- Limited fresh iron ore export inquiries from the east coast

- Baltic Capesize Index (BCI) increases by 211 points w-o-w

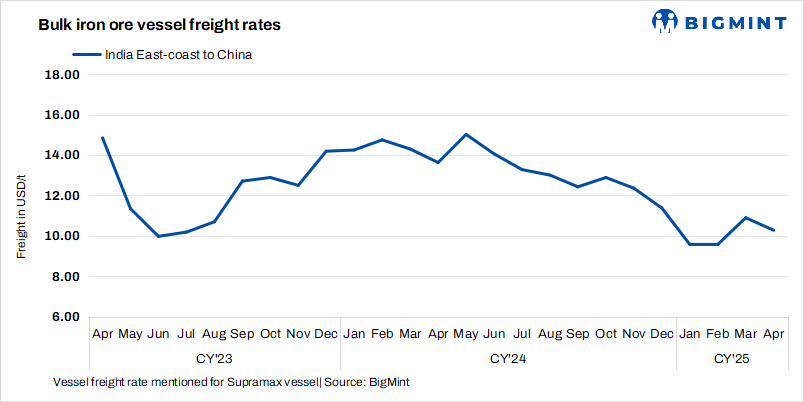

Dry bulk iron ore freight rates from India to China declined this week, driven by subdued spot market activity and a noticeable lack of fresh cargo enquiries, especially early in the week. Market sentiment remained cautious across both Atlantic and Pacific basins, with charterers and owners adopting a wait-and-watch stance due to the absence of clear cues. This hesitancy translated into limited fixture activity, resulting in weaker vessel demand and a softening in freight rates.

In the east coast of India the downtrend was further accentuated owing to less deals happening for exports against availability of ships at ports. In addition, easing bunker prices contributed to the decline in voyage costs, further pressuring freight rates on the India-China route.

“Due to the absence of cargoes, vessels are ballasting out from the east coast of India, leading to downward pressure on freight levels,” a source informed.

Capesize freight rates went up because there was steady demand and fewer ships available, especially in the Atlantic. Even though activity in the Pacific was quiet, with only one big miner fixing ships, the market stayed positive due to expectations of more cargoes after the Labour Day holidays.

Factors influencing freights

- Baltic indices increase w-o-w: The Baltic Dry Index (BDI) was recorded at 1,373 on 28 April, increasing by 112 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 1,889, rising by 211 points w-o-w, reflecting a pick up in demand. The Baltic Supramax Index (BSI) also edged up by 27 points w-o-w to 977 points.

- China’s iron ore spot prices drop $2/t w-o-w: China’s spot prices of iron ore fines (Fe 62%) were assessed at $99.3/t CFR on 29 April, down $2/t w-o-w following weak trading volumes, as the market reacted to the lack of supportive measures from the recent Politburo meeting. Reports show a notable rise in molten iron production, and steel mills are still profitable. Still, the lack of effective economic stimulus measures has led to the decline.

Route-wise updates

- India-China: Freights from the Indian Ocean to China were recorded at $10.3/t, down by $0.3/t w-o-w. According to sources, one Supramax vessel got booked from New Manglore port to Qingdao at $12.8/t for early May shipment.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $8/t on 30 April, up $1/t w-o-w. According to sources, major Australian miner Rio Tinto was seen actively booking Capesize vessels from a Western Australia port to Qingdao at around $7.35-8.05/t. Shipment is scheduled for 9-13 May.

- Brazil-China: Freights for Capesize vessels from Brazil to China decreased this week. Rates from Tubarao to Qingdao Port were assessed at $19.8/t on 30 April, an increase of $1.1/t w-o-w. As per sources, one Capesize vessel got booked from Tubarao port to Qingdao port at $19.60/t with shipment scheduled for 12-20 May.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao Port rose by $1/t w-o-w to $14.7/t. Sources informed BigMint that freight rates from South Africa to China have risen due to consistent demand for iron ore cargoes, coupled with tight vessel availability in the region, especially for prompt loading dates.

Leave a Reply