- IF-route long steel tags down by INR 100-600/t

- Flats volatile, drop by INR 500/t in some regions

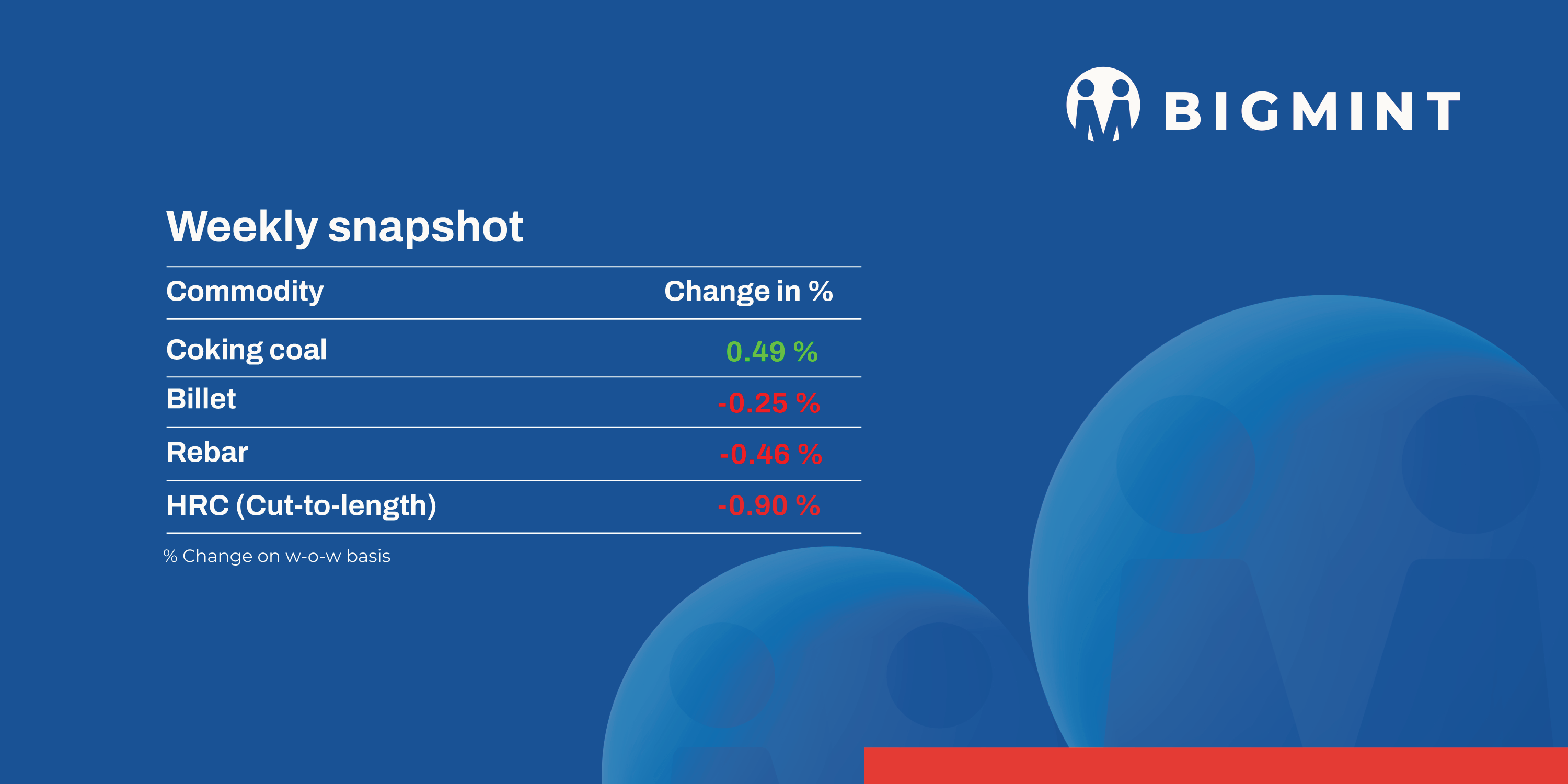

Domestic induction furnace finished long steel offers saw a downward trend, falling by INR 100–600/tonne (t). HRC and CRC trade reference prices also remained volatile, dropping by up to INR 500/t in key markets.

