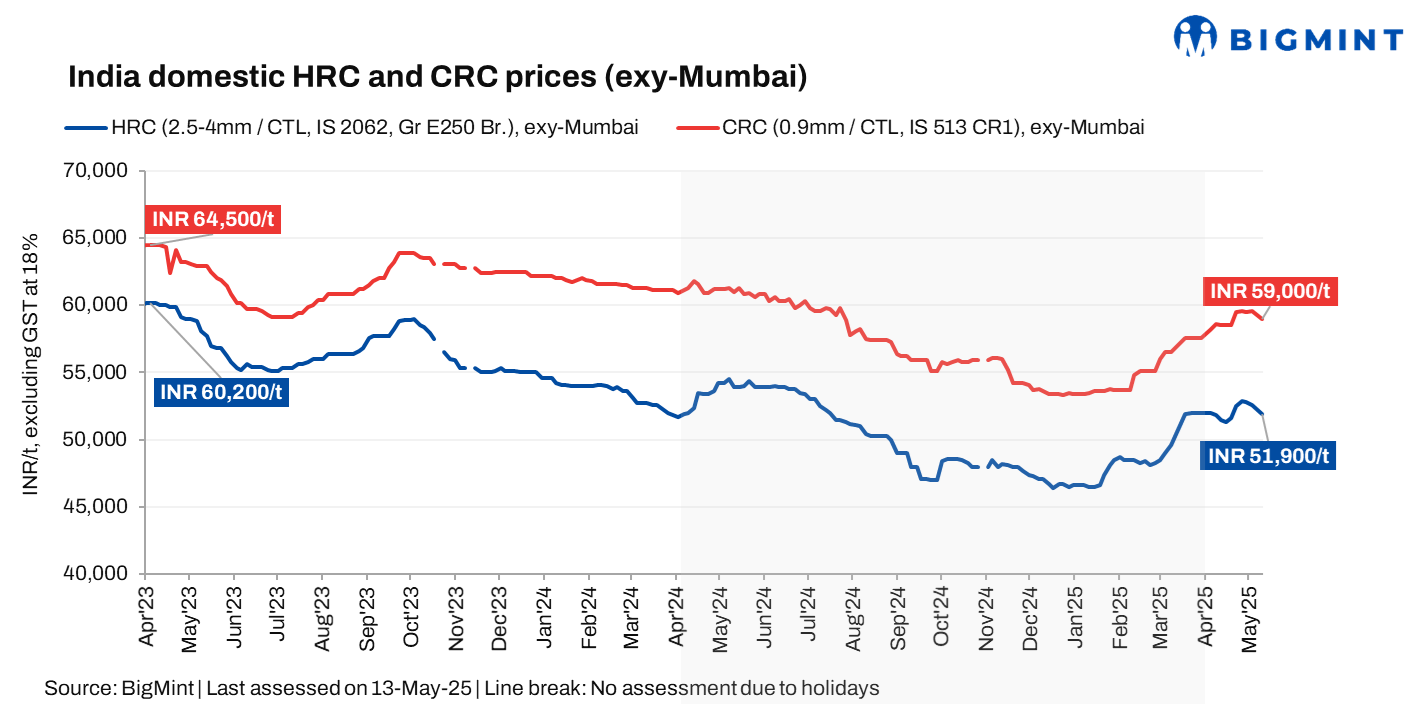

Market faces limited demand, liquidity crunch: Demand was weak, with buyers making purchases only to meet immediate requirements. Liquidity was also constrained, and most new sales were on credit. Payment recovery remained slow.

“The market is expected to remain range-bound as buyers resist price increases. However, the downside risk to prices appears limited due to shrinking availability of older, lower-priced inventory and a decline in imports. While caution is advised, limited supply is likely to support prices and prevent significant declines,” a market participant noted.

Import trends: India’s bulk imports of HRCs and plates touched 70,025 t as of 12 May, based on vessel line-up data from BigMint. The same totalled 306,260 t in April 2025 and 408,762 t in March 2025.

Export trends: Indian HRC (S275) export offers to the European Union (EU) declined by $5/t w-o-w to $640-645/t CFR Antwerp ($590-595/t FOB eastern Indian port), compared to $650-655/t CFR last week. Despite the price drop, trading activity in the region remained subdued. Buyers were cautious due to competitive pricing from European mills within their domestic markets, according to sources.

Meanwhile, Chinese HRC offers to the Middle East (ME) remained stable in a recent transaction. Currently, Indian mills are less active in the ME due to strong competition from Chinese suppliers and better price realisations in the domestic market.

Outlook

In the near term, continued price pressure on HRC and CRC is expected due to weakening demand and tight liquidity. Buyer resistance to price hikes will likely lead to a range-bound market, with diminishing cheaper inventory and lower imports possibly limiting significant downward movement. Caution prevails amid subdued trade activity and competitive offers.

Leave a Reply