- Buyers show reluctance towards higher offers

- Limited supplies, fall in output fail to lift tags

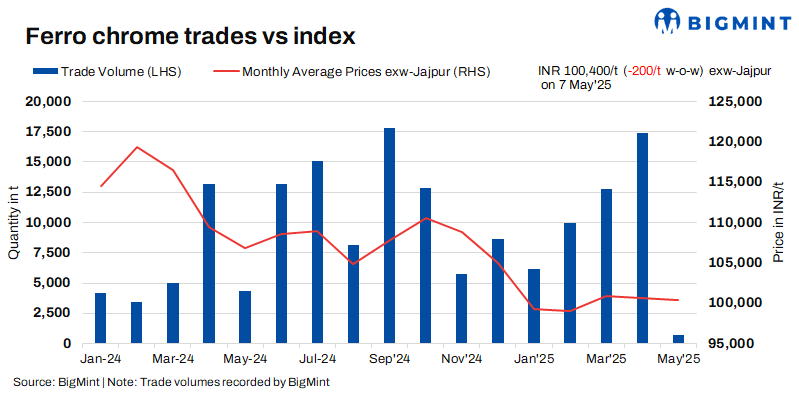

Indian high-carbon ferro chrome (HC60%, Si:4%) prices were largely stable w-o-w, inching down by INR 200/t ($2/t) in comparison to the previous assessment on 30 April. Price fluctuations were minimal, as demand was limited in the domestic market.

As per BigMint’s assessment on 7 April, high-carbon ferro chrome (HC60%, Si:4%) prices in India were at INR 100,400/t ($1,184/t) exw-Jajpur. Deals for nearly 800 t were concluded in the period under review in the price range of INR 100,000-102,000/t ($1,179-1,203/t) exw.

Moreover, low-silicon high-carbon ferro chrome prices dipped by INR 700/t ($8/t) w-o-w to INR 106,000/t ($1,250/t) exw-Durgapur. Trades for around 200 t were finalised within INR 105,000-106,000/t ($1,238-1,250/t) exw.

Additionally, low-carbon (C:0.1%) ferro chrome prices too declined by INR 1,900/t ($22/t) w-o-w to INR 203,600/t ($2,401/t) exw-Durgapur.

Market summary (1-7 May 2025)

Buyers show reluctance towards higher offers: Bid-offer disparities continued, as buyers showed limited acceptance towards higher offers from suppliers, ranging within INR 102,000-103,000/t ($1,203-1,215/t) exw. As per sources, only one major buyer floated an inquiry during this period. Hence, amid limited demand, suppliers reduced offers, and the market mostly operated at INR 100,000-101,000/t ($1,179-1,191/t) exw.

As per BigMint’s data, India’s ferro chrome production was 0.35 mnt in Q4FY’25. A significant drop of 31% y-o-y was seen against the 0.46 mnt produced in Q4FY’24. Commenting on this, a major domestic seller stated, “Despite limited supplies and a drop in production, prices have not increased, as there is a gap between supply and demand.”

Chinese prices remain steady w-o-w: Ferro chrome (HC60%) prices in China were unchanged w-o-w at RMB 8,100/t ($1,121/t) exw-Inner Mongolia. Although demand was weak, given higher chrome ore costs, prices did not experience any fluctuations. Higher chrome ore prices led to tighter spot inventory and increased production costs, reducing smaller manufacturers’ willingness to resume production.

Stainless steel demand, however, improved, driving up ferro chrome demand slightly, as stainless steel is its primary application. This recovery led to optimism among producers about future prices, with some expecting higher tags despite overall stable trading conditions.

India’s stainless steel flats prices edge up: Prices of 304-grade stainless steel hot-rolled coils (HRCs) edged up by INR 1,000/t ($12/t) w-o-w to INR 186,000/t ($2,171/t) exw-Mumbai. The increase was due to a recent hike in prices by a leading Indian manufacturer. Driven by improved demand, the producer raised prices of 300 series products by INR 2,000/t ($23/t) from 6 May 2025.

Finished stainless steel market sentiment was steady, but Indian manufacturers faced sales pressure due to subdued demand and the impact of reduced shipments to the US, alongside competition from potential Chinese steel exports. Long product prices remained unchanged w-o-w.

Outlook

Considering current market conditions, prices are likely to move within a narrow range in the days ahead.

Leave a Reply