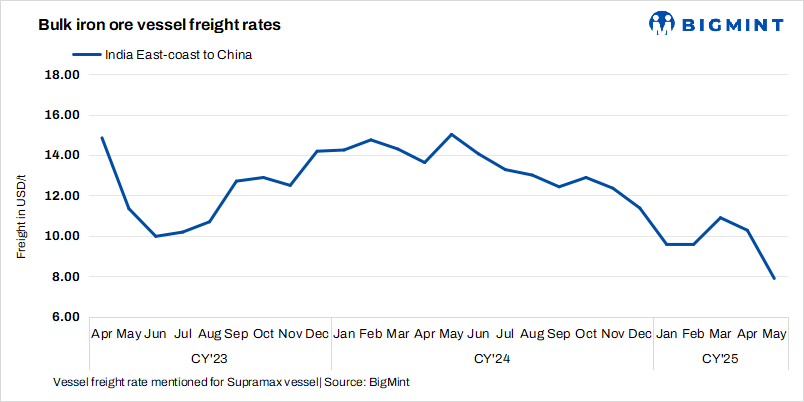

- Freights from India to China remain stable w-o-w

- China sees slow activity post Labour Day holidays

Dry bulk iron ore freights exhibited mixed trends w-o-w on key routes amid subdued market momentum. Freights from India to China remained stable amid a balanced supply-demand dynamic. While overall spot activity was subdued, a consistent trickle of cargoes from Indian ports helped prevent a steep fall in rates. Charterers and shipowners remained cautious, avoiding aggressive pricing moves, which supported rate stability.

Chinese steel production was largely sufficient to sustain a baseline level of import activity. Additionally, with relatively stable bunker fuel prices and no major weather disruptions, freight rates remained steady on the India-China route despite broader market softness.

On the other hand, Capesize freights fell mainly due to a sharp drop in freight derivative (FFA) prices during Asian trading hours. This weakened market confidence and reduced support for freights, despite hopes of a rebound after the holiday period. However, Chinese trading activity remained slow following the Labour Day holidays, limiting any potential rate recovery.

Factors influencing freights

- Baltic indices show mixed sentiment w-o-w: The Baltic Dry Index (BDI) was recorded at 1,421 on 5 May, increasing by 48 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 2,079, rising by 190 points w-o-w. However, the Baltic Supramax Index (BSI) inched down by 22 points w-o-w to 955.

- China’s iron ore spot prices remain stable w-o-w: China’s spot prices of iron ore fines (Fe62%) were assessed at $99/tonne (t) CFR on 6 May, stable w-o-w amid underlying market uncertainties and emerging bearish factors. Ongoing concerns over steel production cuts across key Chinese provinces weighed on sentiment, limiting aggressive buying. While trading resumed post-holiday, mills largely restricted purchases to immediate needs, reflecting caution amid weakening fundamentals.

Route-wise updates

- India-China: Freights from the Indian Ocean to China were recorded at $10.3/t, steady w-o-w. Market uncertainty pressured freights for this route, and there was a lack of fresh fixtures, as China was on its Labour Day holiday.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $7.9/t on 7 May, decreasing by $0.1/t w-o-w. According to sources, major Australian miners Rio Tinto and BHP were seen booking Capesize vessels from a Western Australia port to Qingdao at around $7.9/t. Shipment is scheduled for 20-24 May.

- Brazil-China: Freights for Capesize vessels from Brazil to China fell this week. Rates from Tubarao to Qingdao Port were assessed at $19.2/t on 7 May, dipping by $0.65/t w-o-w. As per sources, freights fell due to limited fixtures, with most cargoes having forward loading dates, reducing near-term demand.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao Port decreased by $0.3/t w-o-w to $14.4/t amid minimal market activity, reflecting weak demand for tonnage.

Leave a Reply