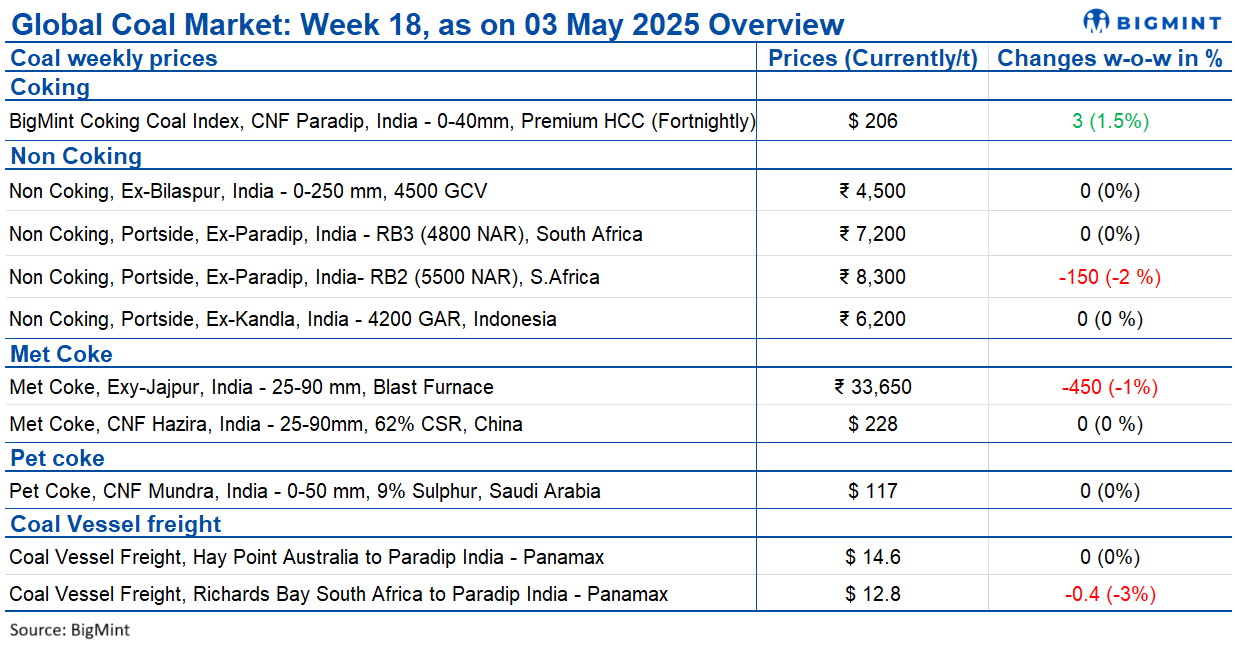

India’s imported and domestic coal market sentiments remain subdued and cautious. Buyers are holding back from making large purchases due to sufficient stock levels, weak downstream demand, and market uncertainty. While some deals were closed in the coking coal market, buyers remain hesitant amid fluctuating expectations.

The portside thermal coal markets for both South African and Indonesian grades are experiencing limited activity, with stable to slightly declining prices. Rising coal inventories at ports contrast with declining stock at power plants, suggesting mixed demand signals. Overall, the coal market is showing stability but slight bearishness persists.

Indonesian coal prices stable at ports

Portside prices of Indonesian thermal coal in India remained steady this week, with 5000 GAR at INR 7,800/t (Kandla), 4200 GAR at INR 6,200/t (Kandla), and INR 6,100/t (Vizag). Only 3400 GAR coal saw a INR 100/t dip to settle at INR 4,800/t at Navlakhi. Limited Chinese buying redirected shipments to India, keeping pressure on prices. Portside coal inventories rose 7.4% to 13.29 mnt, while power plant stocks fell to 56.69 mnt, raising supply concerns at select facilities. Global Indonesian coal prices also declined, with 5800 GAR at $80.31/t and 4200 GAR at $48.42/t, indicating a near-term softening trend.

