- China’s Crude steel output slows but exports firm up

- Manufacturing PMI contracts to 16-month low

- Realty woes continue, automotive sales decline

Morning Brief: China’s macroeconomic indicators presented an uneven picture in January-April 2025 (4MCY’25). Although crude steel production remained higher y-o-y, growth moderated m-o-m in April. However, steel exports and iron ore imports showed robust gains m-o-m. Meanwhile, performance faltered across the manufacturing, infrastructure, and realty segments.

BigMint goes behind the scenes.

Crude steel output growth softens: Following a 7% m-o-m decline in April, the growth in crude steel production during 4MCY’25 moderated to 0.4% y-o-y from 0.6% in the first quarter. A struggling realty segment and contraction in manufacturing activity pressured crude steel production, despite mills logging robust profits, strong export bookings, and decent domestic demand.

In tandem, pig iron production stood 0.8% higher y-o-y at 289 mnt in January-April.

Steel exports rise further: In April, China’s steel exports increased 13.4% y-o-y to 10.46 mnt, leading to a stronger 8.2% y-o-y growth in 4MCY’25 compared to 6.3% in 3MCY’25. Importers kept procurement steady, with overseas manufacturers boosting production to make the most of the 90-day pause on US tariffs. Additionally, China’s predatory pricing tactics continued to give it an edge in the seaborne market.

Meanwhile, the decline in China’s steel imports deepened to 13.9% y-o-y in 4MCY’25 compared to 11.30% in 3MCY’25, possibly due to manufacturing slowdown.

Dip in iron ore imports narrows: While China’s iron ore imports remained lower by 5.5% y-o-y in 4MCY’25, the gap shrank from 7.8% seen in 3MCY’25. Amid healthy margins, mills stepped up their bookings of seaborne cargoes in April. Additionally, reports suggest that the rise could be due to mills compensating for lower imports in March, which were due to cyclone-related supply disruptions in Australia.

Coal imports drop over 5% y-o-y: The drop in coal imports widened to 5.3% in 4MCY’25 compared to 0.9% in 3MCY’25. Imports continued to fall in 4MCY’25 amid a 6.6% uptick in domestic production. Additionally, thermal coal-based power generation also fell 4.1% in the same period, indicating weaker requirement for power coal.

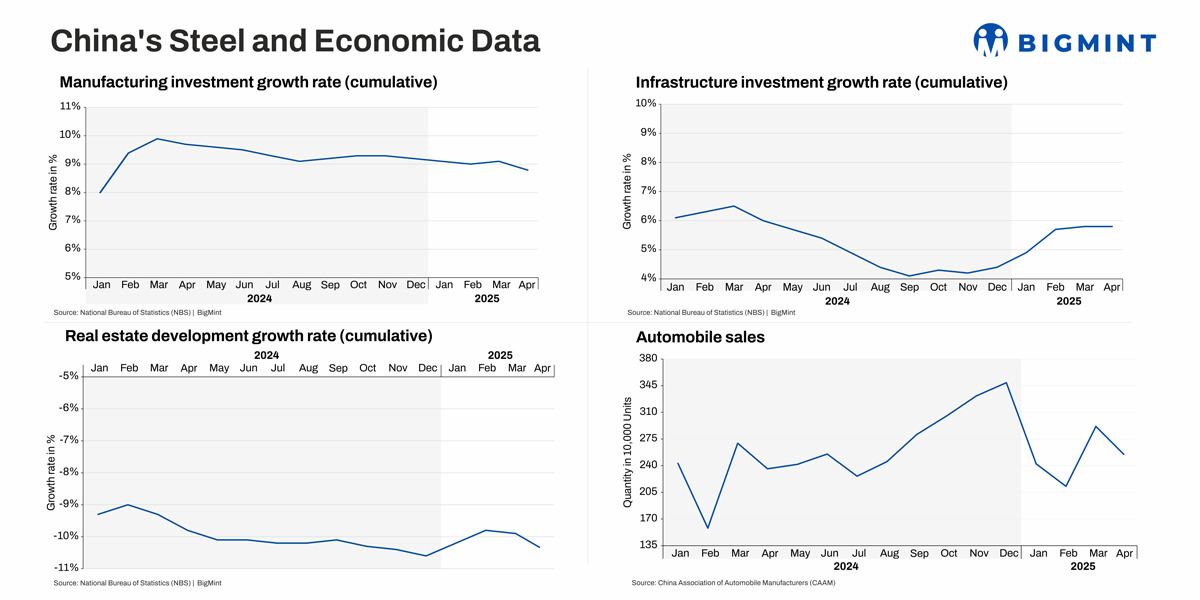

Manufacturing investment growth slides: Manufacturing investment expanded by 8.8% in April, the first time since January 2024 that the metric slipped below the 9% mark. Similarly, the manufacturing purchasing managers’ index (PMI) dropped to 49 points, a 16-month low, from 50.5. A PMI of below 50 reflects contraction in factory output.

The automotive segment also reflected a slowdown in production and sales in April. The growth in automobile production softened by 13% y-o-y in 4MCY’25 from 14.5% in 3MCY’25. Sales also fell to 2.6 million units in April from 2.9 million in March.

However, new energy vehicles (NEVs) remained a bright spot, with output and sales climbing up 48.3% and 46.2% y-o-y, respectively, in January-April.

Moreover, exports rose a measly 2.6% y-o-y to 517,000 units in April, while the total in 4MCY’25 stood at 1.9 million units, up 6% y-o-y.

Infra investment remains range-bound m-o-m: Infrastructure investment growth remained unchanged m-o-m at 5.8% in April, but the non-manufacturing PMI, which covers construction, dipped m-o-m to 50.4 from 50.8. It seems that infrastructure activity was moderately sluggish compared to the previous month, though a stark slowdown did not occur.

However, y-o-y, the growth was slower at 5.55% in 4MCY’25 compared to 6.23% in 3MCY’25.

Realty remains depressed: The drop in real estate investment growth sharpened to -10.3% in April against – 9.9% in March, while y-o-y, the average decline in January-April deepened to -10.1% against -9.4% in the first quarter. Additionally, cement production fell a wider 2.8% in 4MCY’25 against 1.4% in 3MCY’25.

However, there were faint signs of positivity. Property sales by floor area dropped 2.8% y-o-y in 4MCY’25, improving from the 3% in January-March, while new construction starts slumped by a slower 23.8% versus 24.4% in 3MCY’25.

Outlook

Chinese steel production may remain stable in the short term, amid healthy mill margins, easing trade tensions with the US, and moderate demand. Given that the typical off-season is approaching, there may be some urgency on the mills’ part to fill up their order books as much as possible.

Additionally, some suggest that output cuts may not be enforced immediately, as the steel industry is currently on a shaky footing. In the long term, however, production may weaken, mirroring the depression in demand. As such, production sentiment remains strong in the near term.

On the consumption front, it seems that the uncertainty regarding the tariffs and trade war pressured market confidence. While sentiment may improve with the recent trade war de-escalation, fiscal support measures, and lending rate cuts, a turnaround seems remote in the short-to-medium term. The property segment, in particular, may continue to underperform.

Leave a Reply