- Prolonged monsoons impact domestic iron ore mining

- New infrastructure projects boost India’s steel demand

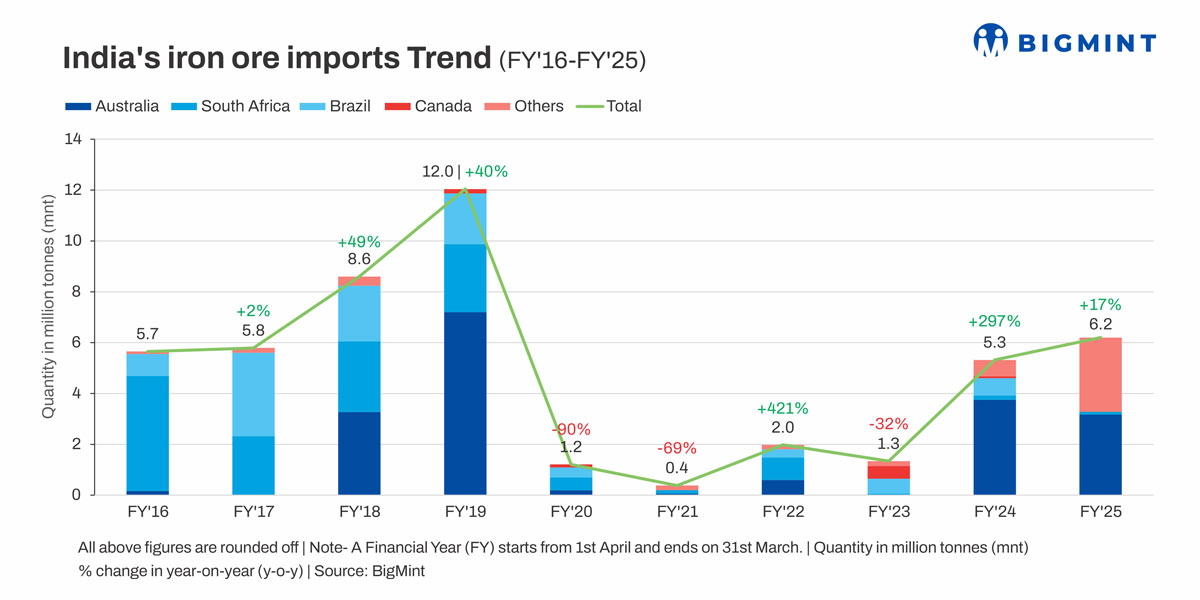

India’s iron ore imports touched 6.2 million tonnes (mnt) in FY’25, marking a six-year high, data maintained with BigMint show. Imports increased by around 17% y-o-y against 5.32 mnt in FY’24, driven by factors such as rising domestic demand from steel producers, supply constraints in key mining regions due to extended monsoons, and fluctuations in global iron ore prices.

Notably, import volumes exceeded 1 mnt for the first time in nearly six years in November 2024, a level last recorded in December 2018.

Australia leading exporter but volumes decline

Australia was the largest exporter of iron ore to India at 3.17 mnt in FY’25, a significant decrease of 15% when compared to 3.75 mnt in the year-ago period. The drop was primarily due to weather-related disruptions in February 2025, which impacted mining and port operations. However, activity rebounded strongly in March 2025, with both production and port functions returning to normal.

Oman and Malaysia occupied the second and third positions among the top exporters with 2.2 mnt and 0.72 mnt, respectively. However, according to sources, this was largely Brazilian ore, which was routed to Oman and Malaysia for post-processing.

JSW emerges as largest importer

JSW Steel, with an import volume of 5.76 mnt, stood as the leading iron ore importer in the period under review.

Port-wise imports

Among the ports, Jaigarh accounted for the biggest share of imports, with 3.14 mnt, followed by Mumbai and Krishnapatnam at 1.77 and 1.27 mnt, respectively.

Why iron ore imports surged in FY’25?

Crude steel production increases: India’s crude steel production capacity increased by over 10% y-o-y in FY’25 to 205 mnt as against 186 mnt in FY’24, according to provisional data maintained with BigMint. Capacity has almost doubled in the last 10 years from 109 mnt in FY’15.

Meanwhile, India’s crude steel production is projected to have increased by 6% y-o-y in FY’25 to 152 mnt from 144 mnt in the preceding fiscal. The sharp rise in capacity and production reflects rapid economic growth, urbanisation, and strong government infrastructure spending.

Budget 2025’s capital outlay of over INR 11.5 lakh crore for major connectivity and urban projects has been a key driver of steel demand. Flagship initiatives such as Housing for All, Bharatmala, Sagarmala, dedicated freight corridors, airport expansion, and metro rail development have significantly boosted steel consumption, resulting in increased production.

Domestic supply tightens: Prolonged monsoons and robust demand tightened domestic supply, prompting a rise in iron ore imports to meet industrial needs.

In mid-2024, domestic production lagged behind rising demand, leading to supply shortages. India’s iron ore output dropped sharply by 27% to 19.25 mnt in July 2024, followed by a further 1% decline to 18.99 mnt in August, reinforcing the reliance on imports to fill the shortfall.

Global iron ore prices fluctuate: Global iron ore prices remained volatile throughout the year, prompting Indian mills (especially those located near ports) to turn to imports as a cost-effective way to sustain production.

Prices of Fe 62% iron ore fines dropped from around $143/tonne (t) CFR China in January 2024 to approximately $100/t in March 2024 and continued to fluctuate, reaching about $90/t by mid-September 2024, according to BigMint data.

Logistical constraints make imports cost-effective: Over and above the high domestic freight charges, logistical hurdles, especially transporters’ issues, impacted dispatches in Odisha. Additionally, logistical difficulties intensified during the monsoon, tipping the balance in favour of imports for some coast-based mills. Notably, iron ore dispatches from Odisha hit an over one-year low in September 2024.

Quality issues affect domestic ore sourcing: Quality concerns with domestic iron ore drove mills to favour imports. Indian ore typically contains higher levels of gangue, especially alumina and silica, compared to Australian material, making it less suitable for efficient sintering and blast furnace operations. Additionally, as most merchant miners approached their environmental clearance (EC) limits, access to high-grade domestic ore became increasingly constrained, further encouraging reliance on imported material.

Outlook

While import volumes rose, they still represent a small fraction of India’s total iron ore consumption, which reached approximately 256 mnt in FY’25.

Recently, southern India-based direct reduced iron (DRI) traders and manufacturers have increasingly turned to imported high-grade iron ore lumps from South Africa to ensure stable raw material supply amid domestic market volatility and supply fluctuations. With tight availability of high-grade ore in key producing regions such as Odisha and Karnataka, combined with logistical challenges and rising crude steel production targets, India’s iron ore imports are expected to remain elevated.

Leave a Reply