South African coal portside prices dip

South African thermal coal prices at Indian ports eased this week amid sluggish demand and limited trades. RB2 (5500 NAR) prices dropped INR 100/t w-o-w to INR 8,350/t exw-Gangavaram, while RB3 (4800 NAR) remained stable at INR 7,200/t. RB2 offers at Vizag ranged between INR 8,000-8,200/t, with a 16,000 t deal concluded at lower levels. Low sponge iron prices and higher domestic coal usage kept most buyers inactive. Export prices also softened, with RB2 at $75/t FOB. Prices may stay under pressure unless demand improves.

Domestic coal prices steady

Domestic coal prices in India remained unchanged this week, with 4500 GCV and 5000 GCV grades assessed at INR 4,500/t and INR 4,950/t, respectively, exw-Bilaspur. The market remained quiet as most buyers held adequate stock and refrained from fresh bookings. In SECL’s recent auctions, only 10-20% of the total non-coking coal offered was sold, reflecting subdued demand and weak buying interest. Overall, firm supply and sufficient inventories continue to keep prices stable, with no immediate signs of upward movement unless buying activity picks up in the coming weeks.

Met coke prices drop in eastern India

Met coke prices in India showed mixed movement this week, with a notable INR 450/t drop in Jajpur to INR 33,650/t exw, while prices in Gandhidham held steady at INR 32,200/t exw. The fall was led by declining pig iron prices, reduced steel production, and increased scrap usage. Durgapur pig iron prices dropped INR 1,200/t to INR 33,300/t by 2 May. Australian coking coal rose slightly to $191/t FOB, but supply remains tight. Meanwhile, Chinese met coke prices rose RMB 50-55/t, with producers proposing a second hike. However, Indian demand remains weak, likely keeping domestic coke prices under pressure in the near term.

BigMint’s coking coal index up $3/t

BigMint’s premium hard coking coal (PHCC) index rose to $206/t CNF Paradip on 28 April, up $3/t from mid-April, driven by Australian supply issues and recent deals. Two deals totalling 50,000 t were closed at $205-209/t CFR. Canadian coal is also being offered in India. Meanwhile, offers at $215-216/t persist, but buyers expect stable prices ahead. In China, met coke prices rose amid restocking before holidays. Some mills seek further hikes, but weak steel demand and high inventories may cap gains post-holiday. Sentiment remains cautious despite recent futures rebound.

Nayara, MRPL lower pet coke prices for May

Nayara Energy and MRPL have reduced their petroleum coke prices effective 1 May. Nayara’s price now stands at INR 13,860/t, down by INR 1,070/t from April. MRPL slashed its rates by INR 1,240/t, with prices at INR 10,430/t for road supply and INR 10,130/t for rake/barge. In April, both refiners had kept their prices unchanged. The latest reductions come amid broader market adjustments and weak buying interest, with refiners responding to subdued demand and aligning prices with prevailing trade sentiment and inventory positioning.

US pet coke prices fall slightly

Imported US pet coke prices in India declined this week, falling by $2/t w-o-w on the east coast to $106/t CFR, and by $1/t on the west coast to $105/t CFR. The slight dip in May-June delivery offers is due to increased availability, with some cargoes originally meant for China diverted to India. Meanwhile, Saudi-origin pet coke prices stayed flat at $114-120/t CFR. Buying interest remained weak, with no significant uptick in demand. Market participants are monitoring price trends closely, especially amid steady supply and sluggish consumption outlook across key regions.

India coal freight trends mixed

Coal freights to India showed mixed movement this week. Atlantic route rates rose amid tight vessel supply, while oversupply capped gains elsewhere. Indonesian freights to India rose by $0.3/t to $14.1/t on reduced vessel availability and firm utility buying ahead of summer. In contrast, South Africa-India rates fell $0.4/t to $12.8/t due to ample vessel supply. Australia-India freights remained stable at $14.6/t. Thermal coal inventories at Indian ports rose 7.4% w-o-w to 13.29 mnt. Meanwhile, Baltic freight indices rose, with the BDI up 112 points to 1,373, reflecting increased chartering and firm demand for coal shipping globally.

Leave a Reply