Domestic induction furnace finished long steel offers witnessed volatility this week. Prices drifted down in the range of INR 200-700/t. Trade reference prices for hot rolled coil (HRC) and cold rolled coil (CRC), however, saw an upward trend, increasing by INR 500-1,000/t w-o-w.

Iron ore and pellets

- BigMint’s bi-weekly domestic pellet (Fe63%) index remained stable w-o-w at INR 9,800/tonne (t) ($116/t) DAP Raipur on 9 May. Trade activity remained sluggish this week; however, a few deals were concluded by suppliers in Odisha at competitive offers.

- NMDC auctioned 72,800 t of iron ore from its Bacheli mines, Chhattisgarh, on 8 May. The entire 21,500-t DRCLO (10-40 mm, Fe 67%) offered was sold at a 3.4% premium over the base price (INR 7,270/t). Around 4,000-t Baila-sized lumps (10-20 mm, Fe 65.5%) were sold at a 7% premium over the base price (INR 6,640/t). However, 47,300-t Baila fines (Fe 64%) received no bids (base price was INR 5,550/t). Prices were on FOR, ex-stockpile/mines basis, including royalty, DMF, and NMET.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index inched down by $1/t w-o-w to $59/t FOB east coast, India, on 8 May. FOB prices dropped amid the hike in vessel freights. Exporters dealing with Fe57% grade fines are reportedly offering discounts of 21-22% compared to the global index. Around 250,000 t iron ore export deals for Fe50-57% were concluded with discounts of 20-22% on Fe57% and 26-28% on Fe54% grade fines.

Coal

- US pet coke prices fell to $100–102/t CFR in eastern and western India amid weak Chinese demand and trade-related uncertainties. Saudi-origin offers rose to $116–118/t CFR but may not sustain the gap for long due to shifting buying patterns.

- IOCL reduced pet coke prices by INR 1,000/t m-o-m in May across key refineries, in line with weak demand and global softness.

- RB2 (5500 NAR) prices declined by INR 50/t w-o-w to INR 8,300/t ex-Gangavaram; a deal was reported at INR 8,150/t at Ennore. Imports dropped 8% m-o-m to 3.24 mnt in April. Export offers eased $1–2/t to $73.5/t FOB as demand remained sluggish amid high portside stocks and weak spot trades.

