- Around 300,000 t of exports deals heard

- Benchmark global fines prices drop to $98/t CFR China on 30 Apr’25

The Indian iron ore export market witnessed a slowdown this week, largely impacted by subdued buying interest from Chinese mills ahead of the Labour Day holidays in China (1-5 May, 2025). Market participants noted that Chinese buyers were largely procuring on a need-only basis from port inventories, leading to a significant dip in fresh seaborne buying interest.

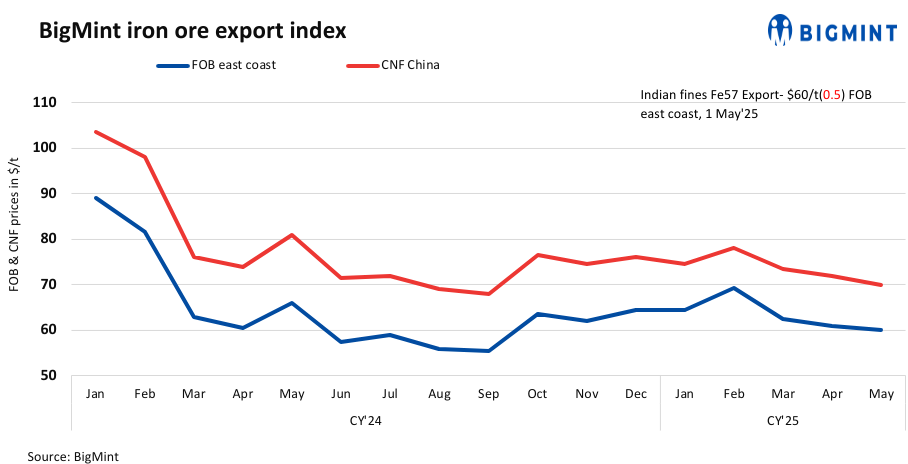

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index inched down by $0.5/t w-o-w to $60/t FOB east coast, India, on 1 May. Trade activity in the Indian Ocean remained thin, but a few exporters received inquiries and concluded deals ahead of market closing. The discount for Fe57% fines was recorded at 21-23% but even this failed to boost deals.

Despite the overall weak sentiment, a few Indian miners and traders managed to close small deals totalling around 325,000 t of Fe50-57% material. These deals mostly involved lower-grade material, catering to buyers looking for discounted cargoes.

Meanwhile, Australian miners have narrowed discounts for their special low-grade fines (Fe56.7%) to 13.75% for April delivery (14.25% in April), which may lower the pressure on Indian fines in near term.

An exporter commented, “Although volumes were down, some trades happened with selected buyers, mostly for low Fe content cargoes. The majority of these deals were concluded by miners while traders remained cautious.”

Exporters continued to face margin pressures, as domestic iron ore prices and margins remaining higher against current international offers. Indian suppliers are struggling to remain competitive as Chinese buyers turn to cheaper alternatives from other origins.

Another miner informed, “We are offering more on the domestic market now, as exports are not viable at current international prices.”

Traders remain cautious, preferring to hold back offers in expectation of improved prices post-holiday. Market participants expect a slight revival in sentiment after the Chinese market resumes next week.

A trader mentioned, “Sentiment could improve after 5 May, depending on how Chinese demand shapes up.”

As per reports, export demand remains limited as Chinese buyers are cautious due to the holiday break. Mills are preferring port stocks to manage short-term needs. The market is now closely watching post-holiday buying activity for clearer direction.

Chinese spot prices fall: Benchmark iron ore fines in China decreased by $3/t w-o-w to $98/t CFR on 30 April. The fall was attributed to reduced trading activity ahead of the Labour Day break. China’s manufacturing PMI missed expectations, and weak mill margins kept market liquidity muted. Mills stayed focused on portside buying, with little push for seaborne cargoes.

DCE iron ore futures down: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2025 contract decreased by RMB 16.5/t ($2/t) w-o-w to RMB 703.5/t ($97/t) on 29 April.

Rationale

- One (1) deal for Fe 57% was reported during this publishing window, and both were considered for price calculations. Therefore, T1 trade was given 50% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received sixteen (16) indicative prices in the current publishing window, and fourteen (14) were considered for price calculation as T2 inputs and given 50% weightage.

Iron ore inventories at major Chinese ports increased by 3 mnt w-o-w to 136.8 mnt on 1 May, according to data published by SteelHome.

Outlook

As per BigMint’s analysis, the market is expected to rebound post-holidays, and trade activity may pick up in the export market.

Leave a Reply