- Raw material tags dip INR 500-800/t w-o-w

- Semi-finished steel prices fall by around INR 500/t

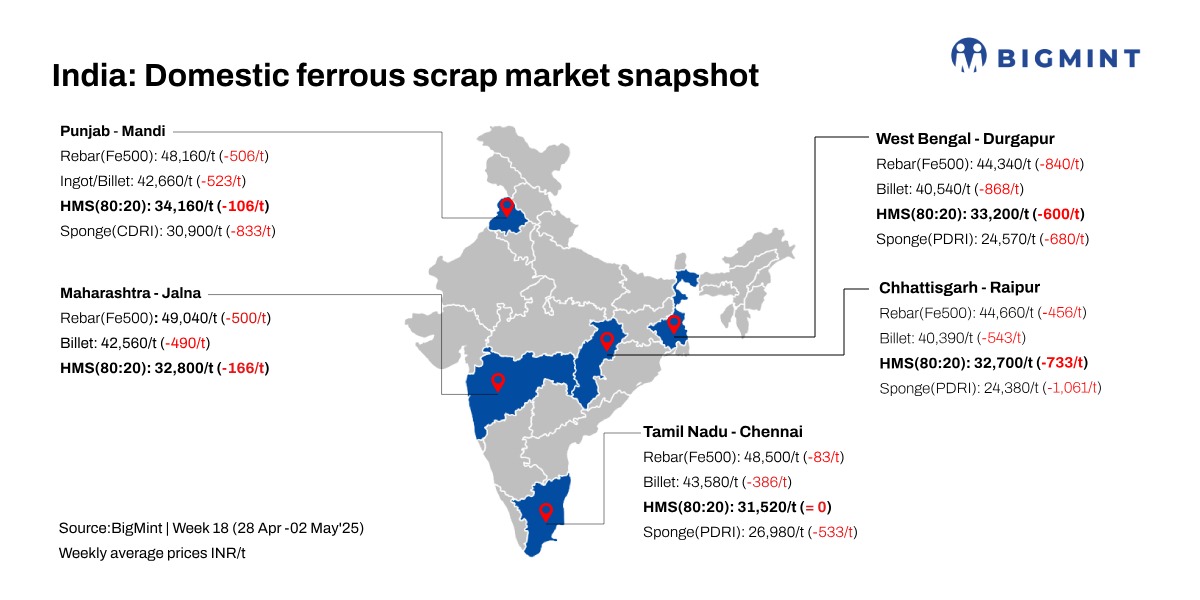

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, inched up by INR 100/tonne (t) d-o-d to INR 36,800/t DAP on 2 May, 2025. W-o-w, scrap prices decreased by INR 100-500/t in the region.

The steel market in Mandi Gobindgarh remained sluggish, with buyers largely inactive amid expectations of further price corrections. On the supply side, steel manufacturers are facing mounting sales pressure, prompting them to lower their offer prices across various steel segments.

However, many steelmakers believe prices may have bottomed out and they are expecting a pickup in demand later this month. With the onset of the monsoon expected next month, active buying is likely to resume, particularly around mid-May. Additionally, the market is looking to primary steel mills for potential price support, as secondary producers expect an upward revision in offers during the first week of the month.

A mill owner informed, “Steelmakers expect ingot and billet prices to remain rangebound between INR 42,300-INR 43,300/t in the near term, amid cautious buying and limited price triggers.”

Imported scrap offers, deals

- Bahrain-origin HMS offered at $366-367/t CFR Mundra.

- EU-origin HMS 1+premium grade offered at $370/t CFR Mundra.

Around 1,000 t of Kuwait origin HMS 1 booked at $370/t CFR Mundra.

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi experienced a d-o-d decline of INR 100/t, settling at INR 30,600/t DAP. Over the course of the week, prices have fallen by INR 833/t.

Steel-grade pig iron prices in Ludhiana remained stable at INR 37,000/t DAP. On a weekly basis, prices saw a more significant reduction of INR 576/t.

Steel market trends

In Mandi Gobindgarh, steel ingot prices remained stable at INR 42,500/t DAP. Similarly, semi-finished steel prices across major trading hubs saw a decline of INR 100-200/t d-o-d. In Mandi, semi-finished steel prices fell by INR 533/t w-o-w.

Rebar prices in Mandi decreased by INR 100/t d-o-d to INR 48,000/t. However, on a weekly basis, rebar prices dipped by INR 506/t on a weekly basis with weak steel demand.

Overview of Mumbai market

Prices for Rebar (Fe 500) on the Mumbai IF route decreased by INR 300/t at INR 49,000/t exw. Limited buying activity was seen in the market for finished steel as buyers awaited for further clarity. Scrap (HMS 80:20) is INR 33,300/t DAP. The conversion spread between scrap and billet is around INR 9,700/t.

CR busheling auction result

A top electric motors and generators producer sold around 1,000 t of CR busheling scrap from its Faridabad, Haryana, unit at INR 35,800/t ex-works, a decrease of INR 1,500/t from last month’s auction.

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread stood at INR 5,600-5,900/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at $345-350/t, which equates to approximately INR 31,734/t (including freight). Local HMS (80:20) prices in Mumbai fell by INR 100/t to INR 33,300/t DAP. Indicative prices of shredded from Europe stood at $370/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 16,100/t.

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply