- Turkish mills struggle with high finished stocks

- Indian buyers prefer local scrap, sponge iron

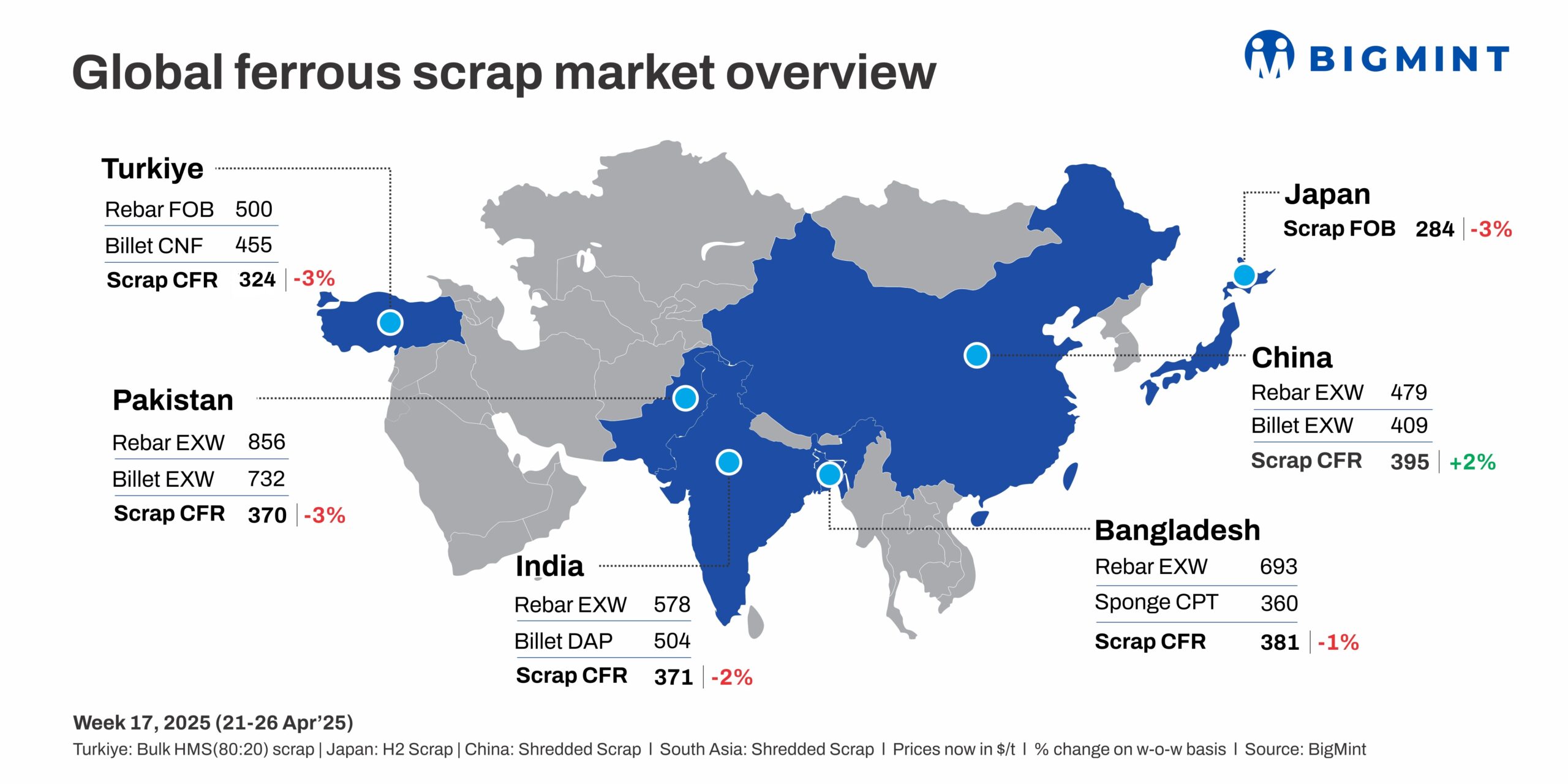

Global ferrous scrap prices remained subdued this week, with key markets such as Turkiye, India, Pakistan, and Bangladesh facing lukewarm demand. In Turkiye, prices dropped to a three-year low due to weak rebar demand. India’s market saw reduced activity with lower prices, while Pakistan and Bangladesh experienced limited buying interest amid weak steel demand and high inventories.

Turkiye: The imported scrap market faced pressure throughout the week. Prices plunged to their lowest in three years, as weak rebar demand and high inventories of finished steel led mills to postpone scrap purchases.

US-origin HMS 80:20 offers hovered at around $325/t CFR, a 3% drop from last week’s $335/t. Sellers, dealing with oversupply and thin margins, were forced to accept lower prices, while buyers remained hesitant due to the lack of urgency and concerns over falling Turkish scrap values.

As the week progressed, the bearish sentiment continued, driven by sluggish domestic rebar sales and limited demand for scrap. Prices of HMS 80:20 from the US, Baltic, and EU continued to decline, with offers at around $315-325/t CFR.

Despite a brief rebound in rebar sales, the market remained under strain, with both suppliers and buyers cautious amid rising freight costs and unfavourable currency dynamics. While there were some signs of stabilisation towards the end of the week, sentiment remained weak due to oversupply and low buying interest.

India: The imported ferrous scrap market stayed subdued this week as prices averaged $371/t CFR, down 2% from last week. Weak global cues, falling domestic steel prices, and slowing demand from Turkiye weighed on sentiment. Confusion over the new 12% safeguard duty added caution. Buyers preferred local scrap or alternatives such as sponge iron amid liquidity issues and high port inventories.

Shredded offers from UK/Europe hovered at $370-375/t CFR Nhava Sheva, but bids lagged at $365-370/t. Falling Turkish scrap prices, rising freight costs, and full inventories at ports such as Kandla limited fresh deals, with buyers preferring ready or short-haul shipments.

Around 18,000-19,000 t of imported scrap were booked in India, comprising 14,000-15,000 t of HMS 80:20 at $350-375/t and 1,000-1,500 t of shredded priced within $370-380/t. The remaining volume consisted of HMS 1, LMS bundles, and turning scrap.

Pakistan: The imported scrap market remained under pressure throughout the week amid weak steel demand, sluggish rebar and billet sales, and global price corrections. Mills continued operating at just 30-40% capacity, with buyers largely inactive due to cash flow constraints and limited downstream activity. Shredded prices fell 3% w-o-w to $370/t from $381/t, reflecting bearish sentiment.

A few small-lot container deals were heard earlier in the week at $368-371/t, but activity dwindled as the week progressed. Domestic scrap hovered at PKR 135,000-140,000/t ($483-501/t), while billets and rebars traded at PKR 200,000-205,000/t ($712-730/t) and PKR 230,000-240,000/t ($820-855/t), respectively.

Around 16,000 t of imported scrap were booked in Pakistan, comprising 13,000-14,000 t of shredded at $369-389/t and 1,000-1,200 t of fabrication at $384-386/t from the UK/Europe and the UAE.

Bangladesh: The imported scrap market remained quiet this week amid soft steel demand, high production costs, and ongoing letter of credit (LC) issues. Buyers were largely inactive, holding sufficient inventories for May-June and expecting further price drops. Shredded prices fell 1% w-o-w to $381/t from $386/t, reflecting weak sentiment. Meanwhile, HMS 80:20 was heard at $365-370/t, with bids near $360/t.

Few deals were observed, as mills focused on July shipments. Bulk and container offers saw limited interest due to rising freight costs, high energy tariffs, and continued currency pressure.

Japan: H2 scrap export offers stood at JPY 40,900/t ($285/t) FOB Tokyo Bay, down JPY 1,100/t ($8/t) from last week. The strengthening yen and weak demand from Turkiye and Asian buyers added pressure. Tokyo Steel reduced its scrap purchase prices by JPY 500/t ($4/t), marking its seventh cut in April. Domestic prices also saw slight declines.

China: Shagang Steel increased scrap procurement prices for the first time this year. Prices were raised by RMB 50/t ($7/t) across all grades from 25 April 2025. Following the adjustment, HMS (6-10 mm) stood at RMB 2,390/t ($328/t), up from RMB 2,340/t ($321/t), inclusive of 13% VAT.

Vietnam: The imported scrap market showed moderate activity, with prices under pressure. Japanese H2 slipped to $325-330/t CFR, while shredded traded at around $345/t CFR. A bulk deal involving 10,000 t of HS and Shindachi was closed at $360-362/t CFR. Despite early signs of recovery in domestic demand, mills remained cautious, influenced by falling billet prices and weak global sentiment.

US: The scrap export index dropped by $18/t w-o-w due to weaker demand, as cheaper Chinese billets entered the market. FOB prices of HMS 80:20 and shredded decreased to $305/t and $325/t, respectively.

Key importers such as Turkiye, Bangladesh, and Vietnam showed subdued demand, driven by weak steel demand, currency volatility, and mills prioritising cost control amid a bearish outlook for flat steel.

Leave a Reply