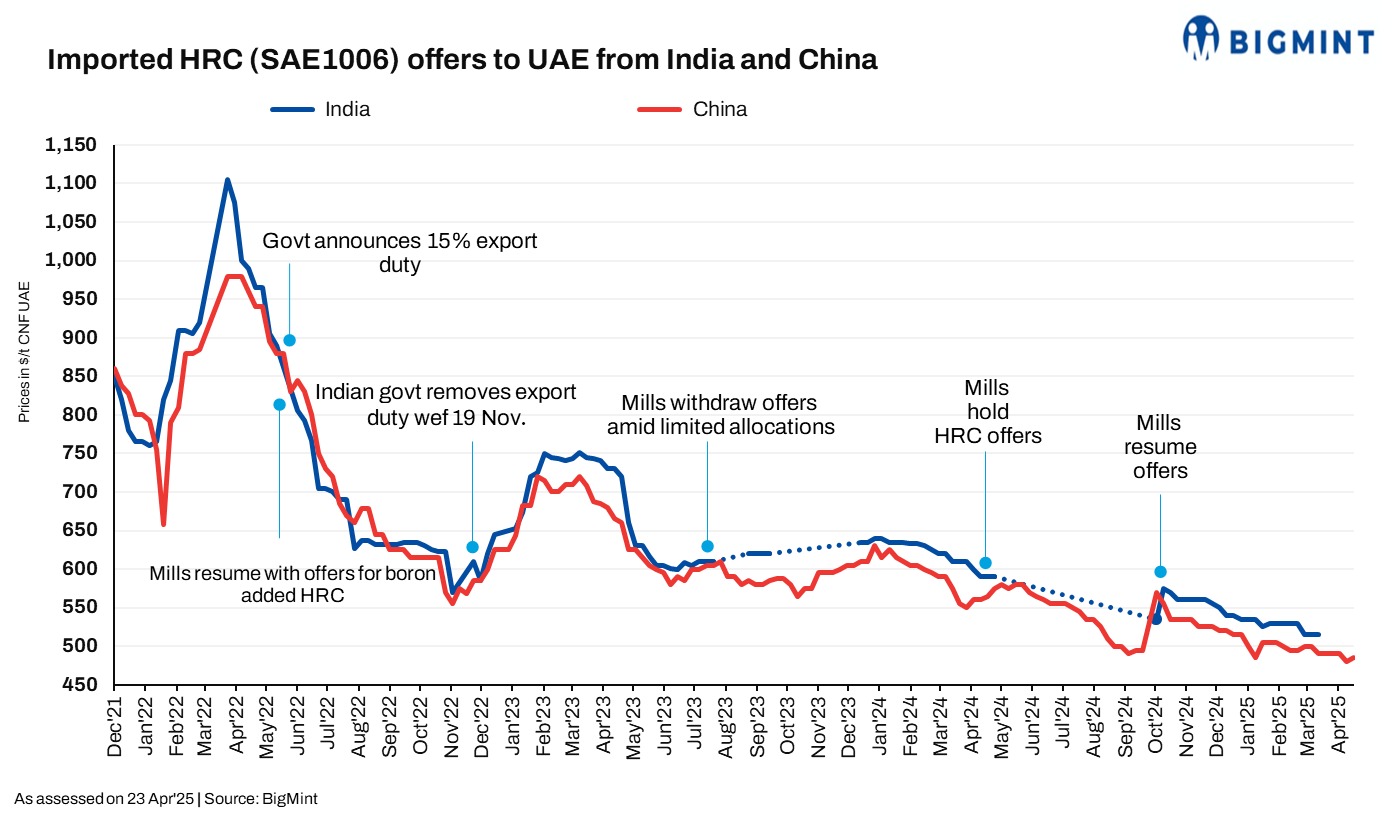

The Middle Eastern hot-rolled coil (HRC) market saw a modest uptick in demand this week, driven by recent transactions. Despite the rise in demand, a reliable source said, “the ongoing tariff war is creating unfavourable business conditions, while the weather is not a major concern at the moment”. However, Chinese HRC offers to the region increased w-o-w following a recent deal. Japan has also secured a deal recently. Meanwhile, Indian mills are holding back offers due to stiff competition from Chinese suppliers and higher domestic realisation.

Chinese HRC (S235 and S275) export offers to the Middle East (ME) increased by $5/t w-o-w to $485-490/t CFR UAE as compared to $480-485/t CFR a week ago. Moreover, a deal of around 12,000 t is heard concluded at $487/t CFR for May’25 shipments, as per BigMint sources.

HRC futures on the Shanghai Futures Exchange (SHFE) stood at RMB 3,188/t ($436/t), down RMB 52/t ($7/t) w-o-w against RMB 3, 240/t ($443/t). However, d-o-d, SHFE HRC futures decreased by RMB 9/t ($1/t) against RMB 3,197/t ($437/t).

Indian mills are not actively offering to the ME due to competitive Chinese offers and higher domestic realisations. Indian steel export volumes to the UAE stood at 85,888 t in March, representing a rise of 38,880 t y-o-y against 47,008 t in March 2024. Additionally, m-o-m, prices went up by 59,893 from 25,995 t in February.

Japan concluded a deal of around 35,000-40,000 t to the ME at $505/t CFR for May shipment. Japan’s steel exports to the UAE in February rose sharply by 37,353 t y-o-y to 51,476 t compared to 14,123 t in the year-ago period. However, m-o-m, prices declined by 75,888 t from 127,364 t in January.

Outlook

The Middle Eastern HRC market is poised for steady growth, driven by infrastructure projects and construction demand. Competitive Chinese offers and potential shifts in global trade policies will influence market trends.

Leave a Reply