- Potential imported scrap arrivals weigh on sentiment

- Ongoing geopolitical tensions make buyers cautious

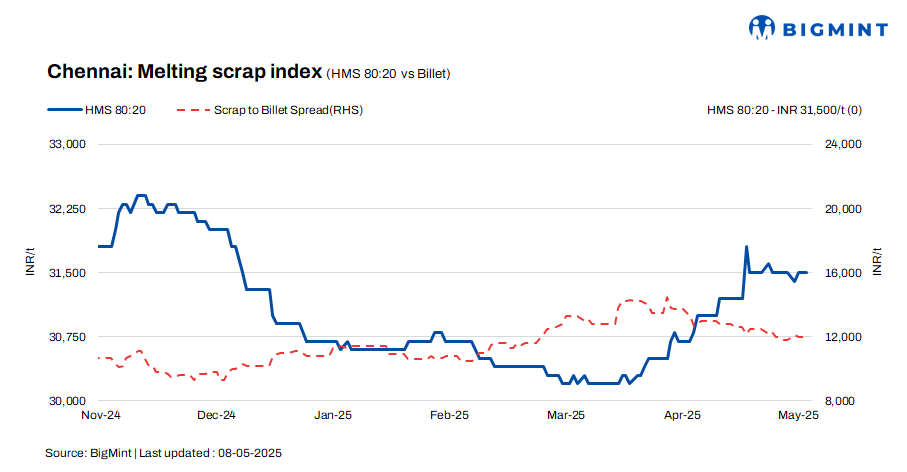

According to BigMint’s latest assessment, HMS (80:20) prices in Chennai remained steady d-o-d and w-o-w at INR 31,500/t amid sluggish finished steel trade. Similarly, billet prices held steady at INR 43,500/t on both d-o-d and w-o-w evaluations. Rebar prices, however, declined by INR 200/t w-o-w, to INR 48,300/t, though they remained unchanged d-o-d. The overall market sentiment indicates a mixed trend, with price stability dominating daily trades and only marginal fluctuations seen over the week.

Imported, domestic price trends

A scrap trader observed that offers for shredded from Australia were in the range of $365-370/t CFR Chennai, while HMS 80:20 was quoted at $345-350/t. Notably, buying activity was subdued, as ongoing geopolitical tensions pushed major buyers into a wait-and-watch mode. Additionally, with previously booked vessels scheduled to arrive at Chennai Port, buyers held off on fresh bookings, expecting potential changes in pricing dynamics once these shipments are cleared.

Domestic HMS (80:20) traded in the range of INR 31,000-31,500/t for immediate payment transactions, while deals involving extended credit terms were priced slightly higher, at INR 31,500-32,000/t. Most offers and concluded deals remained within the INR 31,000-32,000/t range, pointing to a stable pricing environment.

Buyer-supplier sentiments

According to a mill representative, billet offers remained stable over the past few days, as sellers held back material rather than accepting lower bids. A key reason for this firmness is that many major billet suppliers operate their own re-rolling mills, allowing them to opt for internal consumption instead of selling at discounted prices. On the raw material side, sponge iron offers also remained nearly unchanged, with buyers showing a preference for locally sourced sponge due to quality concerns associated with material from neighbouring states.

According to a source, rebar demand weakened in recent days, impacting overall trade activity. The slowdown was further compounded by heavy rain and storms in Chennai last week, which disrupted power supply in the region and negatively affected steel production. Despite this, scrap arrivals at mills remained steady at current prices, with most producers able to procure material as per their requirement, indicating a balanced supply environment.

A scrap supplier stated that HMS 80:20 was trading at INR 31,000-32,000/t, with the variation largely driven by payment terms. With finished steel trade activity slowing in recent days, some market participants expect a possible downward movement in scrap prices. Additionally, expectations of incoming imported scrap vessels at Chennai Port this month added pressure on domestic pricing, as the potential rise in availability could weigh on sentiment.

Regional comparison

In the Jalna market of western India, billet prices dropped by INR 200/t d-o-d to INR 42,200/t, while rebar prices declined by INR 200/t d-o-d to INR 48,600/t. HMS 80:20 also moved down by INR 100/t d-o-d to INR 32,700/t. Market sentiment was cautious amid weak finished steel demand, and scrap suppliers showed a reluctance to sell, holding back inventory in response to the current low price realisations.

Outlook

Sources indicate that scrap prices are expected to remain range-bound, with likely fluctuations of INR +/- 500/t in the short term. This stability will likely be driven by continued uncertainty in the finished steel trade, where both buyers and sellers are taking a cautious approach. The resulting sentiment is expected to limit volatility and keep the market within a narrow pricing band.

Leave a Reply