- Primary mills’ list price hikes fail to lift HRC tags

- Expectations of price drops slow BF rebar trade

- Bid-offer gaps push IF rebar sellers to cut offers

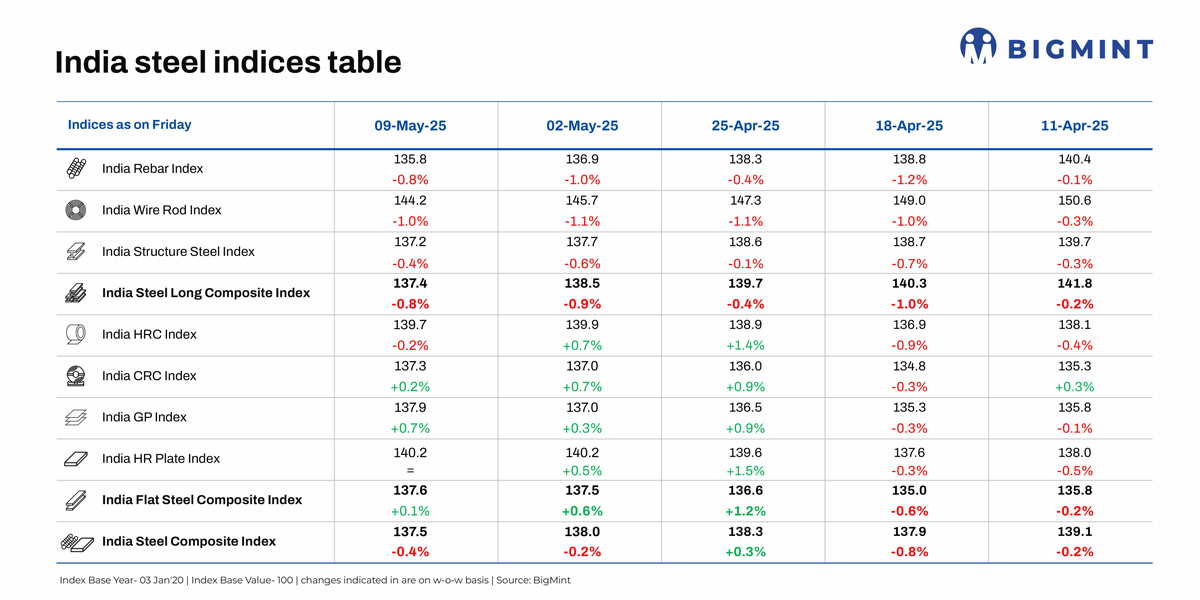

Morning Brief: BigMints India Steel Composite Index continued its downward spiral last week, dropping by 0.4% w-o-w to 137.5 points on 9 May 2025 after a 0.2% drop on 2 May. The primary mills’ price announcements for the month – hiking hot-rolled coil (HRC) and rolling over rebar prices – failed to halt the bearish momentum in the trade market.

While the long steel index dropped 0.8% w-o-w, flats registered a minute 0.1% rise. Notably, a 0.8% fall w-o-w pulled down the rebar index to its lowest since mid-March. Prices in the longs segments experienced pressure, indicated by across-the-board decline. Among flats, only HRC prices dropped, but this was enough to keep the index largely flat w-o-w.

Factors impacting index last week

BF rebar prices remain range-bound: Trade-level blast furnace (BF) rebar prices edged down last week, though some locations such as Delhi and Ahmedabad witnessed a slight rise. Mumbai logged an INR 100/tonne (t) ($1/t) drop w-o-w to INR 56,700/t ($664/t) exy, ex-GST, on 9 May.

Trade-level prices fell amid subdued demand. In fact, it seems that buyers are postponing purchases because they expect price drops soon. However, tags were supported by supply shortages in certain markets.

Earlier this week, Indian tier-1 mills rolled over rebar list prices for early-May deliveries compared to end-April levels. Post-revision, list prices hovered at around INR 56,000-57,000/t ($656-667/t) on landed basis.

The decision could be attributed to (1) sluggish demand, as demonstrated by a 10% increase m-o-m in rebar inventories with Tier-1 mills, in early-May; and (2) continued weakness in IF prices.

IF rebar prices fall amid need-based buying: IF rebar prices declined w-o-w, with Mumbai registering a significant INR 1,000/t ($12/t) drop to INR 48,000/t ($562/t) exw.

Trade was sluggish and need based, and wide bid-offer disparities led producers to reduce their offers to stimulate sales. However, retailers were hesitant to place large orders because of uncertain market dynamics. Consequently, sales pressure increased at mills, with average holding periods increasing to 10-11 days compared to 7-8 days previously.

Mills’ list price hikes fail to support HRC tags: Trade-level HRC prices declined slightly in most regions last week. In Mumbai, prices were at INR 52,400/t ($613/t) exy, ex-GST, on 9 May, down by INR 400/t ($5/t) w-o-w.

Prices fell amid buyer disinterest due to higher prices. Buyers were also unwilling to absorb mills’ price hikes of INR 500-1,000/t ($6-12/t) for HRCs and cold-rolled coils (CRCs), and sluggish trade momentum continued last week. Additionally, credit recovery was poor, especially in the north, with participants delaying payments and exercising caution because of the ongoing military confrontation between India and Pakistan.

However, the price drop was capped by tight supply because of limited imports and maintenance downtime. As per BigMint’s vessel line-up data, bulk imports of HRCs and plates totalled 306,260 t in April, while they were 408,762 t in March and 413,020 t in February.

Notably, revised list prices for HRCs were at INR 53,000-54,000/t ($620-632/t) ex-Mumbai. CRC prices ranged within INR 59,000-60,500/t ($691-708/t).

India’s HRC export offers show mixed trends: Indian HRC (S275) FOB offers to the EU rose by $10/t w-o-w to $650-655/t CFR Antwerp, but trade was slow due to cautious sentiment and market uncertainties. Conversely, Indian mills continued to withhold export offers to the Middle East, where competitive Chinese prices continued to dominate. Instead, Indian mills focused on the domestic market amid higher realisations.

Outlook

Prices are expected to remain range-bound in the near term. Lacklustre demand is expected to continue, buoyed by expectations of further price drops. However, supply shortages may motivate suppliers to keep price cuts limited to a narrow range. Moreover, the current geopolitical tensions may further keep markets cautious.

Leave a Reply