Iron ore and pellet

- BigMint’s bi-weekly domestic pellet (Fe63%) index fell by INR 100/t ($1/t) w-o-w to INR 9,700/t ($116/t) DAP Raipur on 16 May. Raipur-based pellet producers kept offers for Fe 63% (+/- 0.5%) stable at INR 9,600-9,700/t ($112-113/t) exw. Around, 55,000 t trades took place this week in the Raipur region.

- An India-based pellet maker recently concluded an export deal for 50,000 t (Fe61%, 2.5% alumina) through a tender. As per buyer sources, the deal was heard to have been closed at around $93-94/t FOB India. The tender received a positive response following the recent hike in global iron ore prices. Spot prices of iron ore fines in China increased by $4/t w-o-w to $102/t CFR on 15 May.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index increased by $3/t w-o-w to $62/t FOB east coast, India, on 15 May. Trade activity in the Indian Ocean remained moderate, and inquiries increased with the northward march of prices. Exporters dealing in Fe 57% grade fines reportedly offered discounts of 20-22% compared to the global index. Exporters pointed to an overall positive trend, with deals for nearly 350,000 t concluded during the recent price rally.

Coal

- India’s premium hard coking coal index (PHCC) increased by $8/t to $214/tonne CNF Paradip, led by limited availability of Australian cargoes. A 25,000-tonne Goonyella shipment was booked at $214–215/t CFR for June loading. However, many buyers refrained from booking at current prices, anticipating a possible softening due to poor steel margins. Some buyers opted for Canadian alternatives. Despite the price rise, demand remained weak, and any further upside may be capped by resistance from Indian steelmakers.

- South African thermal coal prices at Indian ports declined due to weak demand from sponge iron units and sufficient stock availability. RB2 (5500 NAR) fell by INR 50/tonne to INR 8,250/tonne ex-Gangavaram, while RB3 (4800 NAR) dropped to INR 7,150/tonne.

- Domestic coal prices eased as ample supply from SECL auctions met limited demand. The 4500 GCV grade dropped by INR 150 to INR 4,350/tonne ex-Bilaspur, while 5000 GCV fell to INR 4,800/tonne. SECL conducted two spot auctions on 6–7 May, allocating 784,350 tonnes across six grades, with G11 forming 52% of the total. Buyers showed reduced participation due to sufficient existing inventory and weak downstream requirements.

Ferrous scrap

- Imported scrap market remained sluggish overall with shredded prices stable at $369/t CFR, slightly down from $370/t last week. Trade was limited as wide bid-offer gaps persisted throughout the week. While inquiries were steady, buyer expectations stayed lower than offered levels, preventing deal closures.

- HMS 80:20 was offered at $350-355/t CFR, but buyers resisted below $350/t. Weak steel demand and unclear price direction kept sentiment cautious and bookings limited. Additional pressure came from rising freight costs and a gradual shift by buyers toward more cost-effective alternatives such as sponge iron and pellets.

- Around 11,000-12,000 t of imported scrap were booked in India this week. This included 3,000-4,000 t of HMS 80:20 at $350-361/t CFR, about 4,000 t of shredded scrap at $365-375/t CFR, and 1,500-2,000 t of HMS-PNS mix at $358/t CFR. The remaining volumes comprised turnings, cast iron, AB bundles, and HMS bundle mix.

Ferro alloys

- Silico Manganese:Indian silico manganese prices edged up by INR 500/t ($6/t) w-o-w to INR 70,200-70,900/t ($820-828/t) in the key regions of Durgapur, Raipur and Vizag. Domestic silico manganese prices edged up slightly w-o-w despite weak demand from steel mills. The withdrawal of discounts by some smelters supported the price rise. Falling raw material costs had minimal effect on overall production expenses, keeping output steady.

- Ferro manganese: Indian ferro manganese (HC 70%) prices were largely stable with a slight decline of INR 100/t ($1/t) w-o-w to INR 71,900/t ($840/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, slipped by INR 50/t ($1/t) to INR 72,250/t ($844/t). The market maintained a cautious tone this week, with participants adopting a wait-and-watch approach amid uncertain demand and pricing trends.

- Ferro silicon: Indian ferro silicon prices were largely steady with a slight decline of INR 400/t ($5/t) w-o-w to INR 94,700/t ($1,106/t) exw-Guwahati. However, prices in Bhutan stood firm to INR 95,300/t ($1,113/t) exw. Trades, including bulk deals, were concluded at lower values in this assessment window, which led to slight a drop in prices w-o-w.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices were unchnaged w-o-w at INR 100,400/t ($1,173/t) exw-Jajpur. Amid restricted supply and low trading activity in the domestic market, prices held steady with no significant fluctuations observed this week.

