- Imports climb to 11-month high of over 16 mnt

- Indonesian coal imports drop 20% m-o-m

- Imports from South Africa surge but DRI output falls

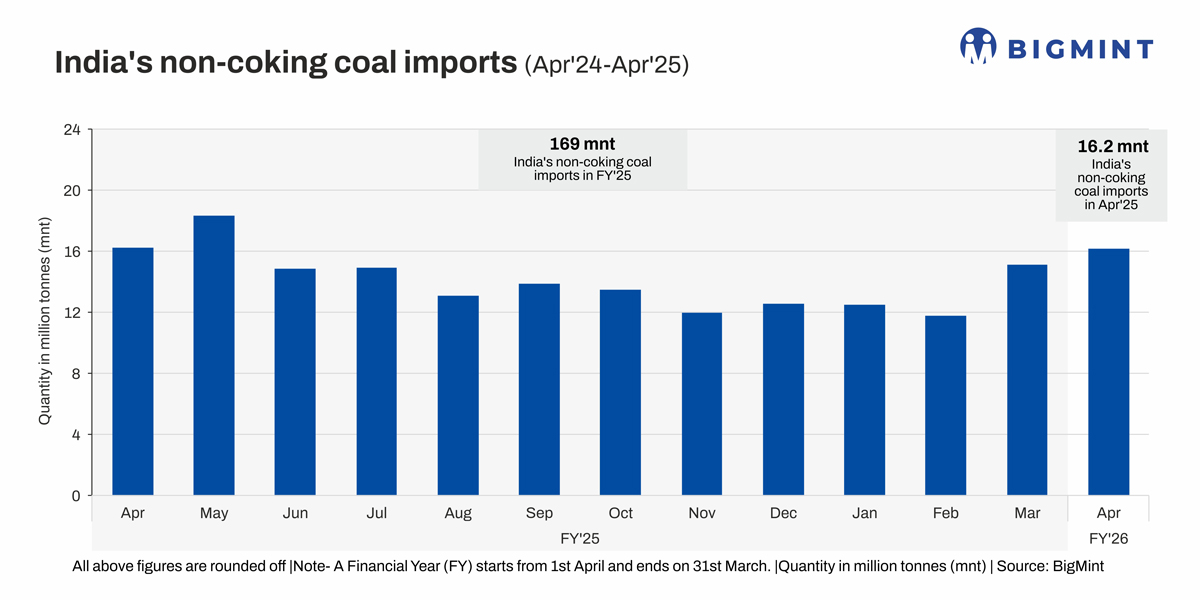

Morning Brief: India’s imports of non-coking coal continued to climb higher in April 2025, largely due to seasonal factors, with total imports reaching around 16.16 mnt – the highest in 11 months, as per BigMint data.

Imports rose by 7% m-o-m to 16.16 million tonnes (mnt) compared with 15.16 mnt in March. However, y-o-y, non-coking coal imports fell marginally by 0.5%.

India’s imports of non-coking coal, used for power production and in other industrial sectors, dwindled by 8% y-o-y in financial year 2024-2025 (FY’25) to around 169 mnt compared with 183 mnt in the preceding fiscal.

Indonesia was the leading exporter to India at over 8 mnt in April. However, volumes dropped 20% m-o-m. South Africa, on the other hand, raised total coal exports by 30% m-o-m to 3.4 mnt. Imports from Russia and Australia too surged, although volumes were not that significant, comprising around 10% of total Indian imports.

Among the major coal-handling ports in the country, Mundra witnessed a sharp decline in traffic – around 45% m-o-m largely reflecting weaker activity by Adani Enterprises, India’s top importer of coal from Indonesia and other countries. In contrast, the eastern ports of Krishnapatnam and Visakhapatnam saw higher traffic. These ports feed the coastal imported coal-based power plants (ICBs) in the eastern part of the country.

Factors supporting imports in April

Moderate uptick in peak summer demand: Coal imports are on the rise during the summer peak demand season, although volumes in April were marginally lower y-o-y. Domestic coal-fired generation saw a 4% m-o-m drop in April. Coal-based generation fell by 3% y-o-y in April. This was primarily because of intermittent spells of thunderstorms and rainfall that prevented the onset of a prolonged heatwave. The marginal decrease in power consumption in April resulted in only moderate growth in import demand.

Domestic production falls from March high: Domestic coal production in April fell to around 81 mnt from a peak of over 118 mnt in March. This was due largely to the efforts of domestic miners to meet dispatch targets ahead of the fiscal year end.

However, CIL pithead stocks were over 107 mnt, although the company’s production declined to around 62 mnt in April from over 85 mnt in March. As per government data, the captive and commercial mines logged production growth of 26.6% y-o-y last month. Coal stocks at power plants remained stable at over 57 mnt as on 11 May.

Therefore, sufficient domestic supplies restricted the growth pace of non-coking coal imports in April.

Sponge iron production falls but imports surge: South African coal imports, used in the Indian sponge iron sector, surged 30% m-o-m in April, although domestic sponge iron production fell by 8% m-o-m. Subdued sentiments in the steel sector weighed on the sponge iron market after an uptick in March, which resulted in the accumulation of inventories at different ports and subsequent price corrections.

Outlook

May usually witnesses a high level of coal imports, with April to June being the peak season before the onset of monsoons. A marginal increase in imports is, therefore, expected in May. However, Indonesian imports may continue to face headwinds amid coal pricing policy regulations introduced by the Indonesian government.

Domestic coal supplies have witnessed a sharp growth. The government has revised the SHAKTI policy to grant fresh linkages under two different ‘windows’ for power sector consumers, which is expected to enhance availability. The government’s mandate for coal imports for blending in power plants has not been renewed since February.

That said, power demand is expected to peak in May and June. So, moderate growth in imports may be expected despite increased domestic supplies.

Leave a Reply