- Low buying interest amid uncertainty

- RB2 coal offers drop on weak demand

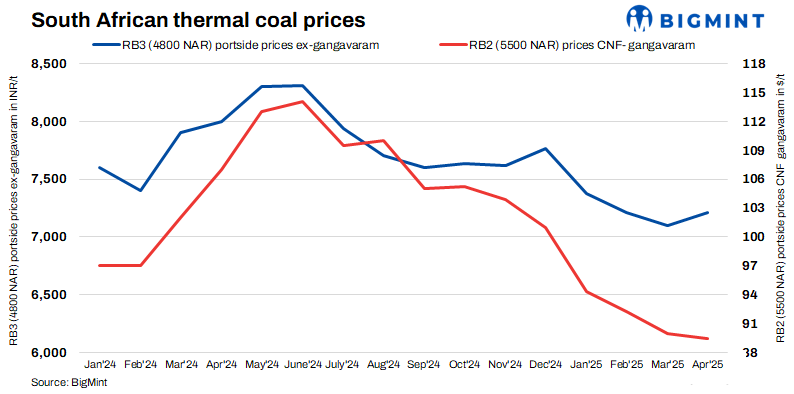

The imported South African thermal coal market at Indian ports remained sluggish this week due to continued weak demand following a drop in sponge prices in the domestic market. BigMint’s latest assessment showed RB2 (5500 NAR) prices slipping by INR 100/tonne (t) w-o-w to INR 8,350/t exw-Gangavaram. RB3 (4800 NAR) remained stable at INR 7,200/t.

At Vizag, offers for RB2 were heard between INR 8,000-8,200/t. A deal for 16,000 t of RB2 was heard concluded at lower prices.

Traders noted that only buyers with urgent needs were active in the market, while most sponge iron producers stayed away due to domestic coal usage, followed by a drop in sponge iron prices.

However, thermal coal inventories at Indian ports rose 7.4% to 13.29 million tonnes (mnt) in week 17 of CY’25 from 12.37 mnt in the previous week.

Market highlights

Export prices ease: South African RB2 export offers dropped to $75/t FOB, while RB3 remained unchanged at $63/t FOB as of 2 May. Miners are reluctant to go beyond these level.

Domestic coal prices stable: 4500 GCV and 5000 GCV grades remained at INR 4,500/t and INR 4,950/t exw-Bilaspur, respectively as most of the buyers with sufficient stock avoided fresh bookings. In recent SECL auctions, only 10-20% of the total non-coking coal offered was sold, highlighting weak demand and lack of buying interest.

Sponge iron under pressure: Domestic C-DRI prices fell again by INR 800/t w-o-w to INR 25,900/t exw-Rourkela, further denting demand for thermal coal. The market witnessed a downtrend, as buyers stayed silent amid fluctuations in the market.

Outlook

With high buffer stocks at ports, weak sponge iron prices, and limited end-user participation, South African portside coal prices are expected to remain under pressure. Spot trading activity may stay thin unless delivered costs drop significantly or buying sentiment improves.

Leave a Reply