Semi-finished

- Indian semi-finished steel prices showed mixed trends as per BigMint’s assessment. Domestic billet prices in some key locations decreased by INR 100-400/t across regions While, other regions showed positive trends by increasing 50-500/t. Similarly, sponge iron prices also showed a fluctuating trend, almost all key locations moved down by INR 100-550/t, with a major decrease of INR 550/t seen in the Durgapur region. While only Raigarh and Mandi Gobindgarh showed increase of 100-300/t.

- Indian DRI export offers decreased by $7/t for CPT Raxaul, to $339/t while, CPT Benapole offers decreased by $7/t to $345/t.

- SAILs Rourkela Steel Plant (RSP) auctioned 6,000 t of steel-grade pig iron on 13 May, with 1,500 t booked at a base price of INR 32,800/t exw. This marks an INR 700/t drop from the previous auction on 6 May, where 900 t were booked at INR 33,500/t exw.

NMDC’s Nagarnar Steel Plant conducted auction for 10,000 t of steel-grade pig iron (for road transport) on 14 May. Of the total offered quantity, 4,500 t were booked at the base price of INR 32,500/t — INR 500/t lower than the bids at its 5 May auction, where, out of the 10,000 t offered, 1,500 t were booked at the base price of INR 33,000/t (road transport).

Finished longs

- IF-rebar:Induction furnace-route rebar prices declined w-o-w due to weak market demand. Buyers mainly purchased as per immediate needs, leading manufacturers to lower their offers to push sales. However, retailers remained cautious and avoided bulk buying, waiting for more clarity on price trends. As a result, mills started facing sales pressure, and inventory levels have risen to about 10–12 days. In the near term, prices are expected to remain largely range bound.

- On a weekly basis, rebar prices declined in the range of INR 100-600/t across regions except in Goa and Hyderabad where the tags were up by INR 400/t and 1,000/t respectively as per BigMint assessments.

- The trade reference price of IF-route Fe 500 grade, 10-25 mm rebar was assessed at INR 43,400-43,800/t exw Raipur, and at INR 48,000-48,600/t exw Jalna.

- Trade reference price of heavy structural steel of base size 150mm stood at INR 45,200-45,500/t exw Raipur.

- Trade reference prices of wire rods hovered aat INR 43,300-43,800/t ex Raipur.

- BF-rebar: Trade-level blast furnace (BF) rebar prices declined on a weekly basis across key Indian domestic markets, driven by subdued demand and weak market sentiments. The prevailing uncertainty has led market participants to adopt a cautious approach, opting to stay on the sidelines.

Trade-level BF rebar prices edged down by INR 300/t w-o-w to INR 56,400/t exy-Mumbai, as per BigMint’s assessment on 16 May 2025. Prices are exclusive of GST at 18%. - In the projects segment, prices dropped w-o-w to INR 54,500-55,500/t FOR Mumbai amid disparity between bid and offers. End-users procured only on urgent basis amid weak market sentiments and in anticipation of further price drops.

Flats

-

- Trade-level prices of hot-rolled coils (HRCs) fell by up to INR 500/t ($6/t) w-o-w to INR 51,900-53,500/t ($609-627/t) across markets. Cold-rolled coil (CRC) prices declined by up to INR 600/t ($7/t) w-o-w to INR 57,000-61,000/t ($668-715/t).

- Market demand remains weak, with buyers making purchases only to meet immediate requirements. Liquidity is also constrained, as most new sales are on credit and payment recovery continues to be slow.

- India’s bulk imports of HRCs and plates touched 70,025t as of 12 May, based on vessel line-up data from BigMint. The same was 3,06,260t in April 2025 and 4,08,762t in March 2025.

- Indian HRC (S275) export offers to the European Union (EU) declined by $5/t w-o-w, settling at $640–645/t CFR Antwerp ($590-595/t FOB eastern Indian port), compared to $650-655/t CFR last week. Despite the price drop, trading activity in the region remained subdued, as buyers stayed cautious due to competitive pricing from European mills within their domestic markets, according to sources.

- Meanwhile, Chinese HRC offers to the Middle East (ME) remained within a stable range in a recent transaction. Indian mills are currently less active in the ME market due to strong competition from Chinese suppliers and better price realisations in the domestic market.

Leave a Reply