- Turkiye scrap prices firm as US-China trade tensions ease

- Wide bid-offer gaps limit deal closures in India

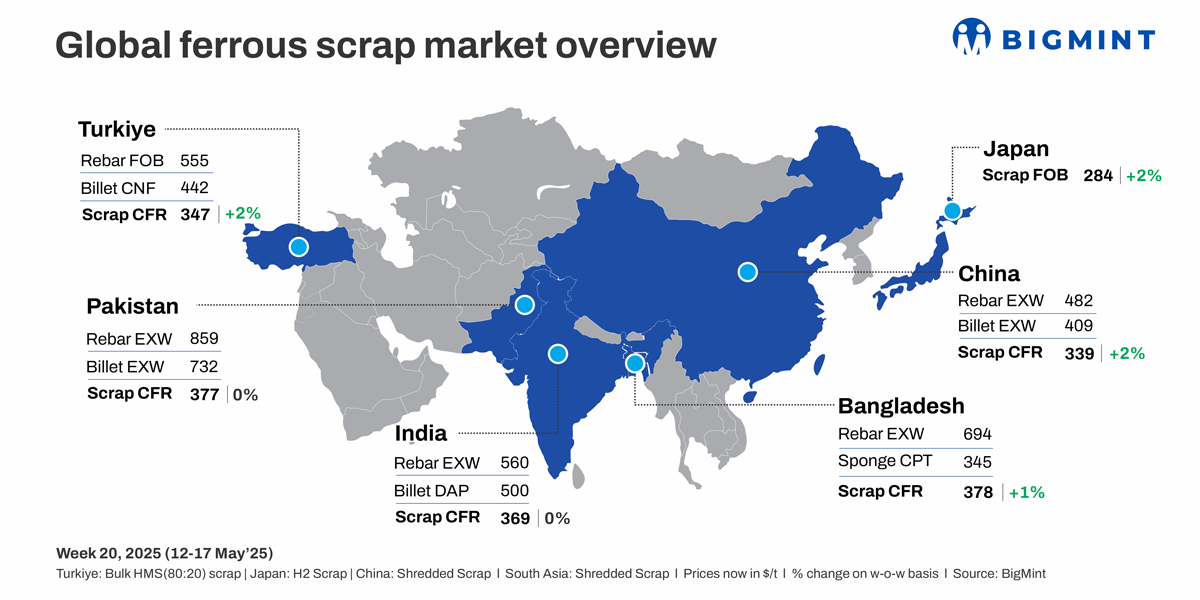

Global ferrous scrap prices showed an uptrend this week, supported by stronger steel demand and early restocking ahead of key holidays. Market activity increased overall, though some regions remained cautious amid ongoing uncertainties and bid-offer gaps.

Turkiye: The imported scrap market showed steady upward momentum this week, with US-origin HMS 80:20 bulk prices rising to $347/t CFR, up from $340/t last week. The increase was supported by improved domestic rebar sales and restocking interest among mills, who became more active in securing June-July shipments.

Market sentiment was buoyed by easing global trade tensions and optimism around peace talks in Istanbul, which encouraged firmer seller positions. Offers from the US and EU ranged between $345-350/t CFR, while recent deals hovered at $340-347/t CFR. However, bid-offer gaps persisted midweek as some mills resisted prices beyond $345/t, citing ongoing payment term issues.

Buyer resistance appeared but outlook stayed positive with strong steel demand and expected rebar sales supporting steady mill activity and firm prices.

India: The imported scrap market remained sluggish overall with shredded prices stable at $369/t CFR, slightly down from $370/t last week, limited trades as wide bid-offer gaps persisted throughout the week. While inquiries were steady, buyer expectations stayed lower than offered levels, preventing deal closures.

Pakistan: The imported scrap market remained subdued amid weak construction demand, slow steel sales, and tight rebar margins. Buyers mostly capped bids at around $375/t CFR Port Qasim, despite offers ranging up to $385/t due to higher freight costs. Mills maintained sufficient inventories while awaiting clearer market trends ahead of the Eid slowdown. Shredded prices remained largely stable w-o-w, inching up to $377/t from $376/t.

In the domestic market, scrap prices were at PKR 138,000-139,000/t ($488-492/t) ex-yard. Mills remained cautious with limited fresh bookings amid weak finished steel demand.

Bangladesh: Imported scrap market stayed sluggish amid monsoon rains and weak construction demand. Trade was limited due to a $5-7/t bid-offer gap. There were some interests in bulk cargoes like a 10,000-t Japanese shipment of shindachi at $375-380/t, and HMS at $350/t CFR. Shredded prices rose slightly by 1% to $378/t from $376/t.

In the domestic market, steel demand remained soft. Domestic HMS was assessed at BDT 46,000-47,000/t ($540-552/t) ex-yard, and rebar hovered at BDT 80,000-82,000/t ($940-963/t) ex-plant. Mills continued to refrain from bulk bookings, prioritising inventory management as finished steel sales remained weak.

Japan: H2 export prices increased to JPY 41,300/t ($284/t) FOB Tokyo Bay, up JPY 900/t w-o-w, supported by firmer billet prices and a weaker yen. The May Kanto tender lifted sentiment, though trade remained limited due to a wide bid-offer gap and tariff concerns.

In the domestic market, average H2 prices stood at JPY 38,200/t ($263/t), down slightly w-o-w. Kansai saw a dip to JPY 38,000/t, while Kanto and Chubu held steady at JPY 43,000/t and JPY 36,300/t, respectively.

China: Shagang Steel raised scrap purchase prices by RMB 50/t ($7/t) on 13 May, bringing HMS (6-10 mm) to RMB 2,440/t ($337/t) with VAT, marking a total increase of RMB 100/t ($14/t) since April.

Vietnam: The imported scrap market stayed quiet amid a wide bid-offer gap and cautious sentiment. Japanese H2 was offered at $325–327/t CFR, but bids near $320/t saw no deals. US and Australian HMS 80:20 offers held at $350/t and $345/t CFR, while bids stayed at $330/t. Tariff concerns, currency risks, and a local BF issue added pressure.

UAE: UAE domestic HMS prices rose by AED 14/t ($4/t) to AED 1,227/t ($334/t), driven by tight supply as extreme heat slowed scrap collection. Sellers stayed firm amid rising global offers, especially from the US to Turkiye. Processed HMS traded at AED 1,220-1,230/t ($332-335/t), shredded at AED 1,260-1,270/t ($343-346/t), though demand was weak.

US: The US ferrous scrap export index rose $7/t this week, driven by increased buying from Turkiye amid stronger steel markets and Eid restocking. Vietnam and Bangladesh showed limited interest.

Leave a Reply