- LME nickel prices fall slightly

- Finished stainless steel market remains stable

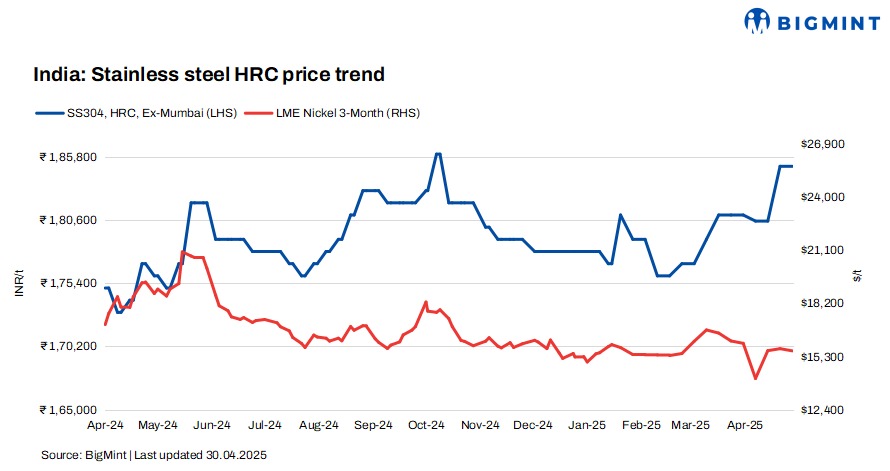

Prices of Indian stainless steel (SS) finished flats and longs held steady w-o-w amid limited market activity.

BigMint’s benchmark assessment for stainless steel (304 series) hot-rolled coils (HRCs) stood at INR 185,000/tonne (t), stable w-o-w, while 304L (25-100 mm) black round bars stood at INR 160,000/t, both ex-Mumbai.

LME nickel tags up, Asian NPI falls w-o-w

At the time of reporting, three-month LME nickel prices stood at $15,545/t, reflecting a slight decrease of 1% from last week’s $15,730/t. Nickel stocks in LME-registered warehouses stood at 201,564 t, range-bound compared to 202,818 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) witnessed a w-o-w decrease of RMB 10/metric tonne unit (mtu) ($2/mtu) to RMB 975/mtu ($134/mtu). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $115/mtu, down by $2/mtu w-o-w.

Finished market remains steady w-o-w

As per BigMint’s assessment, SS 316 HRCs remained stable w-o-w at INR 324,000/t ex-Mumbai.

According to a market participant,“The flats segment continues to remain stable, with no significant changes observed in demand. On the raw material side, LME nickel levels have also remained largely steady, showing minimal fluctuation.”

BigMint’s assessment of SS 316L (25-100 mm) black round bars stood at INR 269,000-271,000/t ex-Mumbai, unchanged w-o-w. Prices of SS 316L (25-100 mm) bright bars stood at INR 286,000-288,000/t ex-Mumbai, steady w-o-w.

A source informed BigMint, “The stainless steel longs market remains steady, driven by need-based buying. Continued reliance on credit-based purchases is exerting financial pressure on mills. Induction furnace (IF) route mills are operating below full capacity, reflecting subdued demand and challenging market conditions that limit production and liquidity.”

Another source mentioned, larger mills are currently struggling to liquidate material, resulting in rising inventory pressure. In contrast, the smaller units are relatively insulated from this trend and are not facing significant inventory buildup.

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 14,050/t ($1,933/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were at $1,910/t.

Raw materials overview

1. Ferro molybdenum: Indian ferro molybdenum prices edged down slightly by INR 5,000/t ($59/t) as against the previous assessment on 23 April. Prices were stable as market showed minimal movements.

Ferro molybdenum prices in India were INR 2,547,000/t ($30,044/t) exw-India, as per BigMint’s assessment on 30 April. Around 35 t of deals were reported last week in the price range of INR 2,490,000-2,550,000/t ($29,372-30,079/t) exw.

2. Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,600/t ($1,189/t) exw-Jajpur, down by INR 700/t ($8/t) w-o-w.

3. Ferrous scrap: India’s imported scrap market remained sluggish last week, with EU-origin HMS 80:20 dropping $2/t to $348/t CFR Nhava Sheva, and shredded prices falling by $4-5/t w-o-w to $370/t CFR. Buyers were cautious due to volatile Turkish prices, weak domestic demand, high freight rates, and full inventories. Market activity slowed as buyers expect further price softness with the approaching monsoon season.

Outlook

In the near term, prices are likely to remain rangebound, with weak demand and subdued buying activity continuing to weigh on the overall market.

Leave a Reply