- List price hikes, supply constraints lift offers

- End-user demand shows slight improvement

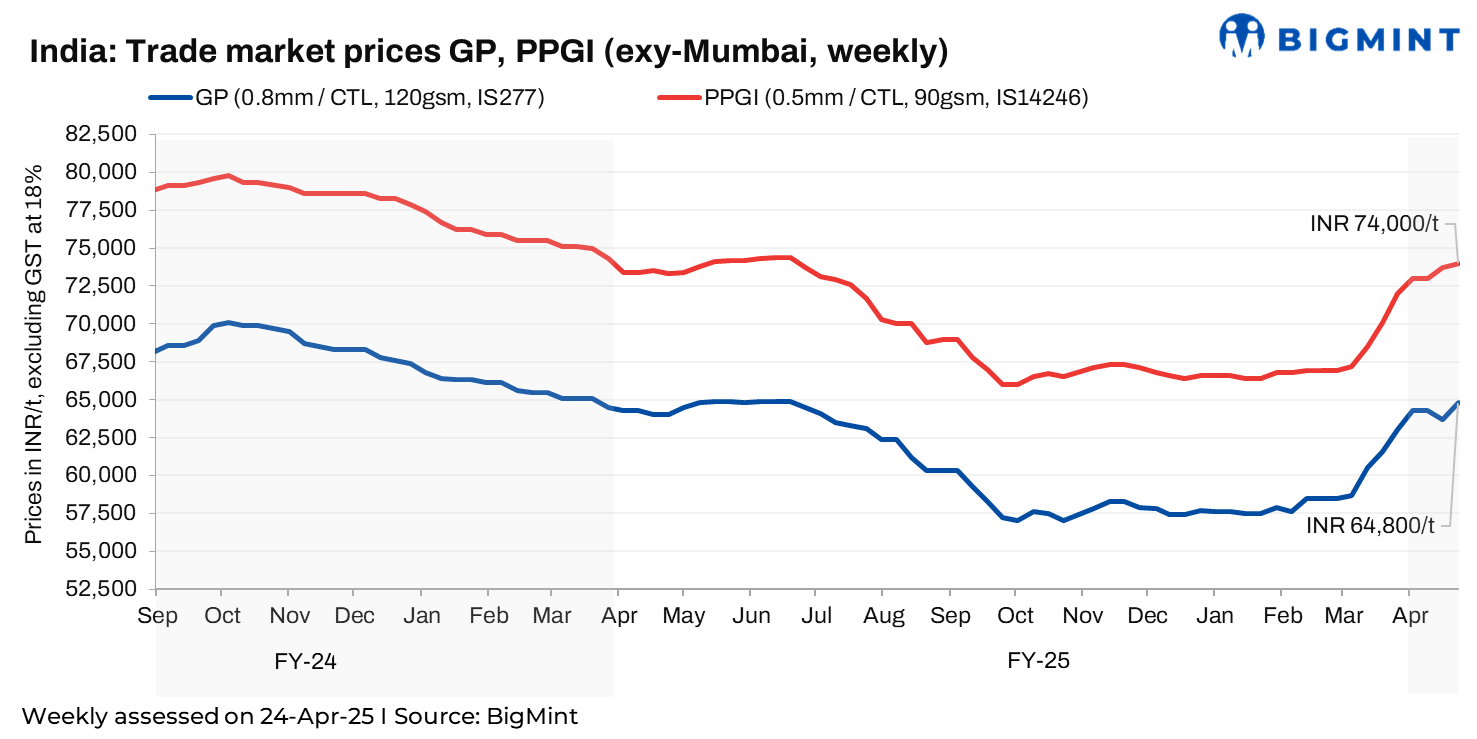

Trade-level coated flat steel prices rose by up to INR 1,100/t ($13/t) w-o-w, backed by improved inquiries and demand. Prices of galvanised plain (GP) steel coils increased by INR 400-1,100/t ($5-13/t) w-o-w, whereas those of pre-painted galvanised iron (PPGI) nudged up by INR 300-700/t ($4-8/t) across markets.

Meanwhile, a major private mill announced a list price hike of INR 1,000/t for GP and INR 750/t for PPGI on around 18 April 2025. This action also prompted distributors to quote higher in the traders’ market. Effectively, list prices increased to around INR 64,600/t ($757/t) exy-Mumbai for GP (0.8 mm, 80 gsm, IS277) exy-Mumbai and INR 74,500/t ($874/t) exy-Mumbai for PPGI (0.5 mm, 90 gsm, IS14246). The prices mentioned are for coil forms, excluding GST at 18%.

The latest weekly assessment, on 25 April 2025, shows galvanised plain (GP, 0.8 mm/CTL, 120 gsm, IS277) steel coil prices at INR 64,800/t ($760/t) exy-Mumbai, with offers varying in the range of INR 64,000-65,000/t ($750-762/t) exy-Mumbai, higher by INR 1,100/t ($13/t) w-o-w. Similarly, pre-painted galvanised iron (PPGI, 0.5 mm/CTL, 90 gsm, IS14246) was assessed at INR 74,000/t ($868/t) exy-Mumbai, with offers at INR 73,500-74,500/t ($862-874/t). Prices are minus GST at 18% (USD 1 = INR 85.2866; INR 1 = USD 0.0117252).

Market updates

Supply constraints favour higher quotes from traders: Supply disruptions in the distribution network from domestic mills allowed distributors to quote higher offers this week.

As reported last week, a major private mill in Jamshedpur began capital maintenance on one of its blast furnaces on 1 April. Industry sources expect the process, involving realignment and refractory brick replacement, to last 1-2 months and cause downstream production losses. This has supported the rise in colour-coated steel prices.

Meanwhile, another major private mill had decent volumes in their export log books till 22 April 2025, which made them cut their allocations for the traders’ segment, further restricting supplies to the distribution network.

Demand from various end-user industries improves: Growing demand across various end-user industries, coupled with tight supply conditions, led distributors to increase market quotations this week.

Seasonal factors, including summer and the pre-monsoon period, led to steady demand from key industrial buyers, particularly those engaged in roofing, cladding, white goods, automotive, and machinery manufacturing.

“Several key end-user industries- such as roofing, cladding, white goods, automobile, and machinery manufacturing- have started sending in their requirements after having stayed on the sidelines during the first fortnight of the month,” stated a leading distributor from the western region.

“There has been a decent increase in inquiries from manufacturers of white goods and industrial cooling solutions as summer sets in. Similarly, demand is gradually rising for profiled coated flat products, particularly from roofing and cladding material manufacturers preparing themselves for end-buyers coming out and procuring as monsoon season closes in,” BigMint learnt from a north-based distributor.

Additionally, the automotive sector has also ramped up its procurement, creating additional pathways for the utilisation of value-added flat products, he added.

Outlook

Trade-level prices are set to rise in the near term, driven by increasing demand, supply constraints, mill price hikes, and import restrictions – all reinforcing higher distributor quotations. Additionally, market buzz is that mills may raise list prices of coated flat products by INR 1,500-2,000/t ($18-23/t) for May 2025 sales. It remains to be seen how market participants will navigate the coming weeks amid evolving challenges to their bargaining position.

Leave a Reply