- Realty investment drops by 11.5% y-o-y in Apr

- Steel supply firm, but oversupply risks persist

Horizon Insights: China’s macroeconomic landscape in April 2025 delivered another round of soft indicators, according to National Bureau of Statistics (NBS) data, reinforcing concerns over a slow and uneven recovery in ferrous demand. While steel output remained broadly stable, subdued activity in key steel-consuming sectors such as real estate and infrastructure dampened the market’s sentiment.

Construction activity remains below expectations

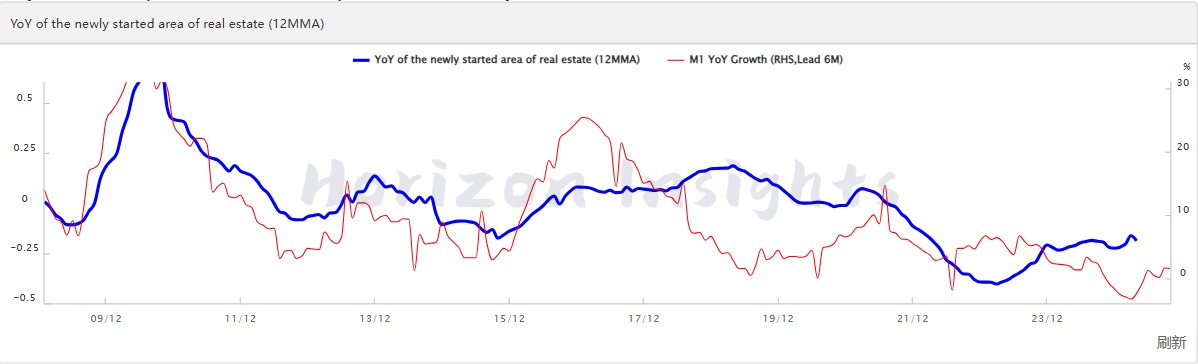

The real estate sector remained at a critical pressure point, with investments falling by 11.5% y-o-y this year and new construction starts slumping 22.3% y-o-y in April. On the pricing front, Tier 1 new home prices remained flat m-o-m, while secondary home tags inched down 0.2%, indicating lacklustre end-user interest and persistent inventory overhang.

Steel output stable, but risks of overproduction prevail

Crude steel production remained largely unchanged y-o-y at 86.02 mnt in April, while pig iron output edged up 0.7% y-o-y to 72.58 mnt. For cumulative January-April 2025, crude steel production totalled 345 mnt, marginally higher by 0.4% y-o-y. Pig iron production totalled 289 mnt, up by 0.8% from the same period this year. With no clear production limits in place and margins staying steady for now, mills seemed focused on keeping output high before the seasonal slowdown begins.

Muted sentiment across value chain

Despite stable supply, downstream steel demand showed little spark. Majorly, CRC-HRC spreads remained narrow, and end-user buying was cautious, with market participants refraining from restocking. The market saw a slight lift in demand in the early days of week 20, but the momentum again subsided at the end of the week. Export demand is expected to be moderate from mid-June, especially as front-loaded bookings wane and seaborne appetite adjusts.

Outlook

The near-term outlook for steel remains tepid. While production may stay elevated through early summer, demand-side signals remain weak, particularly from construction and infrastructure for finished steel. Without a fresh round of policy easing or fiscal push, steel prices may stay range-bound, with October rebar contracts under pressure amid oversupply concerns and faltering real demand.

Note: This article has been written in accordance with a content exchange agreement between Horizon Insights and BigMint.

Leave a Reply