- Warm weather onset marginally boosts construction

- Lower input costs, growing profits boost Mar output

- Tariff concerns likely to restrain volumes in short term

Morning Brief: China’s crude steel production inched up by 1% y-o-y to 259 million tonnes (mnt) in January-March 2025 (Q1CY’25), reversing the slight decline – of 1.5% y-o-y – seen over the first two months of the year. The slight recovery defies expectations of a continued downtrend, following the government’s plans to cut production to battle overcapacity in the steel industry.

Notably, this 1% uptick in Q1CY’25 comes amid a 4.6% y-o-y and 12% m-o-m increase in crude steel production to 93 mnt in March, a 10-month high according to National Bureau of Statistics (NBS) data.

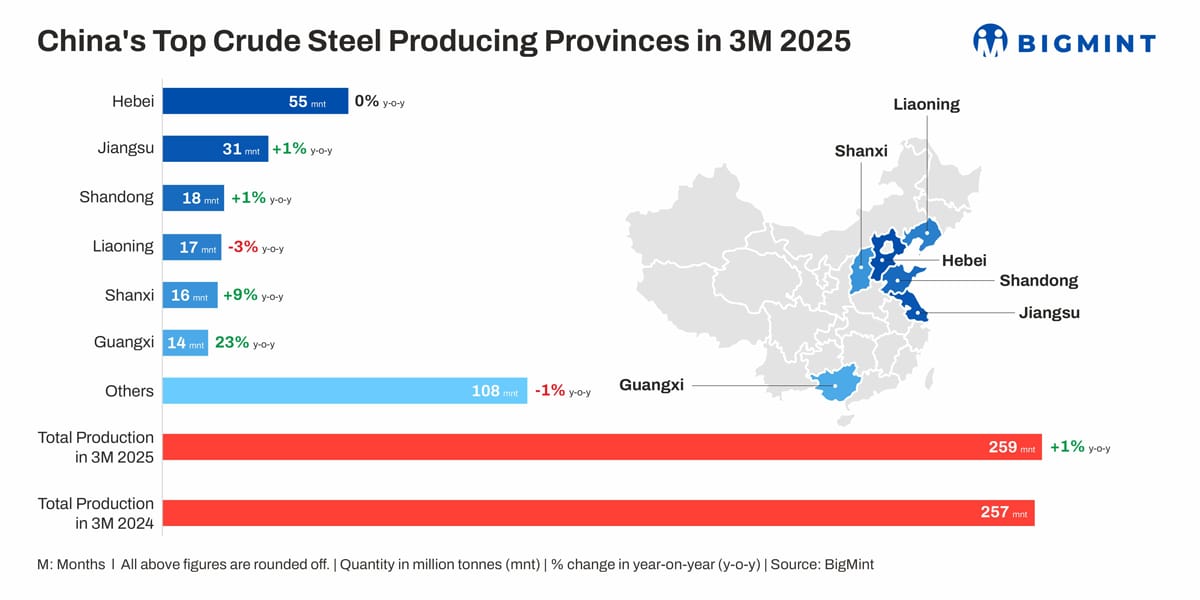

Province-wise break-up

Among the top six crude steel-producing provinces, Hebei, the largest contributor, logged 55 mnt in Q1CY’25, flat y-o-y. Jiangsu and Shandong followed, up by a marginal 1% y-o-y at 31 mnt and 18 mnt, respectively. Liaoning saw a 3% y-o-y dip to 17 mnt, while Shanxi’s output moved up by 9% to 16 mnt. Additionally, Guangxi surged by a robust 23% to 14 mnt.

Factors impacting China’s crude steel production in Jan-Mar’25

Domestic demand shows slight improvement: Construction demand picked up slowly in February and March, with the onset of warmer weather.

To illustrate, infrastructure investment growth averaged 5.6% in Q1CY’25, with March recording 5.8% in comparison to 5.7% in February and 5.4% in January. While this was lower than Q1CY’24’s average of 6.3%, there was a marked improvement from the 4.3% recorded in October-December 2024 and 4.5% in July-September 2024. In tandem, the business activity index for the construction segment climbed up by 0.7 points m-o-m to 53.4 in March, the highest since June 2024, according to the NBS data.

Manufacturing activity also gained pace in this quarter, bolstered by policy support. The manufacturing PMI stood at a one-year high of 50.5 points in March, up from 50.2 in February and 49.1 in January. Additionally, automobile production surged by 14.5% y-o-y to 7.56 million units in January-March 2025.

However, the realty segment continued to struggle, as evidenced by a 9.8% decline in investment growth against 9.2% a year ago.

Production costs decline as raw material tags fall: Prices of key raw materials – iron ore and coking coal – plunged in March, bringing down steelmaking production costs.

The benchmark Australian-origin Fe62% iron ore fines index dropped $4.65/t to $102.5/t CNF Rizhao, China, in March from $107.15/t in February. Meanwhile, Australian premium hard coking coal (PHCC) was down by $13/t at $175/t FOB Hay Point in March compared to $188/t in the previous month. Meanwhile, met coke (25-50mm, quasi-grade I) stood at RMB 1,331/t ($183/t) exw-Tangshan, Hebei, in March, reflecting a drop of RMB 97/t ($13/t) m-o-m from RMB 1,428/t ($196/t).

Taking advantage of lower input costs, steelmakers ramped up production in March, especially given uncertainties in future market direction due to potential production cuts and escalating trade frictions.

Profitability improves as input costs dip: Notably, 53% of producers were able to generate profits in March compared to 25% during the same period last year, as reported by Mysteel Global. This is primarily attributed to the decline in raw material prices and increase in trade momentum. These two factors were able to keep profit margins healthy amid range-bound steel prices.

Hot-rolled coil (HRC) prices (thickness: 4.5-12 mm, width: 1500 mm) fell a slight RMB 34/t ($5/t) to RMB 3,340/t ($459/t) in March against RMB 3,374/t ($464/t) in February. Rebar tags (16 mm, HRB400E, Grade 3) were stable m-o-m at around RMB 3,300/t ($454/t) exw-Donghua in March.

Additionally, major steelmakers also announced robust net profits in Q1CY’25. Baosteel’s net profit surged by 26% y-o-y to $0.34 billion, and HBIS Company’s was up a massive 46% y-o-y to $32.2 million. Meanwhile, Shagang’s net profit rose 38% y-o-y to $9.5 million.

Higher profit margins naturally enabled steelmakers to invest further in production.

Steel mills ramp up exports through aggressive pricing: Strong export momentum also incentivised steel production in China. Exporters ramped up activity amid fears regarding worsening geopolitical tensions, which could significantly slow down trade in the seaborne market.

China’s steel exports rose 6.3% in January-March 2025 to 27.43 mnt, the highest volume recorded in Q1 since 2016. Notably, exports increased despite trade restrictions imposed in major importing destinations such as Vietnam, South Korea, and Japan. This was because Chinese steelmakers adopted predatory pricing tactics. On average, Chinese benchmark HRC offers in Q1 were at $470/t FOB, the lowest among the key exporting countries such as Japan ($473/t), India ($502/t), and Russia ($482/t).

Outlook

China’s crude steel production is likely to plateau in April or even shrink, given that domestic demand is weaker than expected despite a slight improvement. Moreover, mounting concerns regarding trade tariffs and restrictions may keep output depressed. While the government has announced plans to cut production, the exact specifics or quantum are still not known. The overall uncertainty in the sector may weigh on volumes in the near term.

Leave a Reply