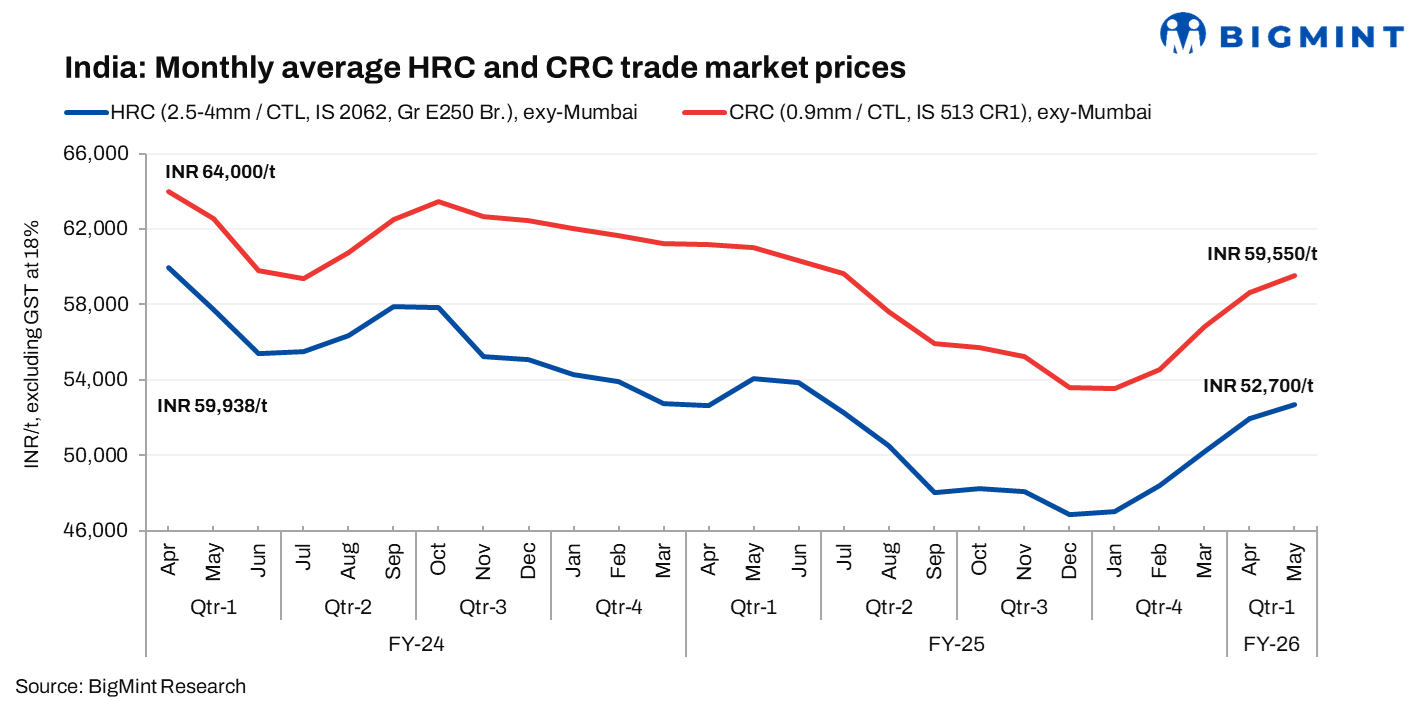

- Trade prices rise m-o-m amid falling imports, tight supply

- List price hikes may face resistance amid muted demand

Leading Indian steel manufacturers have officially raised the list prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) by INR 500-1,000/tonne (t) ($6-12/t) for May 2025 sales. Additionally, some new market entrants have not yet announced any price hikes for the same products. While multiple mills have confirmed this price hike, official announcements from a few others are still pending.

Leading steel manufacturers’ list prices of HRCs (2.5-8 mm, IS2062, Gr E250, Br.) were at INR 53,000-54,000/t ($627-638/t) ex-Mumbai. CRC prices (0.9 mm, IS513 CR1) ranged within INR 59,000-60,500/t ($697-715/t).

Market scenario

Domestic trade prices increase m-o-m: In India’s trade segment, the average monthly price of HRCs rose by INR 700/t ($8/t) m-o-m to INR 52,700/t ($623/t) in April 2025. CRC saw a sharper increase of INR 1,000/t ($12/t) to INR 59,600/t ($664/t).

The price uptick was driven by a sharp decline in lower-priced imports and legacy inventory. Additionally, there were supply constraints, with ongoing maintenance at Tata Steel’s Jamshedpur plant and the upcoming maintenance at JSW’s Dolvi facility expected to further tighten supply. However, buyers undertook need-based procurement at lower tags, which limited any drastic price increase.

“The supply disruptions from ongoing and upcoming maintenance have offset the impact of weak demand,” a market participant noted. “While older inventories are nearly exhausted, fresh inquiries remain scarce. We are only catering to existing clients and mostly on credit, as financial constraints are tight.”

Downtrend in imports continues: As per BigMint’s vessel line-up data, bulk imports of HRCs and plates continued to decline m-o-m. To illustrate, the cumulative import volume touched 306,260 t in April 2025, while it was 408,762 t in March 2025 and 413,020 t in February 2025.

Export trends: Indian steel producers are currently focused on the domestic market, supported by steady demand and stronger price realisations. Meanwhile, Chinese and Japanese suppliers continued to dominate key export markets such as the Middle East and Vietnam, intensifying competition. Additionally, weak demand and cautious purchasing in the European Union limited India’s export opportunities.

Weekly assessment update

As of 6 May 2025, BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) decreased by INR 200/t ($2/t) w-o-w to INR 52,600/t ($620/t). However, CRC (IS513, Gr O, 0.9 mm/CTL) prices rose by INR 100/t ($1/t) w-o-w to INR 59,600/t ($703/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Outlook

HRC and CRC tags may remain range-bound, as mills’ list price hikes may face resistance amid muted demand. Supply remains constrained due to plant maintenance and declining imports, but tepid buyer interest and cautious procurement could limit further price upside. Export prospects stay weak, keeping domestic market dynamics in focus.

Leave a Reply