- Chattogram mills secure 15,000-t H2 scrap

- Japanese H2 offers steady, liquidity thin

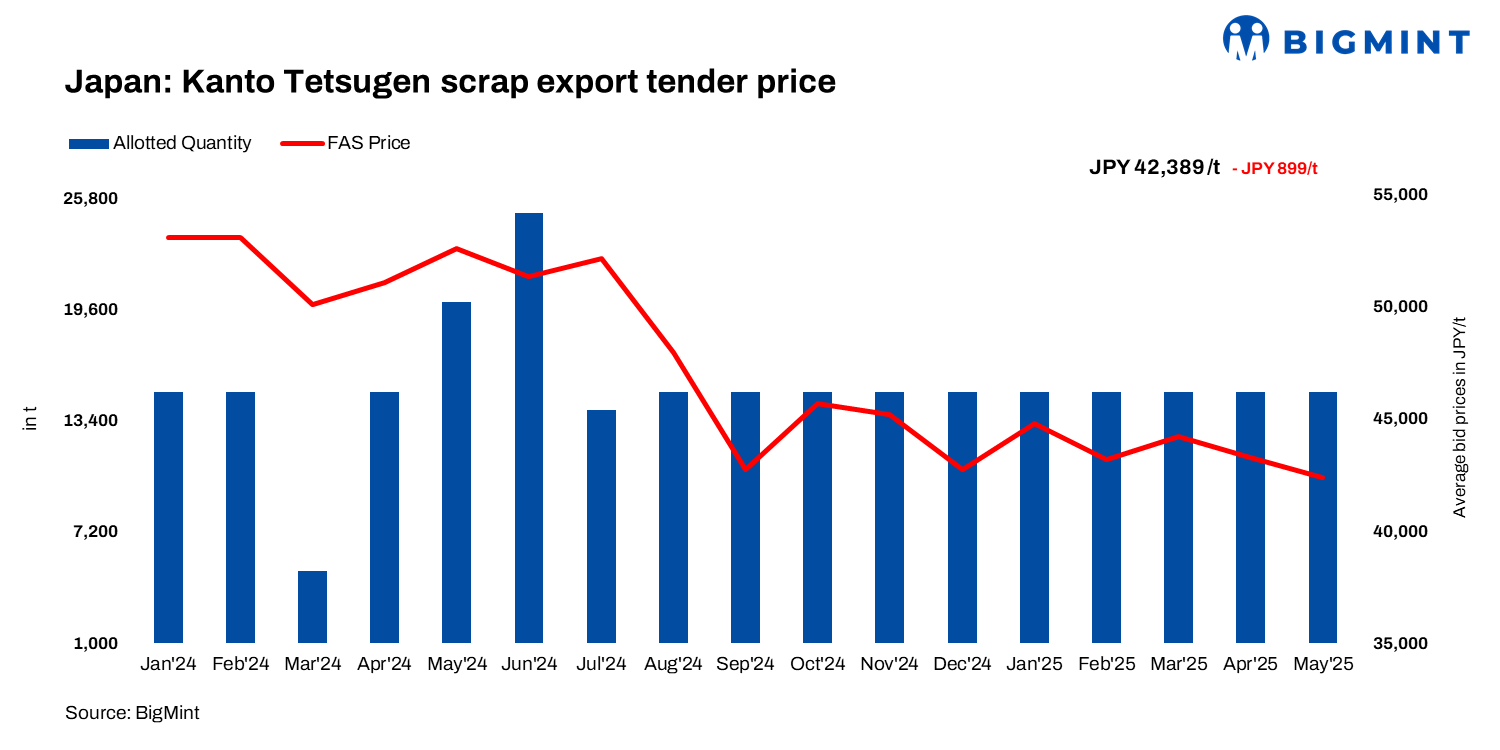

Japan’s May 2025 Kanto scrap export tender saw a m-o-m dip in bids, with a 15,000 tonne (t) H2 scrap lot awarded at JPY 42,389/t ($291/t) FAS, down JPY 899/t and $6/t from April.

According to market sources, a Chattogram-based mill reportedly secured the winning lot via a Japanese trading firm, translating to an estimated FOB price of $300/t, while the CFR price is suggested to be around $350-355/t.

The minor depreciation of the yen to 145.7 from 145.3 had negligible impact on dollar pricing.

This time, all 15 companies submitted 16 bids totalling 141,100 t–the highest since Oct ’21. A 15,000-t lot was awarded with shipment due by 30 June.

Additionally, the Japanese H2 export market remained mostly inactive and rangebound during the week, as participants returned from the Golden Week and were waiting for the Kanto tender.

BigMint assessed H2 scrap export offers almost steady at JPY 40,400/t ($278/t) FOB Tokyo Bay, with domestic FAS prices slipping down to JPY 40,300/t ($277/t) w-o-w.

Still, restocking of Japanese H2 may rise soon due to logistical challenges with cargoes from other origins.

Market updates

Vietnam: Sentiment in Vietnam’s imported scrap market stayed muted as buyers remained inactive due to a wide bid-offer gap and soft demand. A persistent bid-offer gap prompted some Vietnamese buyers to explore more competitively priced South American HMS 80:20, though logistical delays may prompt restocking of Japanese H2.

Offers to Vietnam were at $325-330/t CFR, with bids around $315/t. Japanese H2 traded at $320/t CFR Vietnam.

Meanwhile, Vietnam imposed a 27.83% anti-dumping duty on certain Chinese HRCs, following a 21% y-o-y decline in March steel imports-aiming to shield its domestic steel sector.

Bangladesh: The imported scrap market in Bangladesh remained sluggish as mills stayed cautious about fresh bookings amid weak finished steel demand and rising freight rates.

Although the Kanto tender was awarded to a Chattogram-based buyer, overall market momentum remains weak. According to BigMint’s latest assessment Japanese H2 hovered around $357-358/t CFR, with bids trending lower.

Smaller buyers continued facing difficulties in opening LCs, restricting bulk scrap purchases and keeping overall activity dull. With subdued construction demand and squeezed margins, prices are likely to remain range-bound or edge lower in the near term.

South Korea: South Korea’s scrap market saw an uptrend as major mills, including Hyundai Steel and SeAH Changwon, raised purchase prices by KRW 10,000/t ($7/t) for 7-17 May.

POSCO will pause scrap intake at its Gwangyang and Pohang mills from 12-15 May, citing domestic operational shifts, with limited Saturday deliveries and risks of short-term stockpiling.

Scrap inventories fell 9% m-o-m to 845,000 t due to slower shipments during the holidays. With central and southern region stocks declining by 11% and 6%, respectively, competition for scrap is intensifying.

Outlook:

Japan’s scrap export market is expected to stay muted amid weak overseas bids, a wide bid-offer gap, and slow post-holiday activity. Despite lower Kanto tender prices, demand from Vietnam and Bangladesh remains sluggish. Some restocking interest in H2 may emerge ahead of the next tender on 11 June–a key event for East Asian buyers.

Leave a Reply