- Turkiye sees limited trades, sentiments stable

- India favours short-haul cargoes, skips new bookings

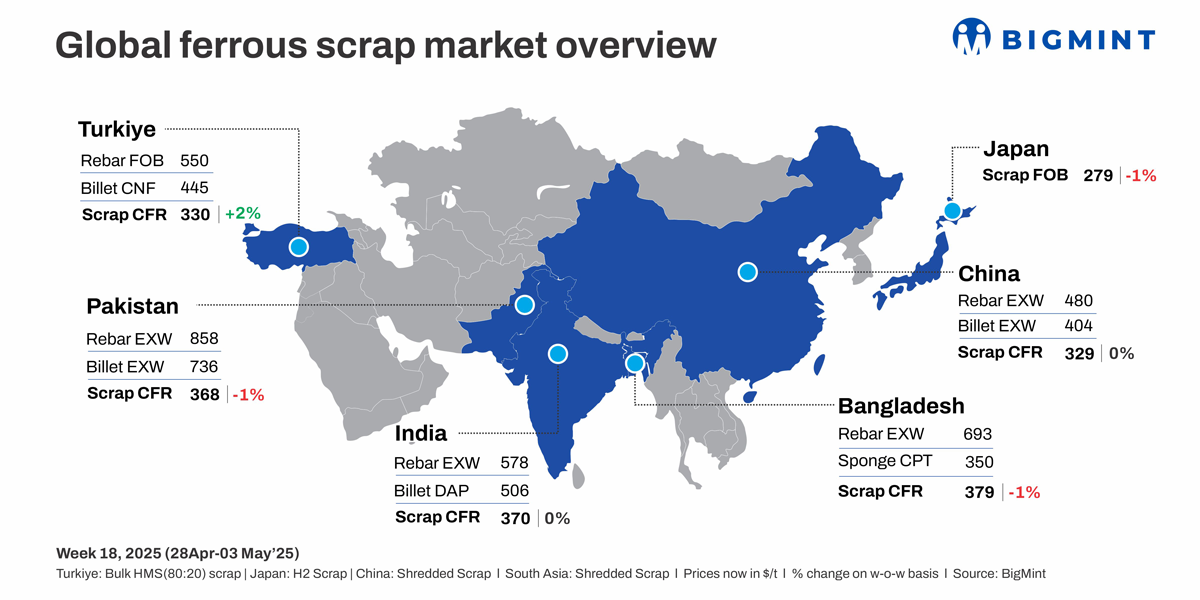

Global ferrous scrap prices remained rangebound this week as markets faced weak steel demand, cautious buying, and seasonal slowdowns. Stable offers in Turkiye and India contrasted with softer trends in Pakistan, Bangladesh, and Vietnam, while limited recovery in US export prices and Japan’s continued weakness kept sentiment mixed.

Turkiye: Imported scrap prices edged up w-o-w, with US and Baltic HMS 80:20 offers at $330-335/t CFR, while buyer interest remained limited to $325-328/t levels. Sellers held firm on prices amid tight supply and high collection costs, while mills remained cautious due to weak rebar demand and a narrow $210/t scrap-to-rebar spread, limiting trades.

As per market insiders, recyclers continued to hold offers firm, especially for US-origin cargoes at $335-340/t CFR, amid expectations of a near-term price floor, supported by tight supply and strong resistance to lower bids.

Rebar market momentum lent further support to scrap sentiment, with FOB prices rising to $550-555/t driven by seasonal demand, earthquake reconstruction, Ukrainian interest, and higher billet offers from China. Mills cautiously adjusted list prices upward, showing increased confidence.

India: The imported scrap market remained stable this week, with UK-origin shredded scrap steady at $370/t CFR Nhava Sheva, nearly unchanged from last week’s $371/t. Buyers stayed cautious amid falling Turkish prices, seasonal slowdown, and weak domestic steel demand. Shredded bids held at $365/t, reflecting a consistent gap between buyer and seller expectations, which kept trades limited. HMS 80:20 offers from the UK, West Africa, and South Africa ranged between $345-360/t CFR, but high freight and full inventories further suppressed buying interest.

Pre-monsoon hesitation and tight liquidity dampened trade. UK suppliers kept shredded offers firm, tight dockside supply and collection costs above EUR 230/t FOB, but Indian buyers were hesitant. Buyers focused on short-haul or on-water cargoes, waiting for clearer price direction before committing.

Around 22,000-23,000 t of imported scrap were booked in India this week. This included 6,000-7,000 t of HMS 80:20 at $347-365/t CFR and 2,000-3,000 t of shredded scrap priced around $365/t CFR. The rest comprised HMS 1, LMS bundles, and approximately 11,000 t of busheling scrap, which traded at $385/t CFR.

Pakistan: The imported scrap market remained sluggish this week, Prices hovered near 4.5-year lows, last seen in November 2020. due to weak steel demand, falling billet and rebar prices, and global uncertainty leading to bearish sentiment in Turkiye. Mills operated at reduced capacity while buyers stayed cautious, pushing shredded scrap bids to $364-370/t CFR Port Qasim against offers of $370-375/t. Shredded prices fell 1% w-o-w to $368/t from $370/t, reflecting bearish sentiment.

UAE-origin shredded was offered at $385-390/t CFR but remained unviable, with no deals reported. Domestic scrap stood at PKR 134,000-138,000/t ($480-494/t), billets at PKR 200,000-205,000/t ($718-736/t), and rebars at PKR 235,000-240,000/t ($843-861/t).

Bangladesh: Imported scrap prices in Bangladesh remained sluggish this week, with buyers cautious due to weak finished steel demand, rising production costs, and currency concerns. Mills delayed fresh bookings, focusing on July shipments. Shredded scrap prices declined 1% w-o-w to $379/t from $381/t. Offers for Australian shredded scrap at $380-385/t CFR saw limited interest, while HMS 80:20 bids were around $360/t CFR, lower than $365-370/t offers.

Domestic scrap held at BDT 54,000-55,000/t ($445-453/t), and rebar prices ranged from BDT 84,000-85,000/t ($692-700/t) in Chattogram to BDT 81,000-82,000/t ($667-675/t) in Dhaka.

Japan: H2 scrap export market remained weak due to slow domestic movement, fewer export deals, and limited operations during the Golden Week. The long-standing West-East regional price gap saw a correction in April.

Offers fell as suppliers adjusted to weaker deep-sea and domestic prices. BigMint assessed H2 at JPY 40,400/t ($278/t) FOB Tokyo Bay, down JPY 500/t w-o-w.

Domestic prices also declined, with the Japan Iron and Steel Association reporting a JPY 800/t weekly drop to JPY 38,300/t ($267/t) across key regions. Chubu saw the steepest fall of JPY 1,500/t.

Vietnam: Imported scrap prices softened as Japanese H2 offers fell to $325/t CFR amid weak demand and dong depreciation. A major mill booked shredded at $345-346/t CFR. Domestic prices held steady, but falling billet prices and reduced buying kept sentiment weak.

South Korea: POSCO resumed imports in late April, bringing in 41,800 t of scrap, led by Pohang with 15,000 t. A KRW 5/kg ($4/t) price cut and rising supply may pressure sentiment, while reduced holiday-season output could affect early May trends.

US: Ferrous scrap export prices rose by $5/t this week, with HMS 80:20 at $310/t and shredded at $330/t FOB East Coast. The rebound follows 2.5-year lows and is driven by US market uncertainty and slight recovery in Turkiye’s deep-sea demand.

Leave a Reply