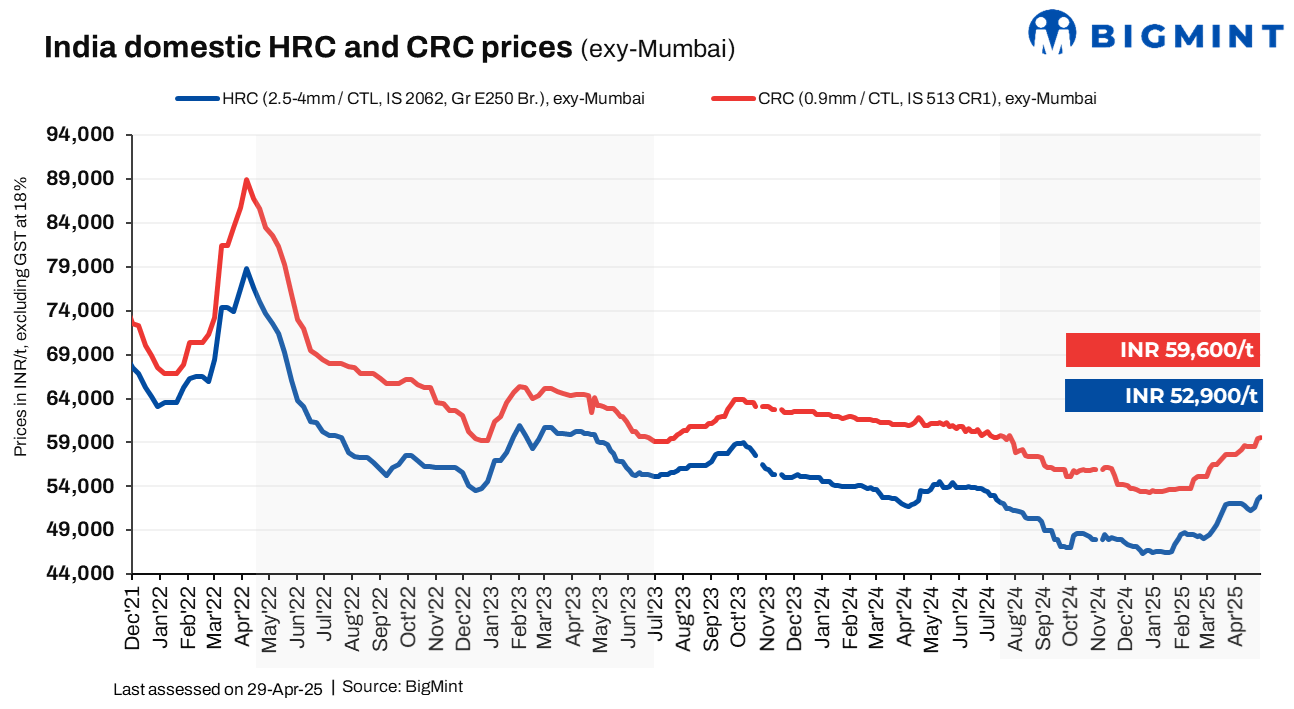

Market updates

Market updatesMill maintenance: Tata Steel has been undertaking a blast furnace maintenance for an extended period. Market sources indicate that JSW’s Dolvi plant may undergo maintenance for 20-25 days next month, though this remains unconfirmed by the company. These planned outages are expected to impact HRC supply in the market.

Market awaits price hike: Demand in the market remains sluggish, with buyers limiting purchases to immediate needs. Liquidity remains tight, as new sales are largely on credit and payment recovery is slow. Additionally, the market is awaiting next month’s price announcement from the mills.

“The market is expected to remain rangebound as buyers resist price hikes. However, with dwindling stocks of cheaper, older material and declining imports, the downside in prices is limited. Caution is advised moving forward,” a market participant noted.

Import trends: India’s bulk imports of HRCs and plates touched 2,83,840 t as of 28 April, based on vessel line-up data from BigMint. Another 94,919 t are expected to arrive shortly next month.

Export trends: Indian mills have reduced their HRC (S275) FOB offers, currently quoted at $585-590/t from main Indian ports for EU-bound shipments. According to sources, the ongoing weakness in exports is primarily due to unfavourable euro-dollar parity. Trade activity in the EU remains subdued as buyers have adopted a cautious stance.

Meanwhile, Indian mills are refraining from actively offering to the Middle East due to aggressive Chinese pricing and better domestic realisations. W-o-w, Indian HRC export offers to the EU have dropped by $10/t, now at $635-640/t CFR Antwerp ($585-590/t FOB east coast India), compared to last week’s $645-650/t CFR.

Outlook

In the near term, HRC and CRC prices may hold firm amid mill maintenance, limited imports, and speculation of list price hikes. However, subdued demand, liquidity constraints, and cautious buying are likely to keep trade activity under pressure. Further upside may be capped unless strong fundamentals or export recovery materialise.

Leave a Reply