- Turkish scrap inches up despite cautious market sentiment

- Asian and Middle Eastern markets stay subdued

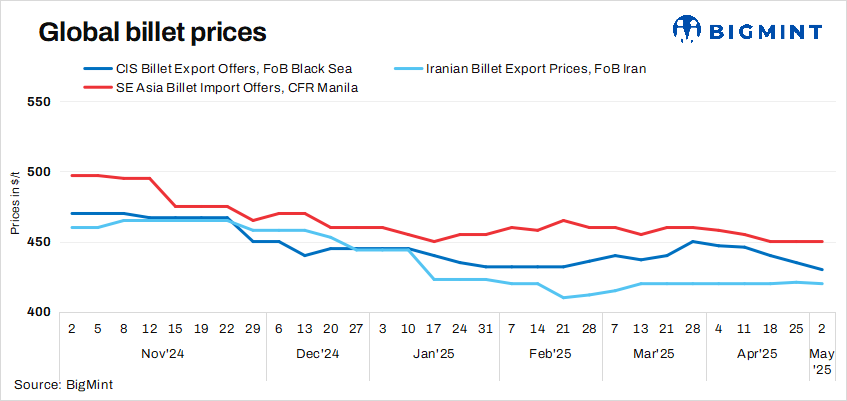

In week 18 of CY’25, the global steel billet market remained relatively stable, showing limited volatility compared to recent weeks. Billet prices held steady across regions, reflecting a supported market sentiment amid subdued activity. The slight uptick in global scrap provided support to billet producers, though it was not enough to significantly close any major trades. Overall, the market maintained balance, with participants closely watching raw material trends and demand signals before making new moves.

The Turkish deep-sea imported scrap market saw sluggish trading this week, though sentiment showed mild improvement as offers edged up by $2/t w-o-w on 2 May after previously hitting a three-year low. Buyer activity from mills remained limited, keeping sellers cautious. However, a strong lira is providing some price stability, while a slowdown in scrap inflows may lead to tighter supply in the near term. US-origin HMS 80:20 bulk scrap was assessed at $330/t CFR Turkiye, marking a $2/t weekly gain on 2 May. While the market appears to have found a potential floor, Turkish mills continue to push for further discounts. In contrast, sellers-particularly of EU-origin cargo are resisting pressure, holding firm near the $325/t CFR level.

In China, billet prices continued to edge down gradually, weighed by limited demand. While last week saw a brief sense of optimism driven by rumours of possible tariff reductions, the current week failed to confirm or sustain that sentiment. Southeast Asian markets also remained largely sluggish, with limited buying activity across key regions. Meanwhile, in the Middle East, billet production was impacted by recurring power shortages and tepid demand, as market participants remained cautious in their buying decisions.

Market highlights

- Billet prices in the Philippines remained unchanged w-o-w at $450/t CFR Manila as of 2 May, despite a quiet market. Offers were heard in the range of $445-455/t CFR for 5sp grade, sources informed BigMint. Both traders and end-users continued to adopt a wait-and-watch stance, uncertain about the near-term price direction.

- The Vietnamese billet export market remained largely inactive during the week as trading was halted due to market closure, with no major bulk deals reported.

- Iranian semis exporters remained active in week 18 despite challenges following a major explosion at Bandar Abbas port on 26 April. The prices were steady w-o-w at $420/t FOB Iran. The incident disrupted port operations, leading to delays in steel-related shipments and heightened market uncertainty, particularly across the MENA region. Market participants are cautious, with many holding off on new shipments until infrastructure is restored-estimated to take another two to three weeks. The prices refused to increase due to lack of demand in the downstream sector.

Leave a Reply