- India sees muted demand amid geopolitical tensions

- Japan’s market stays quiet ahead of Kanto tender

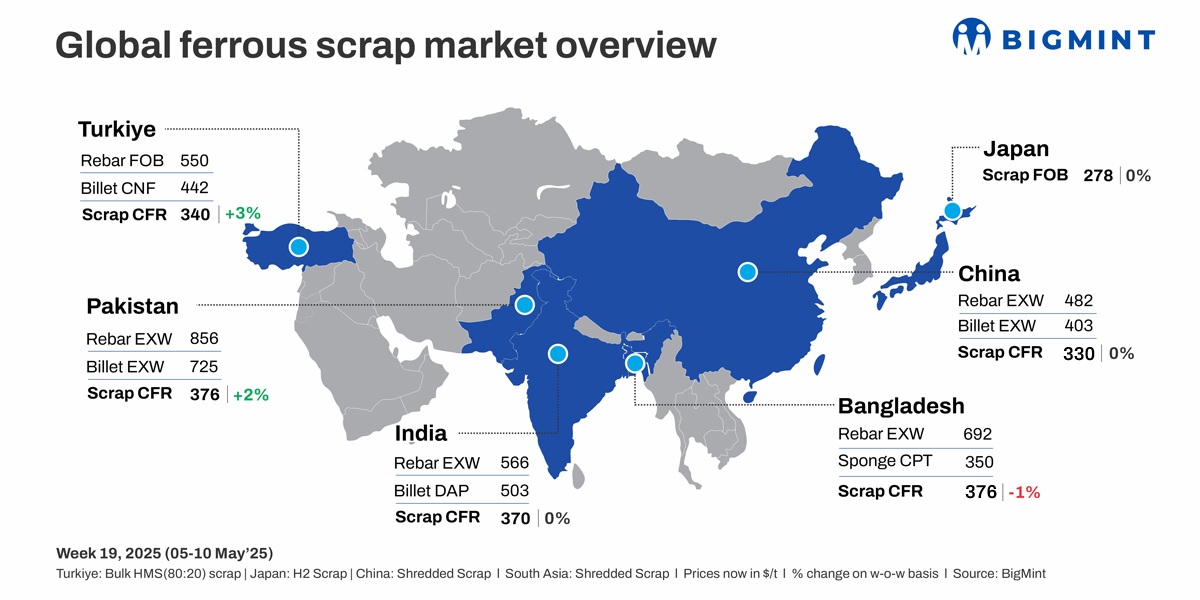

Global ferrous scrap prices showed mixed trends this week. India, Bangladesh, and Vietnam saw subdued markets due to weak demand. Pakistan showed some positive sentiment despite low activity, while Turkiye experienced improved sentiment, with stronger demand from mills and tighter supply.

Turkiye: Imported ferrous scrap market saw a gradual improvement with US-origin HMS 80:20 CFR Turkiye rising to $340/t, up 3% from last week’s $330/t, driven by rising collection costs in the US and Europe and expectations of post-holiday restocking. While mills remained cautious due to sluggish rebar demand and adequate scrap inventories, sellers gained confidence that prices had bottomed out and held firm on offers.

A key US-origin HMS 80:20 deal at $338/t CFR supported a price rebound, with further bookings at $337-342/t CFR. Sellers from the US and EU pushed higher offers, but Turkish buyers remained selective due to pressure on finished steel sales.

Despite firming market fundamentals, trading volumes stayed limited as mills waited for clearer signals from the steel market before booking significant volumes.

India: The imported ferrous scrap market remained largely muted throughout the week as buyers adopted a cautious stance amid weak domestic steel demand, regional geopolitical tensions, and the approaching monsoon season. Despite firm offers from UK and EU suppliers, buyers refrained from active bookings, preferring ready material and holding back on forward deals.

Shredded scrap offers from the UK and EU stayed stable at $370-375/t CFR, but most bids remained at $360-365/t, creating a wide bid-offer gap. Only limited deals were reported around $365-367/t. For HMS 80:20, EU-origin offers hovered at $350-355/t CFR, but buyer resistance capped transactions at or below $350/t.

Around 8,000-8,500 t of imported scrap were booked in India this week. This included 1,000 t of HMS 80:20 at $350-365/t CFR and 1,000 t of shredded scrap priced around $365/t CFR. The rest comprised turnings, cast iron, CRC bundles, and around 3,000 t of bluesteel scrap, which traded at $381-384/t CFR.

Pakistan: The imported scrap market in Pakistan remained sluggish this week, despite a rise in UK/EU-origin shredded scrap offers, which increased by 2% w-o-w to $376/t CFR Port Qasim, from $368/t. Mills continued to operate below capacity due to weak finished steel demand, falling billet and rebar prices, and geopolitical tensions. This led to limited deal-making as a persistent bid-offer gap and bearish sentiment dampened market activity.

Domestic scrap prices were at PKR 135,000-140,000/t ($480-500/t), billets at PKR 195,000-200,000/t ($693-711/t), and rebars at PKR 230,000-240,000/t ($823-859/t), with slow construction activity and stalled government projects negatively impacting market sentiment.

Bangladesh: The imported scrap market remained sluggish this week as mills refrained from fresh bookings amid weak steel demand, tight liquidity, and rising freight costs. Bulk and containerised trade slowed after a wave of recent bookings, with offers for Australian shredded and PNS scrap hovering around $375-385/t CFR Chattogram. Shredded prices fell 1% w-o-w to $376/t from $379/t, reflecting weak sentiment.

Domestic rebar demand remained soft, with mills offering rebar at BDT 82,000/t in Dhaka and BDT 85,000/t in Chattogram, along with discounts of BDT 500-1,000/t. Rising freight rates and subdued construction activity kept mill buying interest low.

Japan: H2 scrap market remained subdued this week ahead of the May Kanto tender, with a 15,000 t lot awarded at JPY 42,389/t ($291/t) FAS, reflecting a slight drop m-o-m. Market sentiment was muted as participants awaited for cues from the tender.

Export offers held steady at JPY 40,400/t ($278/t) FOB Tokyo Bay, while domestic prices dipped to JPY 40,300/t ($277/t) amid low activity. Japanese H2 scrap may see increased demand as logistical issues in markets like Bangladesh shift interest toward Japan.

Vietnam: The imported scrap market remained quiet due to weak demand and a wide bid-offer gap. Some buyers considered South American HMS 80:20 for better pricing, but delays may shift interest back to Japanese H2, which traded at $320/t CFR.

South Korea: The scrap market gained momentum as Hyundai Steel and SeAH Changwon raised purchase prices by KRW 10,000/t for 7–17 May. POSCO will pause scrap intake from 12–15 May, leading to possible short-term stockpiling. Nationwide scrap inventories fell 9% m-o-m to 845,000 t, with sharper drops in THE central and southern regions, intensifying competition for available material.

US: Ferrous scrap export prices rose $9/t w-o-w, with HMS 80:20 at $319/t and shredded at $339/t FOB, driven by strong Turkish demand and tight supply. Mills remain selective, eyeing finished steel margins before making commitments.

Leave a Reply