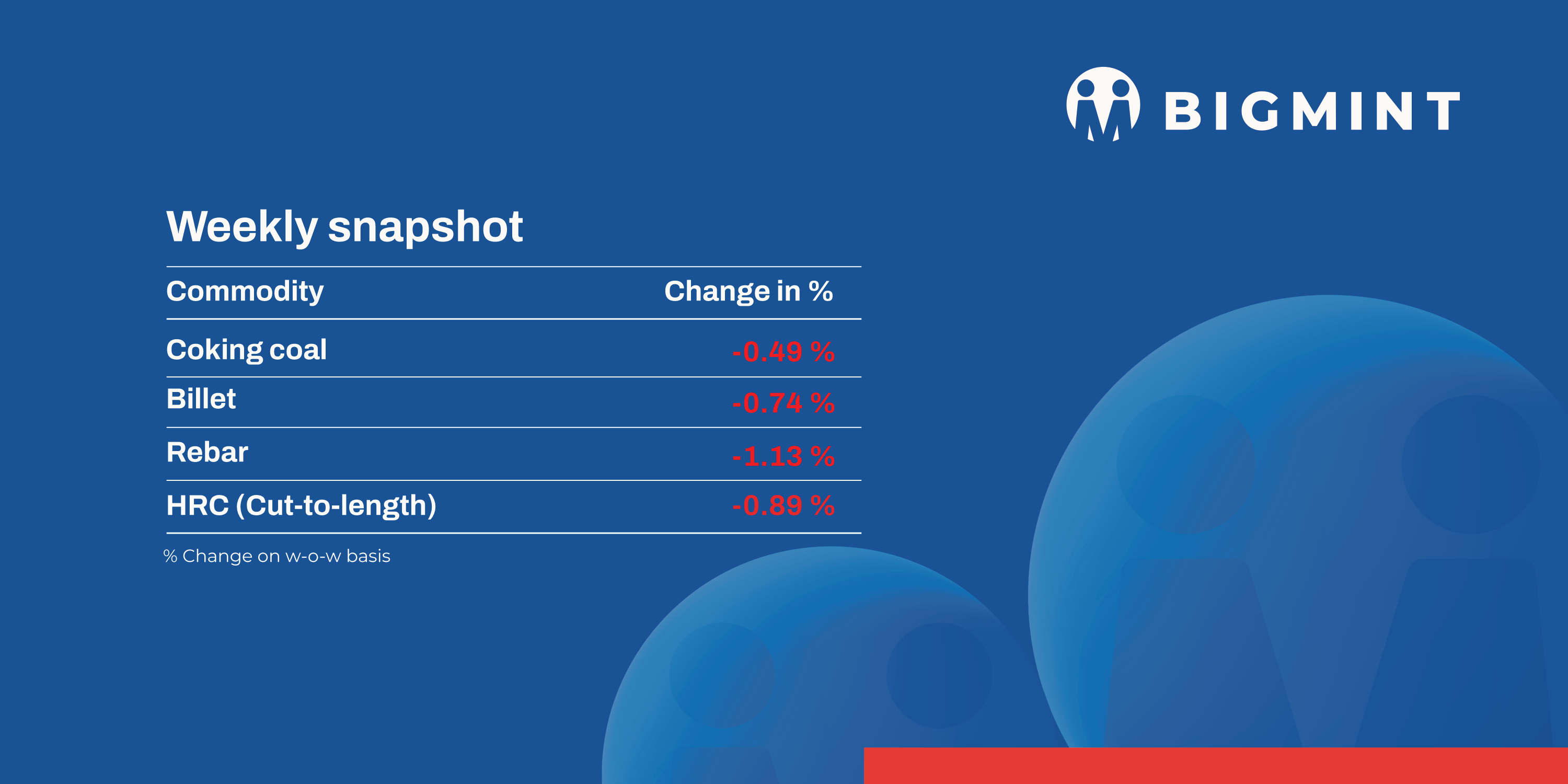

- Met coke prices in Jajpur fell by INR 650/t w-o-w to INR 33,000/t, while in Gandhidham prices dropped INR 1,200/t to INR 31,000/t. The decline was driven by reduced buying interest from end-users amid falling pig iron prices.

- East Kalimantan-Paradip freight dropped $0.6/t to $13.5/t, while Australia-Paradip rates fell by $0.2/t to $14.4/t due to vessel oversupply. South Africa-Paradip rates inched up by $0.3/t to $13.1/t amid tight tonnage. Indian portside coal inventories rose 7% w-o-w, indicating weak import demand.

Ferrous scrap

- India’s imported ferrous scrap market remained largely muted throughout the week as buyers adopted a cautious stance amid weak domestic steel demand, regional geopolitical tensions, and the approaching monsoon season. Despite firm offers from UK and EU suppliers, buyers refrained from active bookings, preferring ready material and holding back on forward deals.

- Shredded scrap offers from the UK and EU stayed stable at $370-375/t CFR, but most bids remained at $360-365/t, creating a wide bid-offer gap. Only limited deals were reported around $365-367/t. For HMS 80:20, EU-origin offers hovered at $350-355/t CFR, but buyer resistance capped transactions at or below $350/t.

- Around 8,000-8,500 t of imported scrap were booked in India this week. This included 1,000 t of HMS 80:20 at $350-365/t CFR and 1,000 t of shredded scrap priced around $365/t CFR. The rest comprised turnings, cast iron, CRC bundles, and around 3,000 t of bluesteel scrap, which traded at $381-384/t CFR.

Ferro alloys

- Silico manganese: Indian silico manganese prices decreased by INR 425/t ($5/t) w-o-w to INR 69,800-70,300/t ($817-823/t) in the key regions of Durgapur, Raipur and Vizag. The downward trend was driven by weak demand, limited export activity, and adequate supply in the market. Buyers showed limited interest amid an uncertain steel sector outlook.

- Ferro manganese: Indian ferro manganese (HC 70%) prices fell by INR 1,000/t ($12/t) w-o-w to INR 72,000/t ($843/t) exw in Durgapur. Meanwhile, prices, exw-Raipur decreased by INR 900/t ($11/t) to INR 72,300/t ($846/t). The market showed hesitancy in accepting higher quotes due to which the prices fell, while slow demand for steel also impacted prices.

