- Billet, sponge iron tags drop m-o-m

- IF-BF rebar price gap widens in Apr

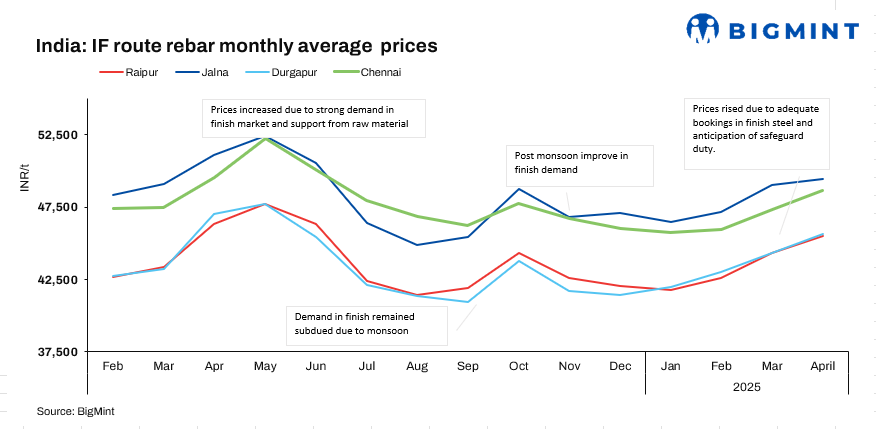

India’s induction furnace (IF) rebar prices declined in April 2025, with rebar (Fe 500) prices falling by INR 200-2,100/tonne (t) m-o-m, according to BigMint’s analysis. The price correction was largely attributed to subdued buying activity across regions.

The sharpest declines were seen in the northern and eastern regions, where prices dropped by INR 2,000/t in Delhi and INR 2,100/t in Durgapur. In the central region, Raipur witnessed a decrease of INR 1,300/t m-o-m. In the south, Bangalore saw a notable drop of INR 1,700/t, while Chennai registered a relatively minor correction of INR 200/t.

Meanwhile, in the west, Ahmedabad recorded a decline of INR 900/t m-o-m, while Mumbai and Jalna saw moderate price drops of INR 200/t and INR 600/t, respectively.

Overall, the market showed a softening trend amid limited demand, with prices adjusting accordingly across key consumption hubs.

Moderate trading activity with steady buying was observed across most regions in the finished steel market. Buyers, having already stocked up on material in March at higher prices, refrained from bulk purchases and limited their bookings to need-based buying.

Uncertainty over price trends, following the imposition of the safeguard duty, also contributed to cautious sentiment. However, the duty had little to no significant impact on the IF route market. To stimulate demand, manufacturers reduced offers, which supported sales momentum. Smooth lifting and dispatching activities, coupled with consistent buying, helped maintain inventory levels at around 7-8 days.

Notably, India’s rebar production (via both IF and BF routes) stood at 49 mnt in FY’25, marking a 10% increase from approximately 44.5 mnt in FY’24, as per JPC data.

Factors impacting market

Raw material prices drop m-o-m: The decline in finished steel prices was largely driven by a drop in prices of key raw materials – steel billets and sponge iron – used in IF-route production. Weakened buying interest and limited trade activity across several markets prompted manufacturers to cut prices. Considering the Raipur market as a benchmark, billet prices fell by INR 1,500/t m-o-m to INR 40,300/t, while sponge iron (PDRI FeM 80% +/- 1) saw a sharper decline of INR 2,150/t m-o-m, settling at INR 24,150/t exw (spot prices taken from 31 March to 30 April 2025).

However, BigMint’s Odisha iron ore fines index (Fe 62%) rose by INR 150/t m-o-m to INR 5,250/t in April 2025. Prices rose amid active demand from steelmakers for fresh environmental clearance (EC) material and supportive bids in the Odisha Mining Corporation (OMC) auction. Offers from miners were higher last month.

BF-route prices rise m-o-m: Trade level BF rebar prices rose by INR 2,100/t m-o-m to an average of INR 57,100/t exy-Mumbai amid a hike by mills in the first half of April 2025. Limited material availability in the distribution network kept prices supported.

Furthermore, Tier-1 mills rolled over rebar list prices for early-May 2025 deliveries compared to end-April 2025 levels. Post-revision, list prices hovered at around INR 56,000-57,000/t on landed basis.

Currently, the gap between IF and BF-route rebar prices is 8,200/t. While, the price gap between the two widened to INR 7,600/t in April from INR 5,540/t in March on monthly average basis.

Outlook

Market participants expect prices to remain stable or slightly weak in the near term. However, any pick-up in restocking activity by buyers ahead of the monsoon could provide price support later in the month.

Leave a Reply