnes as buyers avoided tariff-hit material.

Thailand: Strong rise in shipments, up 42.2% to 81,644 tonnes, now seen as a leading alternative due to smoother logistics and competitive prices.

Japan: Shipments were relatively stable at 98,230 tonnes, down just 1.0%, but high prices continued to limit larger buying interest.

Malaysia: Imports dropped 13.7% to 54,705 tonnes as port delays reduced shipment interest.

Russia & South Korea: Modest and relatively steady volumes, with Russia down 3.1% to 32,933 tonnes and South Korea down 3.0% to 33,062 tonnes.

Outlook: Supply to remain tight

Looking ahead, market participants are wary of further tightness in the second half of the year unless China removes the remaining 10% import tariff on US-origin scrap. The mood remains cautious, with buyers focusing on flexibility and risk mitigation as trade flows continue to evolve.

Leave a Reply