- Ferro silicon: Indian ferro silicon prices were largely steady with a slight decline of INR 200/t ($2/t) w-o-w to INR 95,100/t ($1,113/t) exw-Guwahati. Meanwhile, prices in Bhutan dipped by INR 200/t ($2/t) to INR 95,300/t ($1,116/t) exw. Prices stayed stable as the majority of sellers both in north east India and Bhutan adapted to the newly announced offers of INR 95,500/t ($1,118/t) exw.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices held steady w-o-w at INR 100,400/t ($1,176/t) exw-Jajpur. Price fluctuations were minimal, as demand was limited in the domestic market. Additionally, bid-offer disparities continued, as buyers showed limited acceptance of higher offers from suppliers.

Semi-finished steel

- Indian semi-finished steel prices showed diminishing trend as per BigMint’s assessment. Domestic billet prices in almost all key locations decreased by INR 200-700/t across regions with major decrease of INR 700/t seen in Durgapur. Similarly, sponge iron prices also showed downtrend, almost all key locations moved down by INR 100-1,000/t, with a major decrease of INR 1,000/t seen in the Ramgarh.

- Indian DRI (Direct Reduced Iron) export offers decreased by $1 for CPT Raxaul, stood at $346/t while, CPT Benapole offers increased by $2 and stands at $352/t.

- In the latest auction held by SAIL-RSP for 5,000 t of steel grade pig iron, only 900 t or less than 20% got booked at INR 33,500/t (ex-works). The last auction, conducted on 24 Apr’25, had concluded at INR 34,500/t.

Finished long steel

- IF-rebar: India’s induction furnace route rebar prices declined w-o-w. Trading activity remained sluggish across most regions, with buyers only purchasing to fulfil immediate needs. The gap between bid and offer prices led manufacturers to lower their offers to stimulate sales. However, retailers, in particular, were hesitant to place large orders, opting to wait for more clarity on price trends amidst ongoing market uncertainty. As a result, sales pressure gradually increased at mills, and inventories have started to accumulate. Current stock levels at mills stand at around 10-11 days, compared to the previous 7-8 days. Overall, market participants expect prices to remain rangebound in the short term.

- On a weekly basis, in rebar prices witnessed a decline in the range of INR 100-1,300/t across regions.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 43,600-44,000/t exw Raipur and INR 48,200-48,800/t exw Jalna.

- Trade reference prices of heavy structural steel for base size 150mm channel are at INR 45,000-45,400/t exw Raipur.

- Trade reference prices of wire rods are hovering at INR 43,600-44,100/t ex Raipur.

- BF-rebar: Indian Tier-1 mills have rolled over rebar list prices for early-May deliveries compared to end-April levels. Post-revision, list prices hovered at around INR 56,000-57,000/t on landed basis. Trade-level BF-rebar prices remained range-bound w-o-w, fluctuating in a narrow range amid muted buying interest.

- Prices for 12-32mm material in the trade segment this week edged lower by INR 100/t w-o-w to INR 56,700/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the projects segment, prices hovered in the range of INR 55,500-56,500/t FOR Mumbai.

Flat steel

-

- Leading Indian steel producers have raised list prices for hot-rolled coils (HRCs) and cold-rolled coils (CRCs) by INR 500–1,000/t ($6–12/t) for May sales, citing tighter supply and reduced import pressure. Current HRC prices are at INR 53,000–54,000/t ($627–638/t) and CRC at INR 59,000–60,500/t ($697–715/t), ex-Mumbai. While most major mills have implemented the hike, some players are yet to make formal announcements.

- As of 6 May, BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) decreased by INR 200/t ($2/t) w-o-w to settle at INR 52,600/t ($620/t). However, CRC (IS513, Gr O, 0.9 mm/CTL) prices rose by up to INR 100/t ($1/t) w-o-w to INR 59,600/t ($703t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

- Maintenance shutdowns at Tata Steel’s Jamshedpur plant and JSW’s Dolvi unit are expected to further constrain supply. However, demand remains subdued, with buyers focusing on need-based purchases amid tight liquidity.

- Imports continued to fall, reaching 306,260 t in April, down from over 408,000 t in March. Export activity remains limited as Indian producers prioritise domestic sales, while Chinese and Japanese mills dominate international markets.

Leave a Reply