- RB2 weakens further amid muted market sentiment

- RB3 coal prices remain unchanged

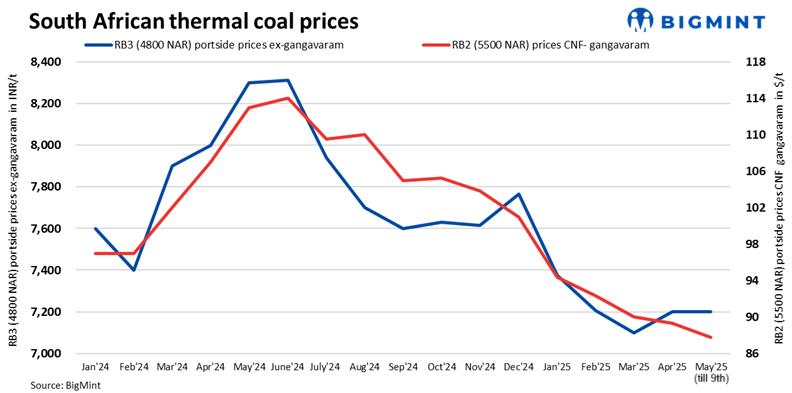

South African coal prices at Indian ports continued to soften this week as demand stayed subdued due to market volatility and high inventory levels. As per BigMint’s latest assessment, RB2 (5500 NAR) slipped INR 50/tonne (t) w-o-w to INR 8,300/t exw-Gangavaram. RB3 (4800 NAR) remained unchanged at INR 7,200/t.

Trade update

A deal for RB2 was concluded at INR 8,150/t at Ennore port.

Import volumes decline slightly

India’s non-coking coal imports from South Africa fell by 8% m-o-m to 3.24 million tonnes (mnt) in April 2025, down from 3.54 mnt in March. Despite the dip, monthly volumes remained strong compared to earlier trends.

Sponge iron prices under pressure

C-DRI prices dropped by INR 300/t w-o-w to INR 25,600/t from INR 25,900/t, while P-DRI ranged from INR 23,600-27,700/t across major markets. The decline of INR 50-200/t d-o-d was driven by limited participation and weak sentiment. Buyers remained cautious, purchasing only to meet immediate requirements.

Export market

South African RB2 export offers declined further by $1-2/t to $73.5/t FOB, while RB3 dropped to $61/t FOB as of 9 May.

Domestic market

Domestic coal prices remained stable, with 4500 GCV and 5000 GCV grades assessed at INR 4,500/t and INR 4,950/t exw-Bilaspur, respectively. SECL auctions continued to reflect low participation amid sufficient stocks and tepid demand.

Outlook

With weak demand, high portside inventories, and falling sponge iron prices, the South African coal market is expected to remain soft in the near term. Spot trades are likely to stay limited unless delivered costs decline significantly or demand picks up.

Leave a Reply