- Surge in scrap demand driven by decarbonisation

- 75 caps include 38% partial/complete export ban

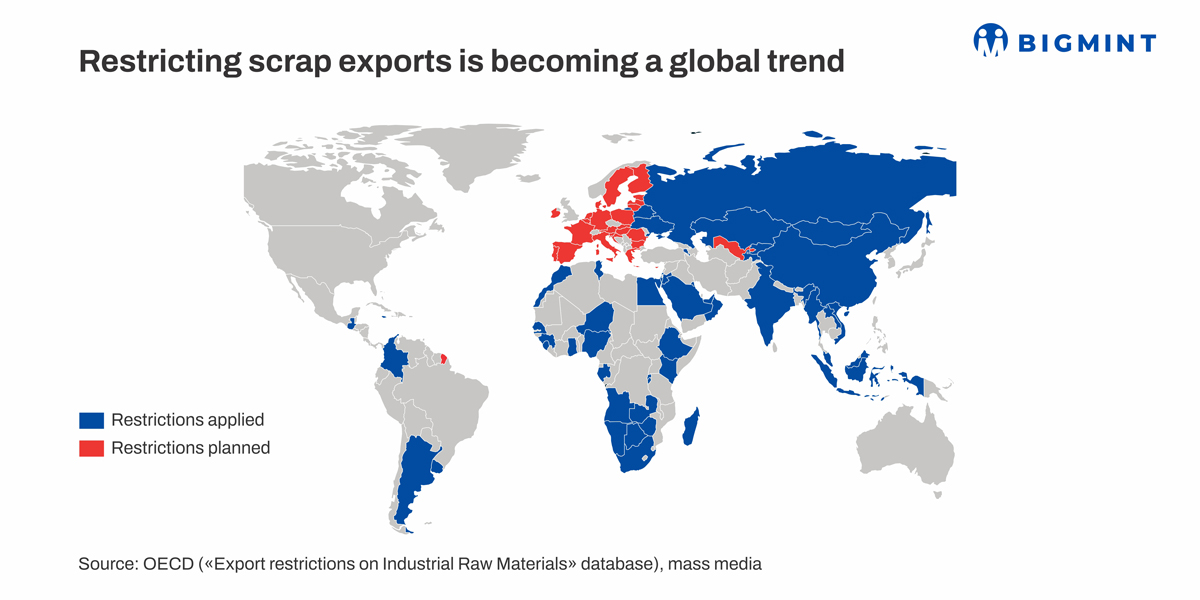

SteelDaily: Ferrous scrap export restrictions are becoming more widespread globally. As of March 2025, around 48 countries have imposed 75 different restrictions on scrap exports, with 38% of these measures involving partial or complete export bans.

This measure is designed to prioritise securing domestic supply in response to the surge in scrap demand driven by the decarbonisation of the steel industry, while supply remains constrained. It is also seen as crucial for stabilising ferrous scrap prices and preserving industrial competitiveness.

To give a few country-specific examples, Burundi has banned exports to regions outside the East African Community (EAC), while Kazakhstan has imposed similar restrictions on exports to regions outside the Eurasian Economic Union (EAEU), alongside tariffs on certain areas.

The European Union is also revised its waste transport regulations in 2024 to limit ferrous scrap exports to non-OECD countries and is considering further measures by Q3CY’25.

Countries have adopted a range of measures to regulate ferrous scrap exports, including export tariffs (27%), export licenses (27%), and export bans (25%). Tariffs are often applied with flexibility, but a growing number of nations are opting for stricter export bans.

These regulations are largely long-term in nature, with many countries transitioning from bans to tariff-based controls rather than lifting restrictions altogether. For instance, the United Arab Emirates has lifted its export ban but continues to regulate exports through the introduction of tariffs starting in 2024.

Steel scrap is increasingly being recognised as a strategic resource, vital to the competitiveness of eco-friendly steel production rather than just a basic industrial input. As a result, countries are actively implementing export restrictions to safeguard their domestic industries and promote fair trade practices.

Outlook

As global demand for low-carbon steel accelerates, ferrous scrap will continue to play a critical role in green steelmaking. Export restrictions are expected to intensify, with more countries likely to adopt long-term measures such as tariffs or bans to secure domestic supply. The European Union’s upcoming regulatory changes and broader global policy shifts signal a tightening landscape, potentially leading to more regionalised scrap markets and pricing volatility.

Leave a Reply